Answered step by step

Verified Expert Solution

Question

1 Approved Answer

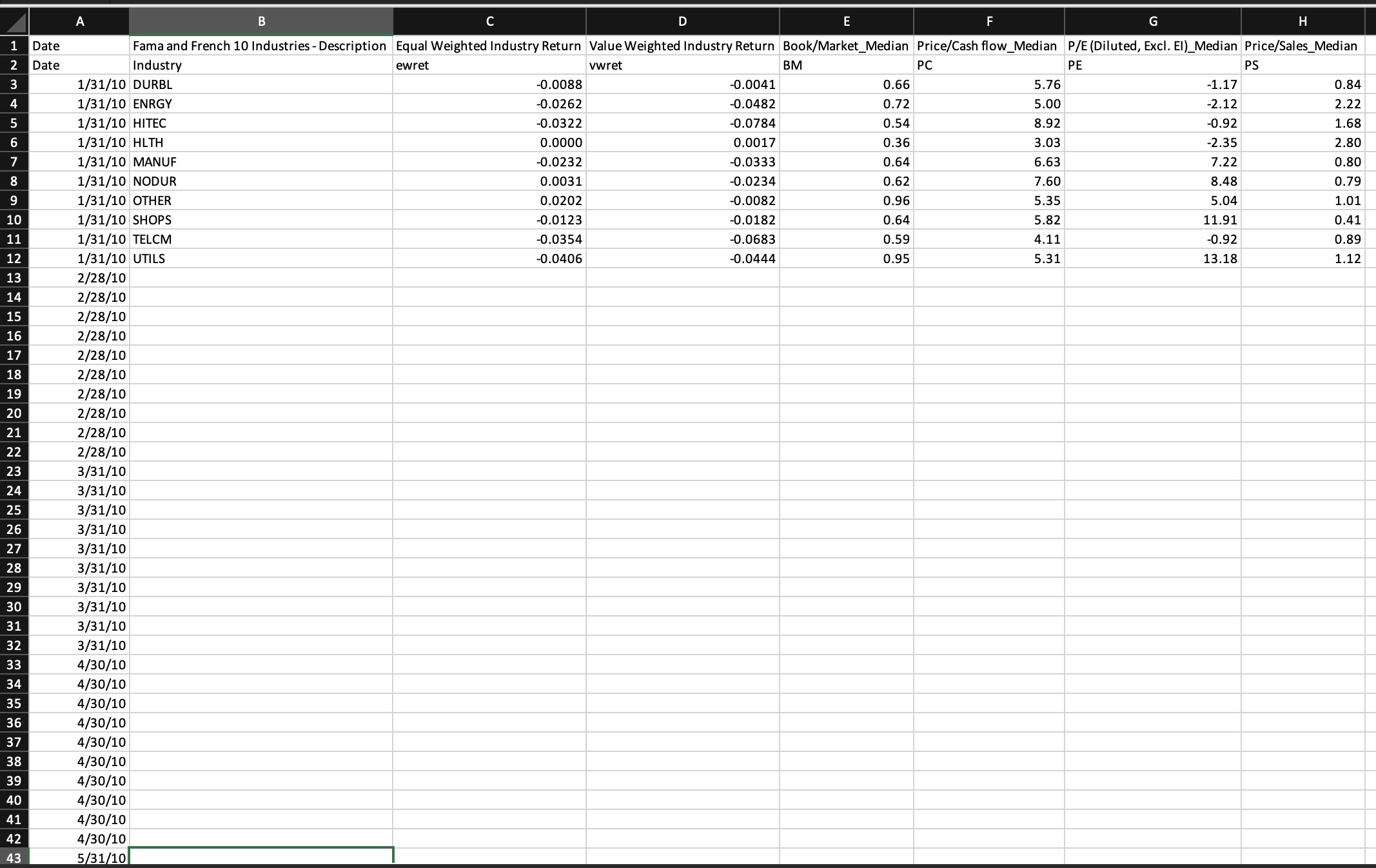

For the period 2 0 1 0 - 2 0 2 2 , calculate the arithmetic mean, standard deviation, skewness, kurtosis, and VaR ( at

For the period calculate the arithmetic mean, standard deviation, skewness, kurtosis, and VaR at for the industry portfolio equalweighted monthly return ewretDo not distinguish different industries, just report these summary statistics for ewret

Arithmetic Mean industry monthly return Round it to decimal points, no percentage sign

Standard Deviation of industry monthly returns Round it to decimal points, no percentage sign

Skewness of industry monthly returns Round it to decimal points, no percentage sign

Kurtosis of industry monthly returns Round it to decimal points, no percentage sign

Value at Risk VaR at of industry monthly returns based on the empirical distribution percentileRound it to decimal points, no percentage sign

Question points

Question options:

Perform a value strategy based on the booktomarket equity BM lagged by one month. Each month, identify your value portfolio to be the industry with the highest BM and your growth portfolio to be that with the lowest BM Create a longshort strategy that invests one dollar in the value portfolio and shorts one dollar in the growth portfolio each month. The value or growth portfolio is equalweighted ewret Calculate the mean returns of the long leg L the short leg S and the longshort portfolio L S and the Sharpe ratios of the longshort portfolios over the sample period

Mean return of the long leg Lby investing $ in the value portfolio: Round it to decimal points, no percentage sign

Mean return of the short leg Gby investing $ in the equalweighted growth portfolio: Round it to decimal points, no percentage sign

Mean return of the longshort portfolio L Sby investing $ in the equalweighted value portfolio and shorting $ in the equalweighted growth portfolio: Round it to decimal points, no percentage sign

Standard Deviation of the longshort portfolio L Sby investing $ in the equalweighted value portfolio and shorting $ in the equalweighted growth portfolio: Round it to decimal points, no percentage sign

Question points

Question options:

Repeat the exercise in Q but select the top and bottom portfolios to be your value and growth portfolio based on BM The value growth portfolio is the equalweighted portfolio invested in the selected two equalweighted industry portfolios.

Mean return of the long leg Lby investing $ in the value portfolio: Round it to decimal points, no percentage sign

Mean return of the short leg Gby investing $ in the equalweighted growth portfolio: Round it to decimal points, no percentage sign

Mean return of the longshort portfolio L Sby investing $ in the equalweighted value portfolio and shorting $ in the equalweighted growth portfolio: Round it to decimal points, no percentage sign

Standard Deviation of the longshort portfolio L Sby investing $ in the equalweighted value portfolio and shorting $ in the equalweighted growth portfolio: Round it to decimal points, no percentage sign

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

College Accounting A Career Approach

Authors: Cathy J. Scott

13th edition

1337280569, 978-1337607773, 1337607770, 978-1337516525, 133751652X, 978-1337668026, 978-1337280563