From material contained in the required reading: Laskaris, J. & Regan, K. (2013). The New Break-Even Analysis. Hfm (Healthcare Financial Management), 67(12) Pages 1-6. (PICTURES

From material contained in the required reading: Laskaris, J. & Regan, K. (2013). The New Break-Even Analysis. Hfm (Healthcare Financial Management), 67(12) Pages 1-6. (PICTURES ATTACHED)

This article refers to "never events" under the Affordable Care Act (AFA) as events that can significantly impact payment. From the internet research "never events in healthcare"

Summarize the "never events"

Explain how they could impact a break-even analysis.

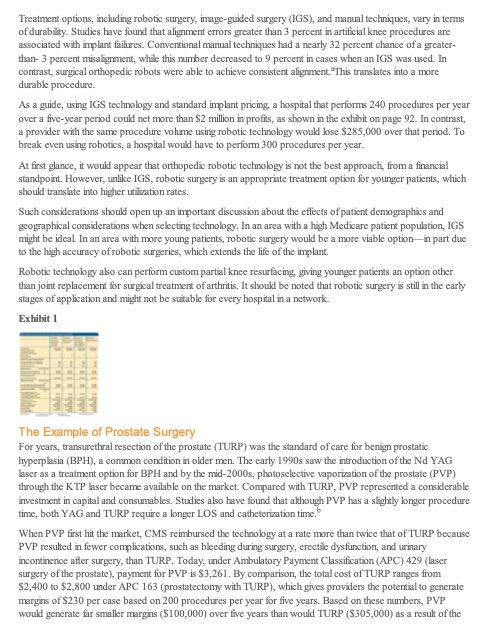

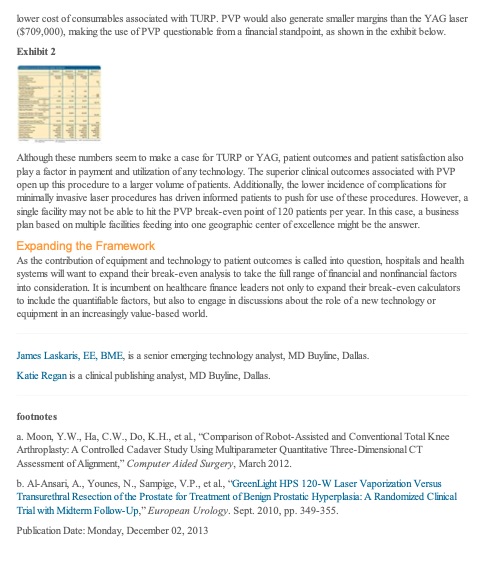

The New Break-Even Analysis JAMES LASKARIS, KATIE REGAN IT'S TIME TO EXPAND THE SCOPE AND ASSUMPTIONS OF THE TRADITIONAL BREAK EVEN ANALYSIS. At a Glance Changes in the economic and legislative environment have complicated the capital acquisition landscape. Hospitals and health systems should: . Question the assumptions that underlic their break-even analysis . Revamp the break-even calculator . Engage in discussions about the clinical aspects of equipment and technology acquisition decisions Hospitals and health systems that contemplate an investment in new equipment or technology typically estimate procedure volume, payment rates, and the useful life of the equipment to determine how long it will take to recoup that investment. That information has allowed these organizations to make reasonably accurate revenue projections for purposes of conducting a break-even analysis and making a capital acquisition decision. But changes in the economic and legislative environment are complicating the capital acquisition landscape. These environmental changes are making it imperative for break-even calculators to evolve based on new assumptions and for providers to start having in-depth discussions about nonfinancial factors as a routine part of their break- even analysis. Assessing the New Backdrop Many trends that are reshaping the healthcare environment have a direct effect on equipment and technology decisions. Outcomes-based payment. As payment is increasingly linked to outcomes, providers are considering investments in technologies with proven clinical benefits that can help reduce length of stay, improve patient safety, and reduce readmissions. Population demographics. As a prerequisite to determining how to reduce costs of care while managing population health, providers are seeking to better understand the demographics, health status, and projected health utilization of the populations in their service areas. The changing nature of competition. As hospitals consolidate and health systems get bigger, these organizations are becoming sensitive about competing with other providers within their own networks (geographical competition), especially when it comes to acquisition of expensive, cutting-edge imaging or surgical technologies. The pricing package. Realizing that it is difficult to commit to capital investments during times of change, vendors have become increasingly sophisticated at shifting prices and revenue among capital, consumables, and service, seeking to maintain perceived equipment affordability up-front while locking in downstream revenues and margins. Therefore, providers should move beyond capital considerations and include discussion of service contracts and the cost of consumables over the lifetime of the equipment in their negotiations with vendors. Against that backdrop, the new break-even analysis may consider four main factors:. Cost . Utilisation . Payment and margins . Clinical considerations Cost Although capital outlay typically represents a large percentage of up-front costs associated with a new technology, other expenditures also should be considered when projecting true costs or comparing technologies. These include the cost of capital, labor, consumables, service, and length of stay (LOS). Capital. With the exception of unique technologies, today's healthcare supply-side marketplace is very competitive. Multiple configurations, installation, and discounting have resulted in significant variations in pricing. making pricing less transparent. Health systems have begun to pool their purchasing power to achieve price concessions from vendors. Even though capital cost increases have tracked closely with the consumer price index, expenses are shifting to consumables and service. Vendors are beginning to make technologies more dependent on consumables, thereby increasing the overall cost of a technology. It is therefore important to consider consumables and service when developing a business plan for a new technology. Labor. Labor can be one of the most significant cost factors in a break-even analysis. Labor is a key cost factor for any clinical technology or IT investment. Overall, labor-including benefit costs-makes up approximately 50 percent of a hospital's expenses. This portion includes overhead labor, such as administrative and medical records staff, which can add 10 to 20 percent to the cost of a test or procedure, as well as clinical labor. Although vendors are developing less labor-intensive