Answered step by step

Verified Expert Solution

Question

1 Approved Answer

from this case study what is 1-objective 2-issue 3- literature review 4- Results 5- conclusion A Note on a Contribution Margin Approach to the Analysis

from this case study what is 1-objective 2-issue 3- literature review 4- Results 5- conclusion

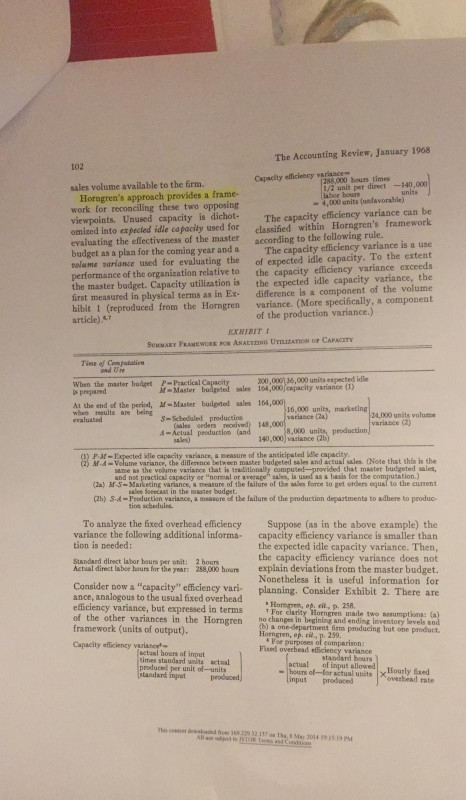

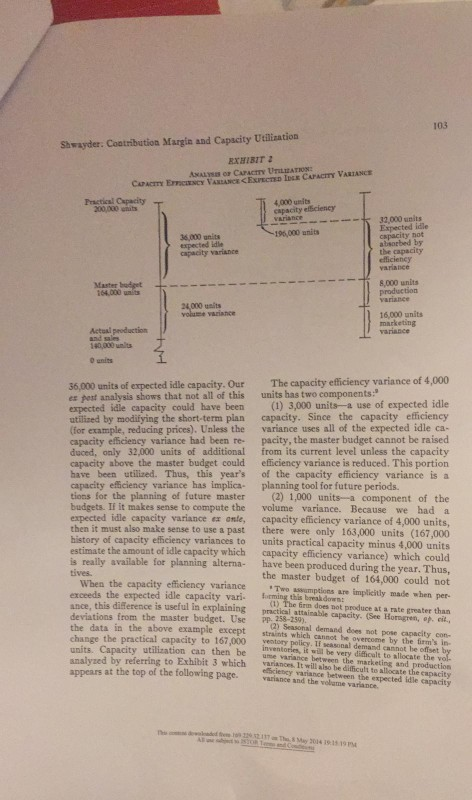

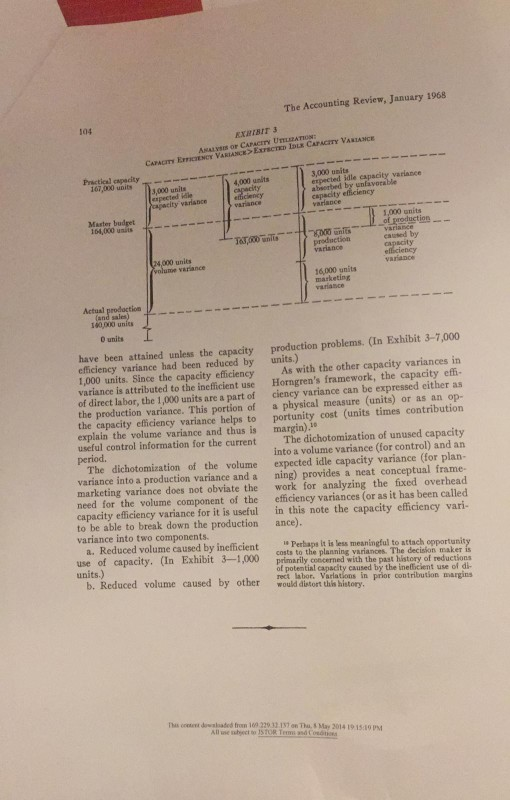

A Note on a Contribution Margin Approach to the Analysis of Capacity Utilization Keith Shwayder Nickerson offers several good argu- TNS article in the April 1967 issue of The Accounting Review, Horngrentments for computing the fixed cost effi- seemingly proposed the elimination of ciency variance, one of which is especially the fixed overhead efficiency variance: interesting,"... for the short-run at least, "... short-run fixed overhead cost incur. variances in the efficiency of labor are not rence is not affected by efficiency. More oing to change the amount of a com- over, the managers responsible for in- pany's fixed burden, though in time, of efficiency will be aware of its existence course, if labor becomes less and less effi through reports on variable cost control; so cient it will take either more equipment or there is little additional management in more automatic, and therefore more ex- formation to be gained from expressing pensive equipment to maintain output." ineffective utilization of fixed factory over- One extension of this argument is as fol- head factors in historical dollar terms." lows: although currently the fixed over- However, on closer examination, it appears head efficiency variances may not be an that Horngren has instead established a economic cost to the firm, at some future framework for giving the fixed overhead time when the master sales budget is closer efficiency variance a conceptual clarity to practical capacity, the fixed overhead lacking in previous approaches to fixed efficiency variance may act as a constraint cost analysis. on the firm's output and thus reduce the There is no evident consensus among countants as to the usefulness of Charles Horngren, "A Contribution Margin Ap- proach to the Analysis of Capacity Utilization THE computing the fixed overhead efficiency ACCOUNTING REVIEW, April 1967, pp. 254-264 Toid. p. 257. ence Backer and Jacobsen summarize Morton Backer and Lyle Jacobsen Cost the argument against determining this A Managerial Approach McGraw-Hill Book Company, Inc., 1964). p. 296. dan "The efficiency variance is based "Clarence Nickerson, and on the assumption that a real loss in the Cew Art end Analysis (McGraw naerial Coul Accounting . pp. 325-327 use of fixed facilities occurs as a con- I . p. 326. sequence of labor inefficiency. This would only occur under the rare circumstances where a plant operates at maximum and Analysis (McGrawital Book Company, Inc., 1954) capacity." Keith Slwayder is Instructor in Ac counting at the University of Chicago. 101 Douma HHH NH HNG New er ma s TH Thu H 14 115 16 and Confes reuma units 102 The Accounting Review, January 1968 Capacity efficiency sales volume available to the firm. O ur times 1/2 unit per direct--140,000 Horngren's approach provides a frame- later hours work for reconciling these two opposing -4,000 units un lavorable) viewpoints. Unused capacity is dichot- The capacity efficiency variance can be omised into expected idle capacity used for classified within Horngren's framework evaluating the effectiveness of the master according to the following rule. budget as a plan for the coming year and a The capacity efficiency variance is a use Dolume variance used for evaluating the of expected idle capacity. To the extent performance of the organization relative to the capacity efficiency variance exceeds the master budget. Capacity utilization is the expected idle capacity variance, the first measured in physical terms as in Ex. difference is a component of the volume hot 1 (reproduced from the Horngren variance. (More specifically, a component article).67 of the production variance.) EXHIBITI SUMMARY PRAMEWORK FOR AALTING UTILIZATION OF CAPACITY Time of Cepaties When the master budget Practical Capacity 200,000 36,000 units expected idle s prepared M Master budgeted sales 164,000 capacity variatice (1) At the end of the period, M-Master budgeted sales 164,000 whes results are being 516,000 units, marketing evaluated 3-Scheduled