Question

Given numbers are the prices of 5-years zero coupon bonds and derivatives. The probablities that an analyst associates with going up and down are 60%

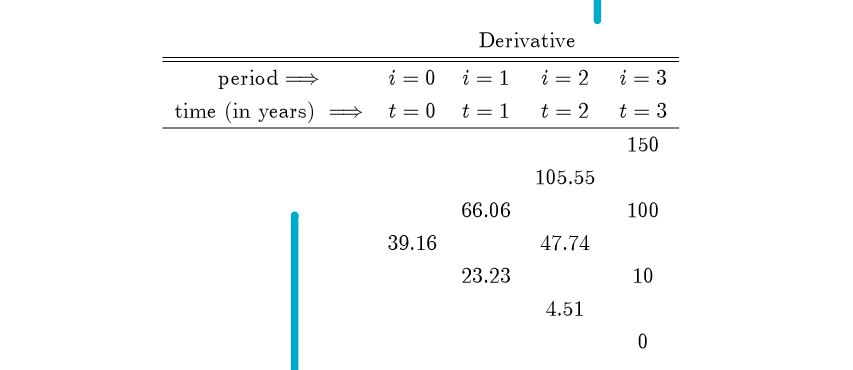

Given numbers are the prices of 5-years zero coupon bonds and derivatives. The probablities that an analyst associates with going up and down are 60% and 40% at each node of the tree, respectively. (NOTE: These are NOT the risk neutral probabilities.)

Q. What is the implied interest-rate tree up to t = 2?

Q. What is the price of a zero-coupon bond that matures at time t = 2?

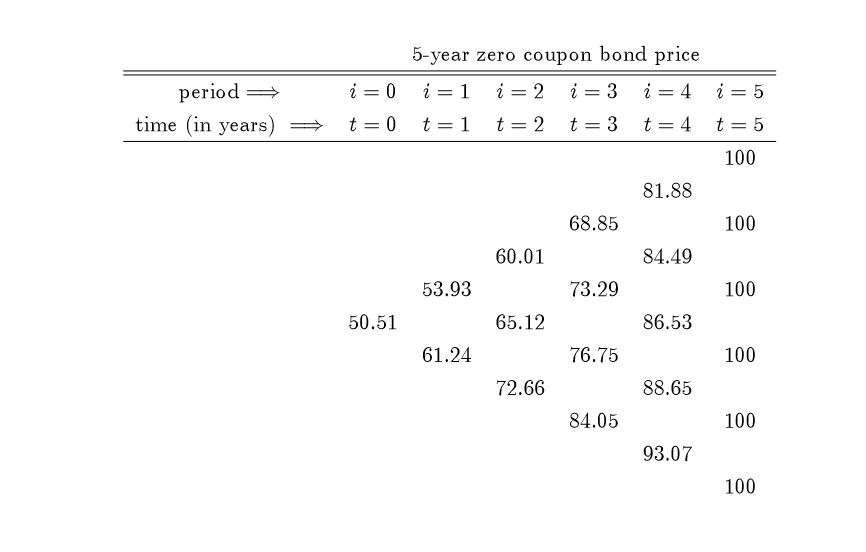

5-year zero coupon bond price period time (in years)t 0t-t 2 t 3 t 4 t 5 100 81.88 68.85 100 60.01 84.49 53.93 73.29 100 50.51 65.12 86.53 61.24 76.75 100 72.66 88.65 84.05 100 93.07 100

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

College Mathematics For Business Economics, Life Sciences, And Social Sciences

Authors: Raymond Barnett, Michael Ziegler, Karl Byleen, Christopher Stocker

14th Edition

0134674146, 978-0134674148