technologies designed to promote efficiency, these technologies do not always translate to reduced labor costs. Consumables. Consumables represent the next largest line item for hospitals. Sixty percent of a hospital's consumables fall into the areas of cardiology, pharmacy, and surgery, which thus have a large impact on cost per patient or procedure. Along with physician preference items and supplies, many consumables that are dedicated to a capital purchase should be taken into consideration. For example, imaging dyes can range from $40 to $80 per patient, which translates to a cost of $ 100,000 to $200,000 per year for a hospital that does, on average, 2,500 imaging studies per year. Some consumables have a low unit cost, but their high volume results in significant expenditures. For example, infusion pump tubing may cost only $8 per patient, but a facility with 100 pumps would spend more than $160,000 per year on tubing alone, assuming an average of 200 patients using each pump annually. Consumable costs can vary dramatically between vendors and technologies. Many vendors tie their capital technologies to specific consumable revenue streams. Be aware that some vendors use the "razor/razorblade" model, in which the capital outlay for a piece of equipment is relatively low, but the buyer is then locked into buying a steady stream of disposables from that vendor. The consumable costs of basic standard-of care technologies, such as IV therapy and pulse oximetry, are far higher over their lifetime than the original capital outlay. In the clinical laboratory arena, consumables represent a $7.8 billion market per year, dwarfing the capital side. Advanced systems, such as robotics or lasers, add a premium to their consumables in the form of a per-patient royalty. These costs should be determined up front. Service. Service can have a significant impact on overall equipment and technology costs over the equipment's life cycle. Each year, the healthcare industry spends more than $14 billion providing service on medical technology, accounting for 3 to 7 percent of original technology costs per year. For low-utilization technologies, that can determine whether a break-even point is reached over the lifetime of a purchase.To put this in perspective, the service cost for a $200,000 ultrasound machine is more than $10,000 per year. Based on a five-year life, this amounts to a $40,000 line item or 20 percent of the equipment costs. For other systems such as a CT scanner, MRI scanner, or instrument washer, service can account for 40 percent of total cost. Given the high-tech, software-driven nature of current medical technology, service costs have been increasing Multiple service options are available; the key for the hospital is to balance the dual objectives of reducing costs and safeguarding outcomes. The manufacturer's full-service contract represents the high end of service costs. It is generally best to figure half or two-thirds of the manufacturer's service contract cost when creating a budget. In lieu of service contracts, hospitals may use their in-house clinical engineering staff to service equipment or may elect to pay for service on a time-and-materials basis. LOS. Technology developers are concentrating on less invasive technology that has the potential to reduce operating room (OR) time, recovery time, and LOS. The challenge is determining the extent to which a new technology actually does reduce LOS and OR time. Peer-reviewed journals are an excellent resource for determining how a technology can affect LOS and OR time. Factoring in LOS or OR times can be tricky as pricing standards in the industry can vary. In general, for inpatient procedures, the patient's projected LOS should be based on the geometric LOS for each DRG provided by the Centers for Medicare & Medicaid Services (CMS). A good guide for internal cost is $500 per day for nursing units and $1,200 to $3,000 for critical care, with the high end of the critical care range representing patients receiving ventilator support. For outpatient procedures, $600 represents a good high mark for a 23-hour stay, and for less than 23 hours, fractions of that amount can be used. The standard value for the cost of OR time is approximately $30 to $50 per minute, taking into account the cost of room, light, tables, and support services, although for cardiovascular procedures, per-minute cost can be $60 or more. For outpatient centers, it is usually slightly lower. Utilization Utilisation has a direct effect on break-even points and profit margins. Traditionally, utilization projections have come from physician input and historical data, but projecting a break-even point offers a more effective way to determine utilization. It reverse-engineers utilization by taking cost and revenue numbers and calculating how many procedures must be performed for a new technology to yield a profit. This can help a provider determine the financial viability of a particular technology based on its own numbers. It should not, however, be used to set a target volume the hospital needs to meet in order to make a technology affordable. Under the Taxpayer Relief Act of 1997, CMS has tied payment