production 124.000 units volume variance (2) 38.000 units, production t variance (2) Actual production and rech race () (I) P E xpected Wle capacity variance, mesure of the anticipated de capacity. (2) M-1-Volume variance, the difference between master budgeted sales and Netual sales. (Note that this is the same as the volume variance that is traditionally computed-provided that master budgeted sales, and not practical capacity or normal or average und as a basis for the computation) (2) M S-Marketing variance, a measure of the failure of these force to get onders equal to the current sales forces in the water budget. (26) S-4-Production variance, care of the failure of the production departments to adhere to produce To analyze the fixed overhead efficiency variance the following additional informa tion is needed: Standard direct labor hours per unit: Actual direct labee hours for the year 2 hours 288,000 hours Consider now a "capacity" efficiency vari- ance, analogous to the usual fixed overhead efficiency variance, but expressed in terms of the other variances in the Horngren framework (units of output) Capacity efficiency var actual hours of input times standard with produced per unit of units standard input produced Suppose (as in the above example) the capacity efficiency variance is smaller than the expected idle capacity variance. Then, the capacity efficiency variance does not explain deviations from the master budget. Nonetheless it is useful information for planning. Consider Exhibit 2. There are Horren, op. cit., p. 258. For clarity Horngren made two sumptions: (a) to changes in begining and ending inventory levels and (b) a one-department firm producing but one product. Horngren, op. cit., p. 259. For purposes of comparison: Hued overhead ciency variance standard hours ac fingulosed bons of or custo l y input d produced overhead rate rate and the 103 Shwayder: Contribution Margin and Capacity Utilisation 2 ANAL O CAPACITY UTILLATION NCY VARANCE EXPECTED I CAPACITY VARIANCE CAPACITY E Practical Capacity 200,000 stats 4.000 units capacity efficiency Variance 196,000 units 36 000 units expected die capacity are 32 000 units Expected idle capacity tot absorbed by the capacity efficiency Master baget 8.000 units production 16.00 24.000 units volume variance 16.000 units marketing variance Actual production nis 36,000 units of expected idle capacity. Our e past analysis shows that not all of this expected idle capacity could have been utlined by modifying the short-term plan (for example, reducing prices). Unless the capacity efficiency variance had been re- duced, only 32,000 units of additional capacity above the master budget could have been utilized. Thus, this year's capacity efficiency variance has implica- tions for the planning of future master budgets. If it makes sense to compute the expected idle capacity variance ex ante, then it must also make sense to use a past history of capacity efficiency variances to estimate the amount of idle capacity which is really available for planning alterna- tives When the capacity efficiency variance exceeds the expected idle capacity vari ince, this difference is useful in explaining deviations from the master budget. Use the data in the above example except change the practical capacity to 167,000 units. Capacity utilization can then be lysed by referring to Exhibit 3 which appears at the top of the following page. The capacity efficiency variance of 4,000 units has two components: (1) 3,000 units a use of expected idle capacity. Since the capacity efficiency variance uses all of the expected idle ca. pacity, the master budget cannot be raised from its current level unless the capacity efficiency variance is reduced. This portion of the capacity efficiency variance is a planning tool for future periods. (2) 1,000 units-a component of the volume variance. Because we had a capacity efficiency variance of 4,000 units, there were only 163,000 units (167,000 units practical capacity minus 4,000 units capacity efficiency variance) which could have been produced during the year. Thus, the master budget of 164,000 could not T u mptions are implicitly made when per (1) The firm does not produce at a rate practical attainable capacity. (See Horgen, ter than t. pp. 258-259) 2) Seasonal demand does not pose capacity co- straints which cannot be overcome by the ventory policy. If 's in al demand cannot be inventories, it will be very set