Answered step by step

Verified Expert Solution

Question

1 Approved Answer

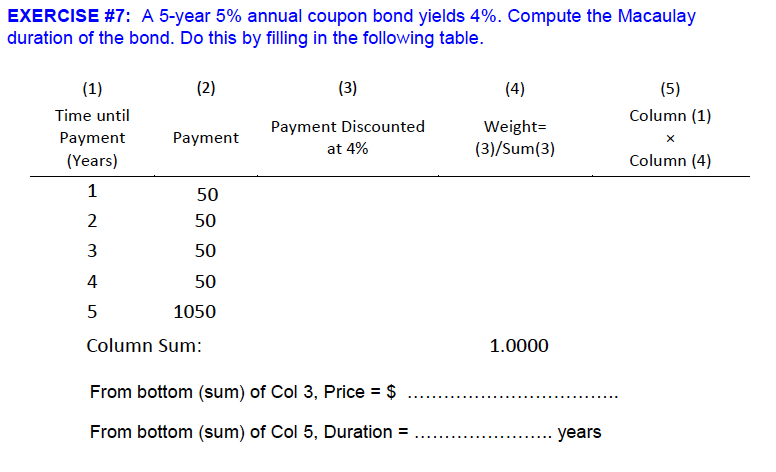

four decial places please A 5-year 5% annual coupon bond yields 4%. Compute the Macaulay duration of the bond. Do this by filling in the

four decial places please

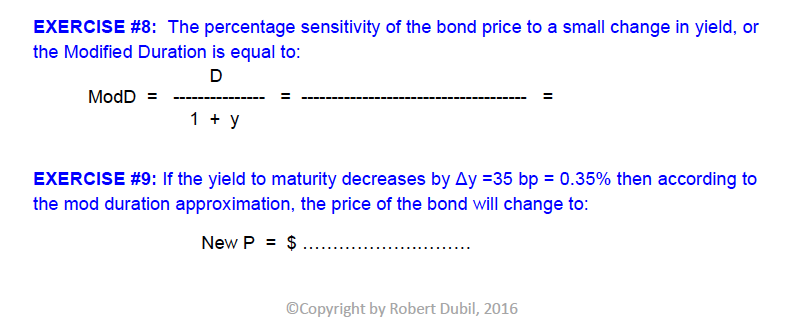

A 5-year 5% annual coupon bond yields 4%. Compute the Macaulay duration of the bond. Do this by filling in the following table. The percentage sensitivity of the bond price to a small change in yield, or the Modified Duration is equal to: ModD = D/1 + y = = If the yield to maturity decreases by Delta y = 35 bp = 0.35% then according to the mod duration approximation, the price of the bond will change to: New P = $Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

McMillan On Options

Authors: Lawrence G. McMillan

2nd Edition

0471678759, 978-0471678755