rates for high-end imaging (c.g, CT, MRI, positron emission tomography) to utilization. In 2010, the utilization rate requirement was increased from 50 percent to 60 percent. To receive full payment in 2013, hospitals will have to use their systems 90 percent of the time. To put this into perspective, a facility that would have needed 4,000 patients per year under the 50 percent rate to achieve break-even status would need 7,000 patients per year under the 90 percent rule. Technology life expectancy. Equipment lifespan is an important data point for determining the viability of a technology. Most facilities use the American Hospital Association's Guide to the Estimated Useful Lives of Depreciable Hospital Assets as a benchmark. This guide, which was published in 2008, projects the life of an asset until a major upgrade is required. However, there are discrepancies between the published numbers and real-world experience. For example, the guide rates the life expectancy of robotic equipment at seven years, but we have yet to see a system in place more than five years without a major upgrade. In our survey research, most CFOs target a payback period of one to two years, well below the projected life of the equipment.Payment and Profit Margins The Affordable Care Act includes two key provisions-"never events" and payment reductions for readmissions that now tie payment to outcomes and allow CMS to impose steep financial penalties on providers. Such outcome-based payments can make projecting revenue from a technology more complicated as they are really cost-avoidance considerations and not as straightforward as other components in the break-even calculator. Average CMS payment provides a good guide when determining the effect of payment on a purchasing decision. Although Medicare payment historically reflected a worst-case scenario, private payers no longer reimburse at significantly higher levels than Medicare; in some geographic locations, private payer reimbursement may even be lower than Medicare rates. Clinical Considerations As CMS transitions from volume-based to outcomes-based payment, hospitals are seeking ways to deliver better care while holding the line on costs. Value analysis teams working across department lines now consider the impact of any new technology decision on LOS, infection control, and hospital readmissions. In addition, providers should address population and geographical concerns, which dictate payment and volumes for specific procedures. Competition is an important factor; not every urban center can support multiple specialized physician practices or specialized technology such as robotic surgery systems, proton beam therapy, and hybrid ORs. Population demographics. Although population demographics often are left out of discussions about new technology acquisitions, demographics are highly relevant to technology decisions. In areas that serve a large percentage of non-Medicare patients, labor and delivery is likely to account for the top six of the 10 most common DRGs. In comparison, providers that serve a high percentage of Medicare patients find that pneumonia, chronic obstructive pulmonary discase, heart failure, and joint replacement are among the most common DR.Gs. Geographic competition. In addition to competing with other providers for patients and for physician services, hospitals and health systems need also be sensitive about competing within their own networks. Major capital purchases at the corporate level that impact an entire service line should now take into consideration not only a hospital's traditional geographic service area but also how the purchase will affect the network or hospital system A break-even calculator that takes into account financial and clinical considerations is a valuable tool that can allow a hospital to strategically invest in technology that can combine improved outcomes, efficiency, and margins in a way that is right for a particular hospital or health system, as the examples in the following sections show. The Example of Robotics According to a robotic surgery equipment manufacturing report, industry revenue derived from robotic treatments is projected to increase at an average annual rate of 14.9 percent to $4.2 billion from 2011 to 2016 (IBISWorld, Robotic Surgery Equipment Manufacturing in the U.S.: Market Research Report, October 201 1). Both soft tissue and orthopedic robotic treatments therefore should be key areas of interest for hospital administrators. Utilization of robotic surgery for knee and hip replacements is of particular relevance, given that 719,000 total knee replacements and 332,000 total hip replacements were performed in the United States in 2010, according to the Centers for Discase Control and Prevention/National Center for Health Statistics 2010 National Hospital Discharge Survey.Treatment options, including robotic surgery, image-guided surgery (IGS), and manual techniques, vary in terms of durability. Studies have found that alignment errors greater than 3 percent in artificial knee procedures are associated with implant failures. Conventional manual techniques had a nearly 32 percent chance of a greater- than- 3 percent