Answered step by step

Verified Expert Solution

Question

1 Approved Answer

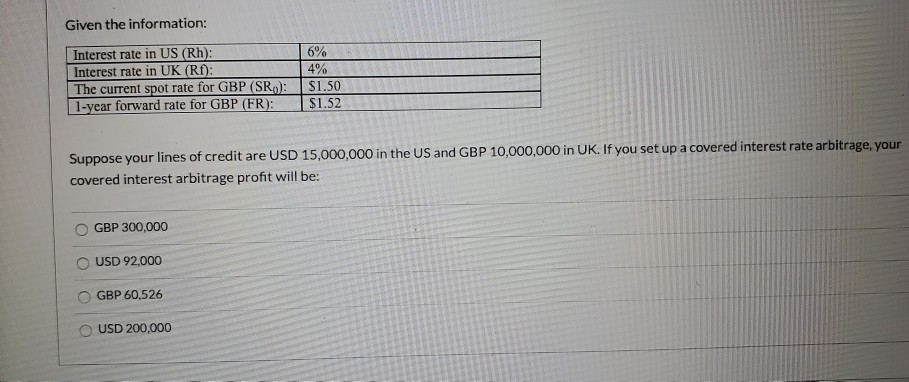

Given the information: Interest rate in US (Rh): Interest rate in UK (RI): The current spot rate for GBP (SR): 1-year forward rate for GBP

Given the information: Interest rate in US (Rh): Interest rate in UK (RI): The current spot rate for GBP (SR): 1-year forward rate for GBP (FR): 6% 4% $1.50 $1.52 Suppose your lines of credit are USD 15,000,000 in the US and GBP 10,000,000 in UK. If you set up a covered interest rate arbitrage, your covered interest arbitrage profit will be: GBP 300,000 USD 92.000 GBP 60,526 USD 200,000

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Institutional Asset Management

Authors: Frank J Fabozzi, Francesco A Fabozzi

1st Edition

9811220034, 9789811220036