Question

Given the bond yields below, calculate the bond yields, spot rates and 1-year forward rates 1 year and 2 year from now (1f1 and 2f1).

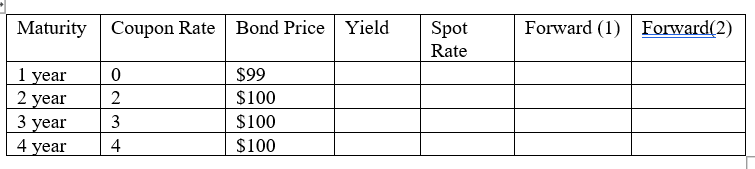

Given the bond yields below, calculate the bond yields, spot rates and 1-year forward rates 1 year and 2 year from now (1f1 and 2f1). All bonds have a face value of $100. Assume that coupon payments are made annually. Round to 1/1000.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Bitcoin Clarity The Complete Beginners Guide To Understanding

Authors: Kiara Bickers

1st Edition

1733871209, 978-1733871204