misalignment, while this number decreased to 9 percent in cases when an IGS was used. In contrast, surgical orthopedic robots were able to achieve consistent alignment. "This translates into a more durable procedure. As a guide, using IGS technology and standard implant pricing, a hospital that performs 240 procedures per year over a five-year period could net more than $2 million in profits, as shown in the exhibit on page 92. In contrast, a provider with the same procedure volume using robotic technology would lose $285,000 over that period. To break even using robotics, a hospital would have to perform 300 procedures per year. At first glance, it would appear that orthopedic robotic technology is not the best approach, from a financial standpoint. However, unlike IGS, robotic surgery is an appropriate treatment option for younger patients, which should translate into higher utilization rates. Such considerations should open up an important discussion about the effects of patient demographics and geographical considerations when selecting technology. In an area with a high Medicare patient population, IGS might be ideal In an area with more young patients, robotic surgery would be a more viable option in part due to the high accuracy of robotic surgeries, which extends the life of the implant. Robotic technology also can perform custom partial knee resurfacing, giving younger patients an option other than joint replacement for surgical treatment of arthritis. It should be noted that robotic surgery is still in the early stages of application and might not be suitable for every hospital in a network. Exhibit 1 The Example of Prostate Surgery For years, transurethral resection of the prostate (TURP) was the standard of care for benign prostatic hyperplasia (BPH), a common condition in older men. The carly 1990s saw the introduction of the Nd YAG laser as a treatment option for BPH and by the mid-2000s, photoselective vaporization of the prostate (PVP) through the KTP laser became available on the market. Compared with TURP, PVP represented a considerable investment in capital and consumables. Studies also have found that although PVP has a slightly longer procedure time, both YAG and TURP require a longer LOS and catheterization time." When PVP first hit the market, CMS reimbursed the technology at a rate more than twice that of TURP because PVP resulted in fewer complications, such as bleeding during surgery, erectile dysfunction, and urinary incontinence after surgery, than TURP. Today, under Ambulatory Payment Classification (APC) 429 (laser surgery of the prostate), payment for PVP is $3,261. By comparison, the total cost of TURP ranges from $2,400 to $2,800 under APC 163 (prostatectomy with TURP), which gives providers the potential to generate margins of $230 per case based on 200 procedures per year for five years. Based on these numbers, PVP would generate far smaller margins ($100,000) over five years than would TURP ($305,000) as a result of thelower cost of consumables associated with TURP. PVP would also generate smaller margins than the YAG laser ($709,000), making the use of PVP questionable from a financial standpoint, as shown in the exhibit below. Exhibit 2 Although these numbers seem to make a case for TURP or YAG, patient outcomes and patient satisfaction also play a factor in payment and utilization of any technology. The superior clinical outcomes associated with PVP open up this procedure to a larger volume of patients. Additionally, the lower incidence of complications for minimally invasive laser procedures has driven informed patients to push for use of these procedures. However, a single facility may not be able to hit the PVP break-even point of 120 patients per year. In this case, a business plan based on multiple facilities feeding into one geographic center of excellence might be the answer. Expanding the Framework As the contribution of equipment and technology to patient outcomes is called into question, hospitals and health systems will want to expand their break-even analysis to take the full range of financial and nonfinancial factors into consideration. It is incumbent on healthcare finance leaders not only to expand their break-even calculators to include the quantifiable factors, but also to engage in discussions about the role of a new technology or equipment in an increasingly value-based world. James Laskaris, EE, BME, is a senior emerging technology analyst, MD Buyline, Dallas. Katic Regan is a clinical publishing analyst, MD Buyline, Dallas. footnotes a. Moon, Y.W., Ha, C.W., Do, K.H., et al, "Comparison of Robot-Assisted and Conventional Total Knee Arthroplasty: A Controlled Cadaver Study Using Multiparameter Quantitative Three-Dimensional CT Assessment of Alignment," Computer Aided Surgery, March 2012. b. Al-Ansari, A., Younes, N., Sampige, V.P., et al, "GreenLight HPS 120-W Laser Vaporization Versus Transurethral Resection of the Prostate for Treatment of Benign Prostatic Hyperplasia: A Randomized Clinical Trial with Midterm Follow-Up," European Urology. Sept. 2010, pp. 349-355. Publication Date: Monday, December 02, 2013

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance