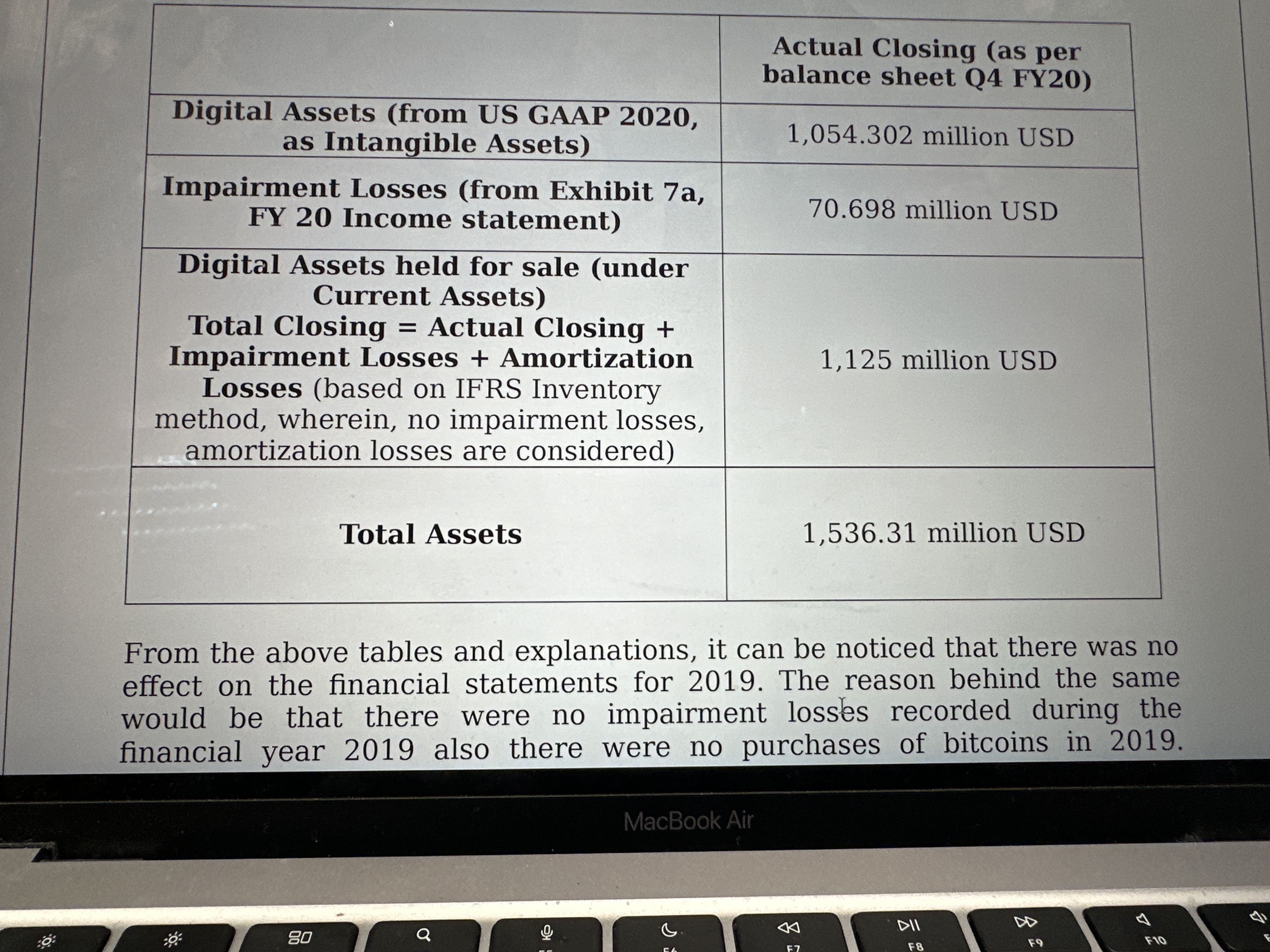

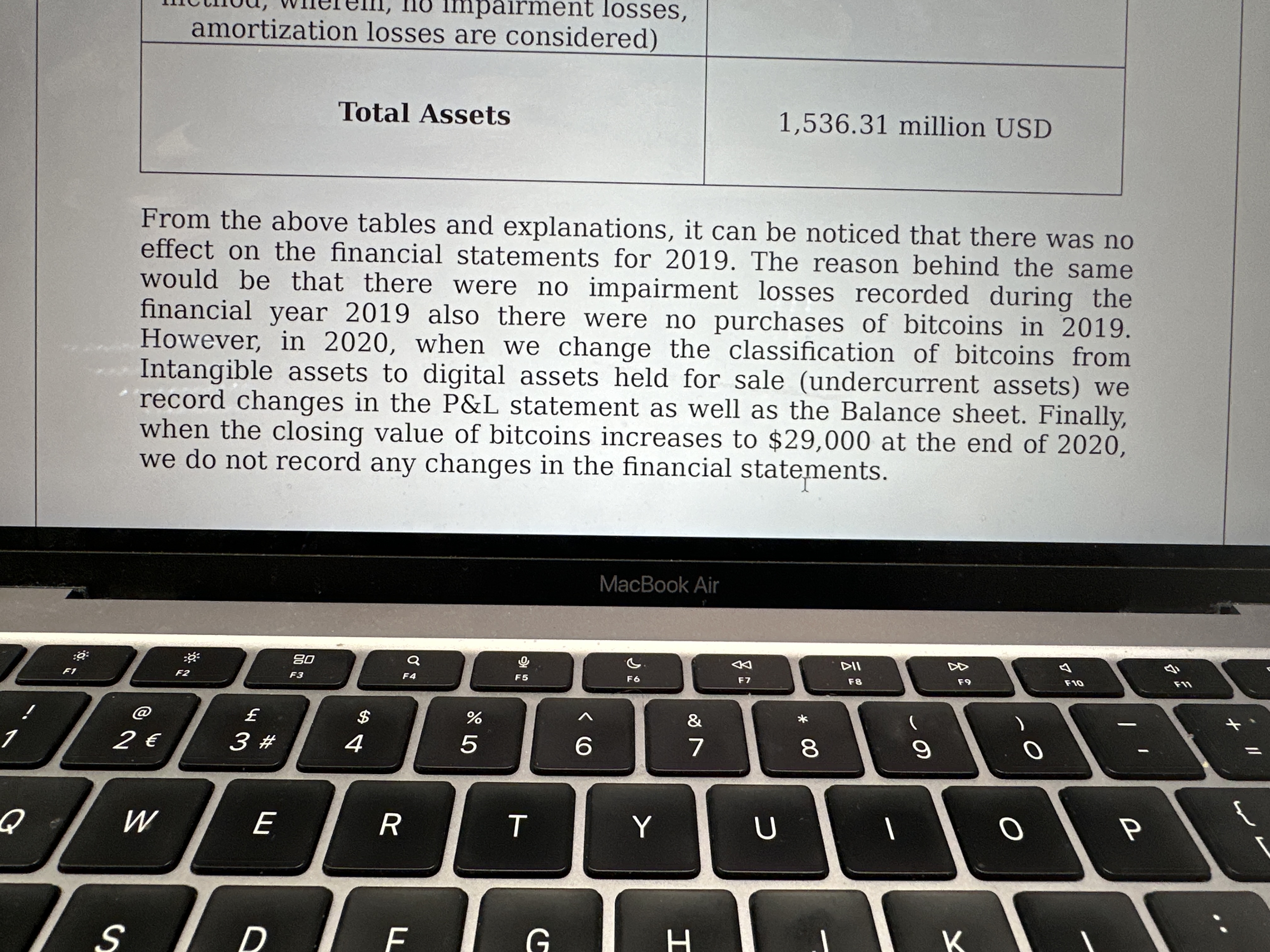

GAAP ) and as (11) part of Inventory (using IFRS standards). 4. How would be accounting for Bitcoin as inventory under IFRS affects MicroStrategy's financial

GAAP ) and as (11) part of Inventory (using IFRS standards). 4. How would be accounting for Bitcoin as inventory under IFRS affects MicroStrategy's financial statements in 2020? Note that MicroStrategy owned 70,409 bitcoins at the end of fiscal year 2020, and each bitcoin had cost $16,109 on average. The Bitcoin closing price on December 31, 2020, was $29,000. In the IFRS standards, cryptocurrencies such as bitcoin can be considered as inventory if it's held for sold in the regular course of business. For the given case, even though MicroStrategy is not planning to sell the bitcoins and planning to hold it (from the 10-K filings), we consider the bitcoins to be inventory. We will list down the changes which would occur if the standards used change from GAAP to IFRS 1. Income statement - Digital assets impairment losses (expenses) would be removed as its specific to the bitcoin being considered as an intangible asset (which would incur impairment losses and MacBook Air esc Q DII DD F6 FB F 10 F1 F3 FA F7 F9 F11 $ % #~ MicroStrategy: Ac... AFD_report_v2.do... x \\l L 1Cran rIU]C\\_I. @D w k@@@'\"%''? E/Zf}@('l am.ortization'costs (=0, as the bitcoin's life is considered infinite)) Th1 change in the impairment losses would reflect in the value of the digital assets, which in turn would reflect in the balance sheet. In IFRS 1nveqtory method, the actual income is considered as the reah_zed gains while the gains due to the increase in the profits are considered in the income statement as unrealized gains (which 1. would be