Question

Refer to exhibit 14.4. What is the value of a synthetic stock created with put and call options that expire in six months with an

Refer to exhibit 14.4. What is the value of a synthetic stock created with put and call options that expire in six months with an expiration price of $50?

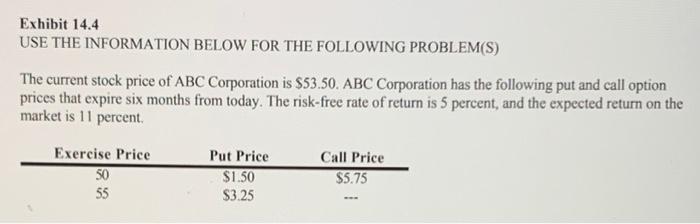

Exhibit 14.4 USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S) The current stock price of ABC Corporation is $53.50. ABC Corporation has the following put and call option prices that expire six months from today. The risk-free rate of return is 5 percent, and the expected return on the market is 11 percent. Exercise Price 50 8 55 Put Price $1.50 $3.25 Call Price $5.75

Step by Step Solution

3.46 Rating (156 Votes )

There are 3 Steps involved in it

Step: 1

Given Information Exercise Price K 50 Call Price c 575 Put Pr...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles of Marketing

Authors: Philip Kotler, Gary Armstrong

16th edition

978-0133850758, 133850757, 133795020, 978-0133795028