Answered step by step

Verified Expert Solution

Question

1 Approved Answer

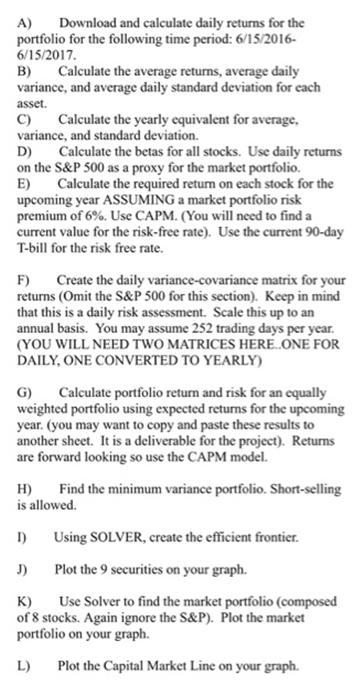

For this project, you will build a portfolio of 8 assets plus the S&P 500 from the following options (9 assets in all): Asset

For this project, you will build a portfolio of 8 assets plus the S&P 500 from the following options (9 assets in all): Asset Group Bulldog: (select 2 stocks from this group. You can't pick three in a row) Coca-Cola (KO) Pepsico, Inc. (PEP) Home Depot (HD) Lowes (LOW) Target (TGT) Walgreen Corporation (WAG) WalMart Stores (WMT) Asset Group Yellow Jacket: (select 4 stocks from this group. You can't pick four in a row) Cicso Systems (CSCO) International Business Machines (IBM) General Electric (GE) Apple Computer (AAPL) Exxon Mobil (XOM) Caterpillar (CAT) Facebook (FB) Twitter (TWTR) Yahoo! (YHOO) Johnson and Johnson (JNJ) Verizon (VZ) Netflix (NFLX) Asset Group Hoosier: (select 2 stocks from this group. You can't pick three in a row) Synovous (SNV) World Wrestling Entertainment (WWE) Anheuser-Busch InBEV (BUD) AT&T (T) Ford Motor Company (F) Delta Air Lines, Inc (DAL) Asset Group Falcon: (select 1 from this group) S&P 500 (^GSPC) Using your 9 stock portfolio plus the S&P Index, perform the following steps: A) Download and calculate daily returns for the portfolio for the following time period: 6/15/2016- 6/15/2017. B) Calculate the average returns, average daily variance, and average daily standard deviation for each asset. Calculate the yearly equivalent for average. variance, and standard deviation. D) Calculate the betas for all stocks. Use daily returns on the S&P 500 as a proxy for the market portfolio. E) Calculate the required return on each stock for the upcoming year ASSUMING a market portfolio risk premium of 6%. Use CAPM. (You will need to find a current value for the risk-free rate). Use the current 90-day T-bill for the risk free rate. F) Create the daily variance-covariance matrix for your returns (Omit the S&P 500 for this section). Keep in mind that this is a daily risk assessment. Scale this up to an annual basis. You may assume 252 trading days per year. (YOU WILL NEED TWO MATRICES HERE. ONE FOR DAILY, ONE CONVERTED TO YEARLY) G) Calculate portfolio return and risk for an equally weighted portfolio using expected returns for the upcoming year. (you may want to copy and paste these results to another sheet. It is a deliverable for the project). Returns are forward looking so use the CAPM model. H) Find the minimum variance portfolio. Short-selling is allowed. I) Using SOLVER, create the efficient frontier. J) Plot the 9 securities on your graph. K) Use Solver to find the market portfolio (composed of 8 stocks. Again ignore the S&P). Plot the market portfolio on your graph. L) Plot the Capital Market Line on your graph.

Step by Step Solution

★★★★★

3.39 Rating (155 Votes )

There are 3 Steps involved in it

Step: 1

A To download and calculate daily returns for the portfolio for the given time period you would need access to financial data or a financial software The daily returns can be calculated using the form...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Statistical Reasoning for Everyday Life

Authors: Jeff Bennett, Bill Briggs, Mario F. Triola

4th edition

978-0321817747, 321817745, 978-0321890139, 321890132, 321817621, 978-0321817624