Answered step by step

Verified Expert Solution

Question

1 Approved Answer

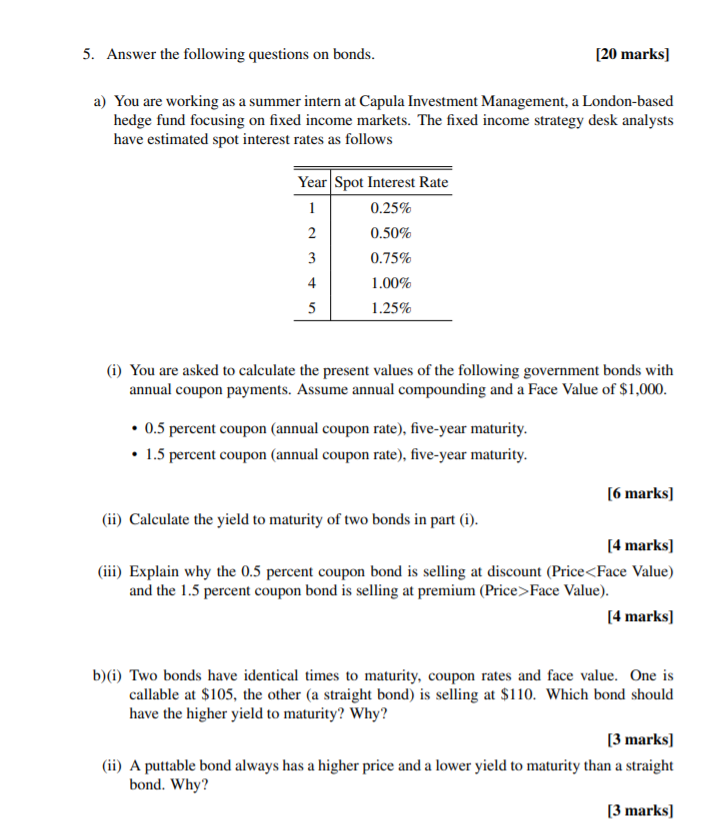

full working all parts no excel 5. Answer the following questions on bonds. [20 marks] a) You are working as a summer intern at Capula

full working all parts no excel

5. Answer the following questions on bonds. [20 marks] a) You are working as a summer intern at Capula Investment Management, a London-based hedge fund focusing on fixed income markets. The fixed income strategy desk analysts have estimated spot interest rates as follows Year Spot Interest Rate 1 0.25% 2 0.50% 3 0.75% 4 1.00% 5 1.25% (i) You are asked to calculate the present values of the following government bonds with annual coupon payments. Assume annual compounding and a Face Value of $1,000. 0.5 percent coupon (annual coupon rate), five-year maturity. 1.5 percent coupon (annual coupon rate), five-year maturity. [6 marks) (ii) Calculate the yield to maturity of two bonds in part (i). [4 marks) (iii) Explain why the 0.5 percent coupon bond is selling at discount (Price

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Tail Risk Hedging Creating Robust Portfolios For Volatile Markets

Authors: Vineer Bhansali

1st Edition

0071791752,0071791760