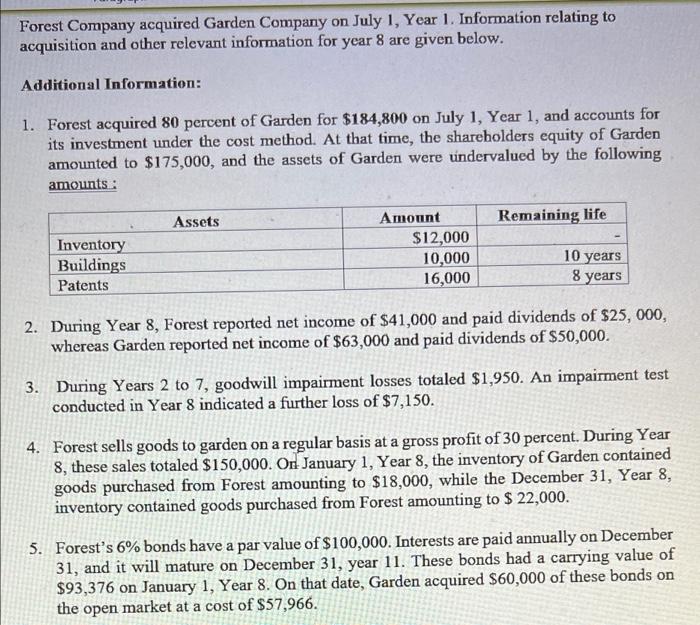

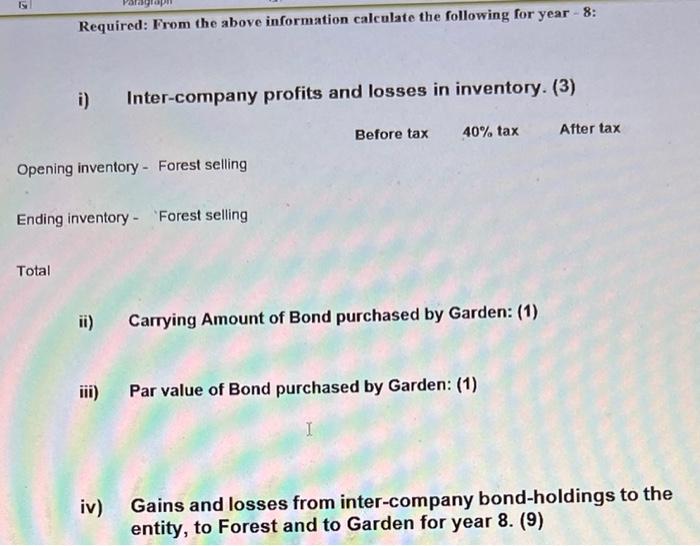

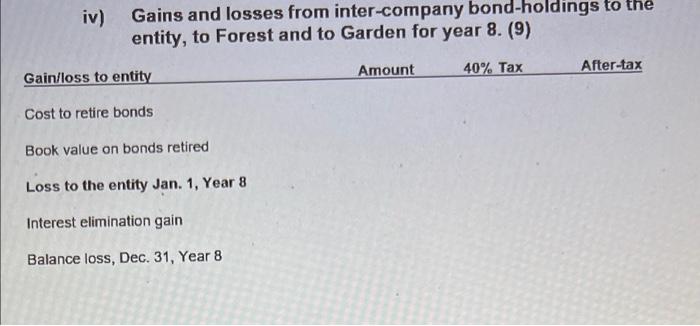

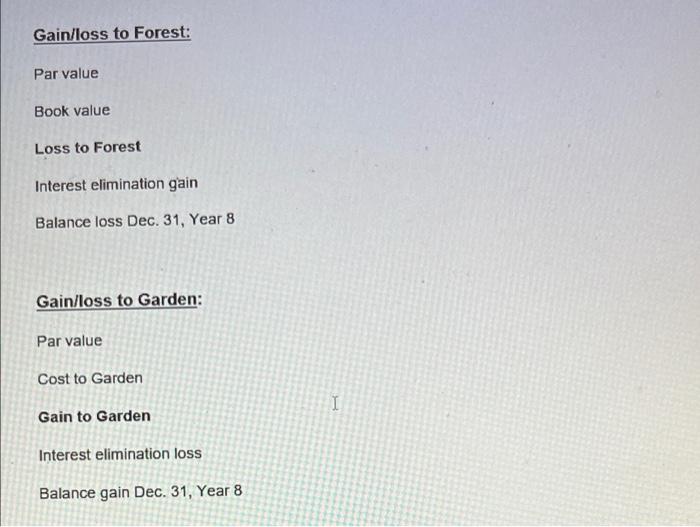

Forest Company acquired Garden Company on July 1, Year 1. Information relating to acquisition and other relevant information for year 8 are given below. Additional Information: 1. Forest acquired 80 percent of Garden for $184,800 on July 1, Year 1, and accounts for its investment under the cost method. At that time, the shareholders equity of Garden amounted to $175,000, and the assets of Garden were undervalued by the following amounts: Assets Remaining life Inventory Buildings Patents Amount $12,000 10,000 16,000 10 years 8 years 2. During Year 8, Forest reported net income of $41,000 and paid dividends of $25,000, whereas Garden reported net income of $63,000 and paid dividends of $50,000. 3. During Years 2 to 7, goodwill impairment losses totaled $1,950. An impairment test conducted in Year 8 indicated a further loss of $7,150. 4. Forest sells goods to garden on a regular basis at a gross profit of 30 percent. During Year 8, these sales totaled $150,000. On January 1, Year 8, the inventory of Garden contained goods purchased from Forest amounting to $18,000, while the December 31, Year 8, inventory contained goods purchased from Forest amounting to $ 22,000. 5. Forest's 6% bonds have a par value of $100,000. Interests are paid annually on December 31, and it will mature on December 31, year 11. These bonds had a carrying value of $93,376 on January 1, Year 8. On that date, Garden acquired $60,000 of these bonds on the open market at a cost of $57,966. 6. Garden owes Forest $22,000 on open account on December 31, Year 8. 7. Assume a 40 percent corporate tax rate and allocate bond gains (losses) between the two companies IS Required: From the above information calculate the following for year - 8: i) Inter-company profits and losses in inventory. (3) Before tax 40% tax After tax Opening inventory - Forest selling Ending inventory - "Forest selling Total ii) Carrying Amount of Bond purchased by Garden: (1) Par value of Bond purchased by Garden: (1) I iv) Gains and losses from inter-company bond-holdings to the entity, to Forest and to Garden for year 8. (9) iv) Gains and losses from inter-company bond-holdings to the entity, to Forest and to Garden for year 8. (9) Amount 40% Tax After-tax Gain/loss to entity Cost to retire bonds Book value on bonds retired Loss to the entity Jan. 1, Year 8 Interest elimination gain Balance loss, Dec. 31, Year 8 Gain/loss to Forest: Par value Book value Loss to Forest Interest elimination gain Balance loss Dec. 31, Year 8 Gain/loss to Garden: Par value Cost to Garden 1 Gain to Garden Interest elimination loss Balance gain Dec. 31, Year 8