by me variance between the marketing and production cult to allocate the vol variances. It will also be difficult to l Sciency variance between the expected de capacity focate the capacity ate v e nd the volume variante The The Accounting Review, January 1968 EXIBIT 3 A S O CAPACITY UMATION ROY VARIANCE Echo Lux Car ACITY VARIANCE CAME Practical capacity 13,000 units le 4,000 units capacity efficiency aspected 3.000 units Il espected idle capacity variance > h ted by unfavorable capacity efficiency Varance 1.000 units of production Onits Variance production caused by Master budget 164,000 units Vrance 000 units volume variance 16.000 units marketing Actual production | and sales) have been attained unless the capacity efficiency variance had been reduced by 1,000 units. Since the capacity efficiency variance is attributed to the inefficient use of direct labor, the 1,000 units are a part of the production variance. This portion of the capacity efficiency variance helps to explain the volume variance and thus is useful control information for the current period. The dichotomization of the volume variance into a production variance and a marketing variance does not obviate the need for the volume component of the capacity efficiency variance for it is useful to be able to break down the production variance into two components. a. Reduced volume caused by inefficient use of capacity. (In Exhibit 3-1,000 units.) b. Reduced volume caused by other production problems. (In Exhibit 3-7,000 units.) As with the other capacity variances in Horngren's framework, the capacity of ciency variance can be expressed either as a physical measure (units) or as an op portunity cost (units times contribution margin). The dichotomization of unused capacity into a volume variance for control) and an expected idle capacity variance (for plan- ning) provides a neat conceptual frame- work for analyzing the fixed overhead efficiency variances (or as it has been called in this note the capacity efficiency vari- ance). 1 Perhaps it is less meaningful to attach opportunity costs to the planning variances. The decision maker is primarily concerned with the past history of reductions of potential capacity caused by the ineficient use of di- rect labor, Variations in prior contribution margins would distort this history, The towed from 10.2017 on Thu May 2014 10 15 All STOR TEC A Note on a Contribution Margin Approach to the Analysis of Capacity Utilization Keith Shwayder Nickerson offers several good argu- TNS article in the April 1967 issue of The Accounting Review, Horngrentments for computing the fixed cost effi- seemingly proposed the elimination of ciency variance, one of which is especially the fixed overhead efficiency variance: interesting,"... for the short-run at least, "... short-run fixed overhead cost incur. variances in the efficiency of labor are not rence is not affected by efficiency. More oing to change the amount of a com- over, the managers responsible for in- pany's fixed burden, though in time, of efficiency will be aware of its existence course, if labor becomes less and less effi through reports on variable cost control; so cient it will take either more equipment or there is little additional management in more automatic, and therefore more ex- formation to be gained from expressing pensive equipment to maintain output." ineffective utilization of fixed factory over- One extension of this argument is as fol- head factors in historical dollar terms." lows: although currently the fixed over- However, on closer examination, it appears head efficiency variances may not be an that Horngren has instead established a economic cost to the firm, at some future framework for giving the fixed overhead time when the master sales budget is closer efficiency variance a conceptual clarity to practical capacity, the fixed overhead lacking in previous approaches to fixed efficiency variance may act as a constraint cost analysis. on the firm's output and thus reduce the There is no evident consensus among countants as to the usefulness of Charles Horngren, "A Contribution Margin Ap- proach to the Analysis of Capacity Utilization THE computing the fixed overhead efficiency ACCOUNTING REVIEW, April 1967, pp. 254-264 Toid. p. 257. ence Backer and Jacobsen summarize Morton Backer and Lyle Jacobsen Cost the argument against determining this A Managerial Approach McGraw-Hill Book Company, Inc., 1964). p. 296. dan "The efficiency variance is based "Clarence Nickerson, and on the assumption that a real loss in the Cew Art end Analysis (McGraw naerial Coul Accounting . pp. 325-327 use of fixed facilities occurs as a con- I . p. 326. sequence of labor inefficiency. This would only occur under the rare circumstances where a plant operates at maximum and Analysis (McGrawital Book Company, Inc., 1954) capacity." Keith Slwayder is Instructor in Ac counting at the University of Chicago. 101 Douma HHH NH HNG New er ma s TH Thu H 14 115 16 and Confes reuma units 102 The Accounting Review, January 1968 Capacity efficiency sales volume available to the firm. O ur times 1/2 unit per direct--140,000 Horngren's approach provides a frame- later hours work for reconciling these two opposing -4,000 units un lavorable) viewpoints. Unused capacity is dichot- The capacity efficiency variance can be omised into expected idle capacity used for classified within Horngren's framework evaluating the effectiveness of the master according to the following rule. budget as a plan for the coming year and a The capacity efficiency variance is a use Dolume variance used for evaluating the of expected idle capacity. To the extent performance of the organization relative to the capacity efficiency variance exceeds the master budget. Capacity utilization is the expected idle capacity variance, the first measured in physical terms as in Ex. difference is a component of the volume hot 1 (reproduced from the Horngren variance. (More specifically, a component article).67 of the production variance.) EXHIBITI SUMMARY PRAMEWORK FOR AALTING UTILIZATION OF CAPACITY Time of Cepaties When the master budget Practical Capacity 200,000 36,000 units expected idle s prepared M Master budgeted sales 164,000 capacity variatice (1) At the end of the period, M-Master budgeted sales 164,000 whes results are being 516,000 units, marketing evaluated 3-Scheduled production 124.000 units volume variance (2) 38.000 units, production t variance (2) Actual production and rech race () (I) P E xpected Wle capacity variance, mesure of the anticipated de capacity. (2) M-1-Volume variance, the difference between master budgeted sales and Netual sales. (Note that this is the same as the volume variance that is traditionally computed-provided that master budgeted sales, and not practical capacity or normal or average und as a basis for the computation) (2) M S-Marketing variance, a measure of the failure of these force to get onders equal to the current sales forces in the water budget. (26) S-4-Production variance, care of the failure of the production departments to adhere to produce To analyze the fixed overhead efficiency variance the following additional informa tion is needed: Standard direct labor hours per unit: Actual direct labee hours for the year 2 hours 288,000 hours Consider now a "capacity" efficiency vari- ance, analogous to the usual fixed overhead efficiency variance, but expressed in terms of the other variances in the Horngren framework (units of output) Capacity efficiency var actual hours of input times standard with produced per unit of units standard input produced Suppose (as in the above example) the capacity efficiency variance is smaller than the expected idle capacity variance. Then, the capacity efficiency variance does not explain deviations from the master budget. Nonetheless it is useful information for planning. Consider Exhibit 2. There are Horren, op. cit., p. 258. For clarity Horngren made two sumptions: (a) to changes in begining and ending inventory levels and (b) a one-department firm producing but one product. Horngren, op. cit., p. 259. For purposes of comparison: Hued overhead ciency variance standard hours ac fingulosed bons of or custo l y input d produced overhead rate rate and the 103 Shwayder: Contribution Margin and Capacity Utilisation 2 ANAL O CAPACITY UTILLATION NCY VARANCE EXPECTED I CAPACITY VARIANCE CAPACITY E Practical Capacity 200,000 stats 4.000 units capacity efficiency Variance 196,000 units 36 000 units expected die capacity are 32 000 units Expected idle capacity tot absorbed by the capacity efficiency Master baget 8.000 units production 16.00 24.000 units volume variance 16.000 units marketing variance Actual production nis 36,000 units of expected idle capacity. Our e past analysis shows that not all of this expected idle capacity could have been utlined by modifying the short-term plan (for example, reducing prices). Unless the capacity efficiency variance had been re- duced, only 32,000 units of additional capacity above the master budget could have been utilized. Thus, this year's capacity efficiency variance has implica- tions for the planning of future master budgets. If it makes sense to compute the expected idle capacity variance ex ante, then it must also make sense to use a past history of capacity efficiency variances to estimate the amount of idle capacity which is really available for planning alterna- tives When the capacity efficiency variance exceeds the expected idle capacity vari ince, this difference is useful in explaining deviations from the master budget. Use the data in the above example except change the practical capacity to 167,000 units. Capacity utilization can then be lysed by referring to Exhibit 3 which appears at the top of the following page. The capacity efficiency variance of 4,000 units has two components: (1) 3,000 units a use of expected idle capacity. Since the capacity efficiency variance uses all of the expected idle ca. pacity, the master budget cannot be raised from its current level unless the capacity efficiency variance is reduced. This portion of the capacity efficiency variance is a planning tool for future periods. (2) 1,000 units-a component of the volume variance. Because we had a capacity efficiency variance of 4,000 units, there were only 163,000 units (167,000 units practical capacity minus 4,000 units capacity efficiency variance) which could have been produced during the year. Thus, the master budget of 164,000 could not T u mptions are implicitly made when per (1) The firm does not produce at a rate practical attainable capacity. (See Horgen, ter than t. pp. 258-259) 2) Seasonal demand does not pose capacity co- straints which cannot be overcome by the ventory policy. If 's in al demand cannot be inventories, it will be very set by me variance between the marketing and production cult to allocate the vol variances. It will also be difficult to l Sciency variance between the expected de capacity focate the capacity ate v e nd the volume variante The The Accounting Review, January 1968 EXIBIT 3 A S O CAPACITY UMATION ROY VARIANCE Echo Lux Car ACITY VARIANCE CAME Practical capacity 13,000 units le 4,000 units capacity efficiency aspected 3.000 units Il espected idle capacity variance > h ted by unfavorable capacity efficiency Varance 1.000 units of production Onits Variance production caused by Master budget 164,000 units Vrance 000 units volume variance 16.000 units marketing Actual production | and sales) have been attained unless the capacity efficiency variance had been reduced by 1,000 units. Since the capacity efficiency variance is attributed to the inefficient use of direct labor, the 1,000 units are a part of the production variance. This portion of the capacity efficiency variance helps to explain the volume variance and thus is useful control information for the current period. The dichotomization of the volume variance into a production variance and a marketing variance does not obviate the need for the volume component of the capacity efficiency variance for it is useful to be able to break down the production variance into two components. a. Reduced volume caused by inefficient use of capacity. (In Exhibit 3-1,000 units.) b. Reduced volume caused by other production problems. (In Exhibit 3-7,000 units.) As with the other capacity variances in Horngren's framework, the capacity of ciency variance can be expressed either as a physical measure (units) or as an op portunity cost (units times contribution margin). The dichotomization of unused capacity into a volume variance for control) and an expected idle capacity variance (for plan- ning) provides a neat conceptual frame- work for analyzing the fixed overhead efficiency variances (or as it has been called in this note the capacity efficiency vari- ance). 1 Perhaps it is less meaningful to attach opportunity costs to the planning variances. The decision maker is primarily concerned with the past history of reductions of potential capacity caused by the ineficient use of di- rect labor, Variations in prior contribution margins would distort this history, The towed from 10.2017 on Thu May 2014 10 15 All STOR TECStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting For Inventory

Authors: Steven M. Bragg

2nd Edition

1938910648, 9781938910647