Question

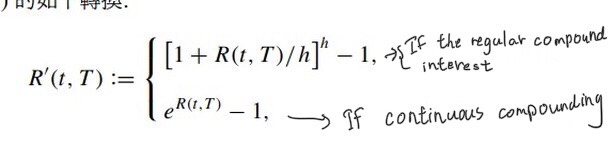

Given the following conversion of the spot interest rate R(t, T): Please prove that whether you use periodic compounding or continuous compounding, the relationship between

Given the following conversion of the spot interest rate R(t, T):

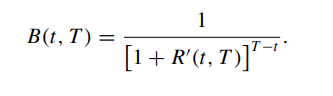

Please prove that whether you use periodic compounding or continuous compounding, the relationship between the discount factor B(t, T) and the spot interest rate  can be simplified as:

can be simplified as:

Please derive another conversion of the spot interest rate R(t, T), so that whether it is using periodic compounding or continuous compounding, the discount factor B(t, T) and the spot interest rate

of the spot interest rate R(t, T), so that whether it is using periodic compounding or continuous compounding, the discount factor B(t, T) and the spot interest rate are:

are:

Please derive another conversion  of the spot interest rate R(t, T ), so that whether it is using periodic compounding or continuous compounding, the discount factor B(t, T) and the spot interest rate

of the spot interest rate R(t, T ), so that whether it is using periodic compounding or continuous compounding, the discount factor B(t, T) and the spot interest rate  are:

are:

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Elements Of Chemical Reaction Engineering

Authors: H. Fogler

6th Edition

013548622X, 978-0135486221