Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Given the following SOFR forward risk-free rates with annual compounding: Time (Yr) 0 1 2 3 Spot 1Y Fwd Rate 6.00% 5.00% 4.00% DF

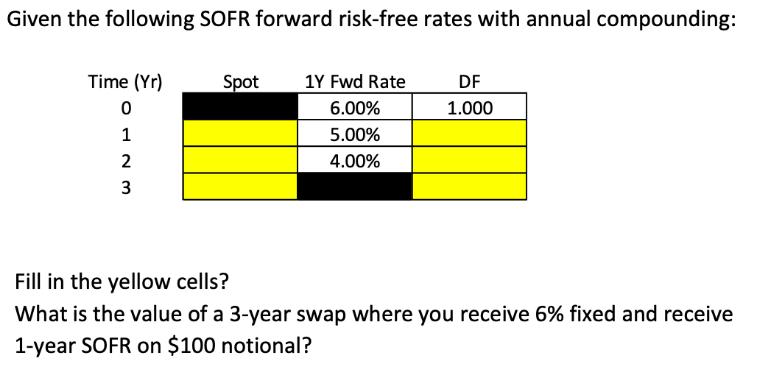

Given the following SOFR forward risk-free rates with annual compounding: Time (Yr) 0 1 2 3 Spot 1Y Fwd Rate 6.00% 5.00% 4.00% DF 1.000 Fill in the yellow cells? What is the value of a 3-year swap where you receive 6% fixed and receive 1-year SOFR on $100 notional?

Step by Step Solution

★★★★★

3.43 Rating (150 Votes )

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fixed Income Securities Valuation Risk and Risk Management

Authors: Pietro Veronesi

1st edition

0470109106, 978-0470109106