Other Comprehensive Income, OCI, if we follow IFRS intangible assets method, 2. would not be considered if we follow GAAP). Also, the losses due to the reduction in the price of the inventory is captured as the unrealized losses, as an alternative to the impairment losses used in the GAAP method. . Balance sheet - In the balance sheet, previously the digital assets value was 1054.302 million USD, which would now become 1,125 million USD (which is the current assets = inventory = digital assets held for sale, as per IFRS inventory method) as the impairment losses for FY20 was 70.698 million USD. Because of the cascading effect, there will be a direct increase in the total assets, and the retained earnings. Thus, the Total assets = Total liabilities + Total stockholders' equity = 1536.31 million USD In the income statement, considering that the cost of revenue remains the same, the gross profit would remain unaffected, but the net income would be changed due to the removal of the impairment losses of 70.798 million e GEPTUR WD + 145% - In the income statement, considering that the cost of revenue remains the same, the gross profit would remain unaffected, but the net income would be changed due to the removal of the impairment losses of 70.798 million USD. Thus, the new net income would be 63.174 million USD. TABLE 4.1: EFFECT OF TREATING BITCOIN AS INVENTORY (IFRS) IN INCOME STATEMENT * In thousands USD 2020 GAAP 2020 IFRS Remarks / Inventory Assumption EO 480 Total Revenues 480,735 735 Unchanged Total Cost of 9 91,055 1,055 Unchanged Revenues 389 Gross Profit 389,680 680 Unchanged In intangible Changes in -70,698 to GAAP, Impairment Losses 000 Impairment MacBook Air DII DD A F12 20 Q S F10 F11 F3 F6 F7 F8 esc & @ % a 2 E 3 # 4 5 6> 2 Ac... . AFD_report_v2.do... x @O "n N BDOO w- K T @y losses are present, which is removed in IFRS inventory method Changed due to Total Operating reduction in Expenses 403,305 impairment losses Changed due to (Loss) Income from reduction in operations | impairment Changed due to | Net Loss (income) Considering the average value of Actual cost of buying 70409 coins @ $16109 mentioned from the case to arrive | at the actual cost | US GAAP 2020 nent Losses (from Exhibit 7a, 20 Income statement) 1 Assets held for sale (under Current Assets) tal Closmg Actual Closing + mpairment Losses + Amortization Losses (based on IFRS Inventory method, wherein, no impairment losses, amortization losses are considered) Total Assets 1,536.31 million 'the above tables and explanations, it can be noticed that on the financial statements for 2019. The reason behin e that there were no impairment losses rec ear 2019 also there were no purchase Ill, no impairment losses, amortization losses are considered) Total Assets 1,536.31 million USD From the above tables and explanations, it can be noticed that there was no effect on the financial statements for 2019. The reason behind the same would be that there were no impairment losses recorded during the financial year 2019 also there were no purchases of bitcoins in 2019. However, in 2020, when we change the classification of bitcoins from Intangible assets to digital assets held for sale (undercurrent assets) we record changes in the P&L statement as well as the Balance sheet. Finally, when the closing value of bitcoins increases to $29,000 at the end of 2020, we do not record any changes in the financial statements. MacBook Air DD DD F1 F4 F7 F10 F3 @ $ % 2 E 3 # 4 5 6 7 9 O Q W E R T Y U O P S D F H

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance