Given the value line:

a.) what is the top line growth for 2015?

b.)Bottom-Line?

c.) Annual dividen per share?

d.) Current ratio in 2014?

e.) % bonds of Captial structure

f.) p/e ratio

g.) beta

h.) EBITDA %

I.) Long-Debt % change 2015

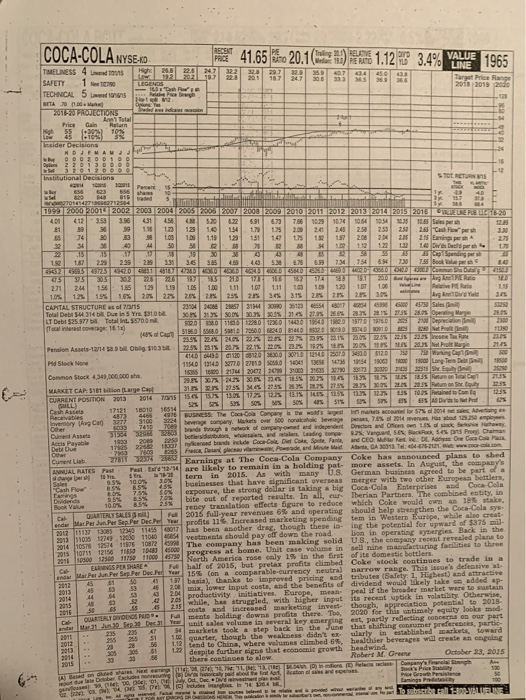

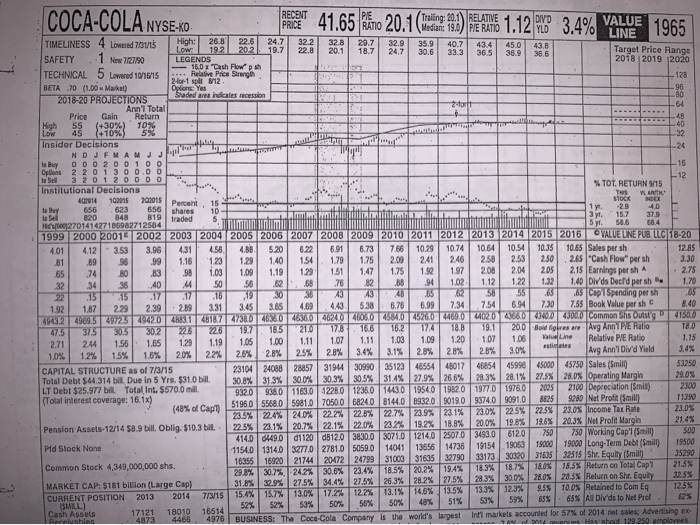

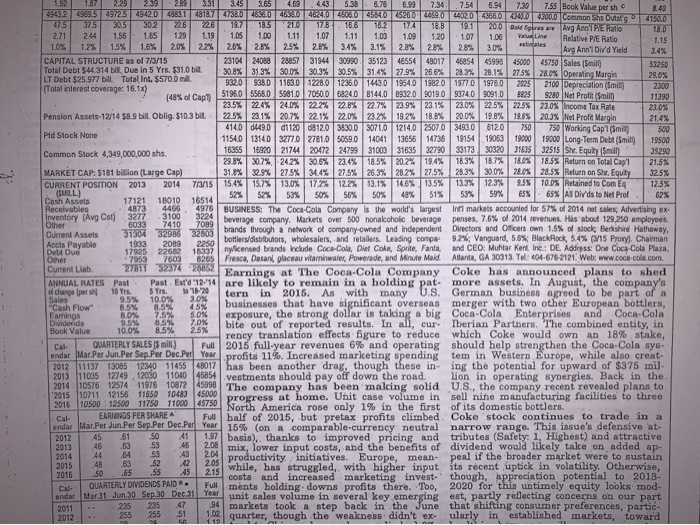

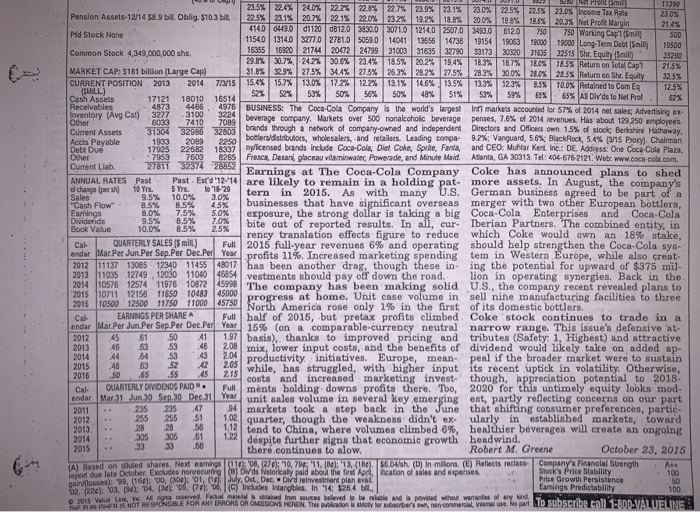

41.65 TO 20.1 (Media 92) ATM 1.12 ** 3.4% YAKE 1965 07 2:22. 87 3. 35.8 COCA-COLA NYSE:KO TIMELINESS 4 Lowered 70115 h: 289 29 SAFETY . 1 New 727190 LEGENDS TECHNICAL 5 Lowered 10/10 . Relative Pics Strengen BETA 70 (1.00 - Market) 2018-20 PROJECTIONS 36.9 Target Price Range 2018 2019 2020 16.0 x "Cash Flow psh 12 Oplont: Yes Sladed area indicales recession Price Ann' Tota Gain Return (-30%) 10$ High 55 XG Percent 15 3.53 156 123 673 12.85 2.53 76 Insider Decisions NDJEMAM le Buy OOO 200100 Opons 2 2 0 1 3 0 0 .0 0 lo Sell 3 20 1 20 000 Institutional Decisions % TOT. RETURN 9/15 400014 100015202015 LAH to Buy 656 623 656 819 3 y. 15. 7 37.9 H / 270141427186962712504| minim 5 y 58.6 8.4 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 VALUE LINE PUB, LLC 18-20 3.96 4.31 1029 1074 10 64 10.54 10.35 10.65 Sales per sh 1.16 1.79 125 2.09 241 246 258 2.50 2.65 "Cash Flow" per sh 3.30 1.00 151 1.47 1.75 1.921 97 208 204 205 215 larines per a - 2.75 50 56 62 941 102 1.12 1.22 1921 1.40 Dids Decl per sh . 1.70 416516258 35 Cap Spending persh85 1.92 2.39 289 3.31 3.45 365 443 5.38 6.76 6.997.34 7.54 6.94 7.30 7.55 Book Value per sh 8 .40 494322290915 29723549420421461871273807636046360462404606.045840145200 4600 402036604043000 Common Shs 1500 30221512819.7115 16.2 177 188 19.1 200 Bow Tires are Avg Ann TPE Ratio T 16.0 2.71 244 1.56 1.65 129 1.19 1.05 1.00 1.11 1.07 111 103 109 120 107 106 Value Line Relative PVE Ratio 1.15 1.0% 1.2% 15% 16% 20% 22% 2.8% 28% 2.5% 28% 3.4% 3.1% 28% 2.8% 28% 30% estimates Avg Ann'l Divd Yield 3.4% CAPITAL STRUCTURE as of 7/3/15 23104 2408828857 3194430990 3512346554 480174685445990 45000 45750 Sales (Smill 53250 Total Debt $44.314 bil. Due in 5 Yrs. $31.0 bill 30.8% 31,3% 30% 30.3% 30.5% 31.4% 27.9% 26.6% 28.3% 28.1% 27.5% 28.0% Operating Margin 29.0% LT Debt $25.977 bill Total Int. $570.0 mill. 932093801163.0 228.0 1236.0 1430 19540 1920 1977 1976.0 2005 2100 Depreciation (Smil) 2300 (Total interest coverage: 16.1%) 14 Car 51960 5568.0 5981.0 7050.0 6824. 0 8144.0 1932.09019. 0 9374. 0 90910 6825 9280 Net Proft Smill) 11390 224% 240% 222% 22,6 22.7% 29% 23.1% 73.0% 22.5% 22.5% 23.09 Income Tax Rate 23.0% 22.5% Pension Assets-12/14 $8.9 bill. Oblig. $10.3 bil. 23.1% 20.7% 22.1% 22.0% 23.2% 19.2% 18.8% 20.0% 19.8% 19.6% 21.4% 20.3% Net Prolit Margin 41406149001120 08120 38300 3071.0 12140 2507.0 3493.0 6120 750 750 Working Cap' (Small) 500 Pld Stock None 1154013140 32770 27810 5059.0 14041 1365614736 191541906319000 19000 Long-Term Debt (Small) 19500 163551692021744 20472 2479931003 31635 3279033173 3032031535 32515 Shr. Equity ($mill 35290 Common Stock 4,349,000,000 shs. 29.8% 30.7% 24.2% 30.6% 23.4% 18.5% 20.2% 19.4% 18.3% 18.7% 80% 18.5% Return on Total Cap1 21.5% MARKET CAP: $181 billion (Large Cap) 32,9% 31.6% 27.5% 34.4% 27.5% 26.3% 28.2% 27.5% 28,3% 325 30.0% 28.0% 28.5% Return on Shr. Equity CURRENT POSITION 2013 2014 7/3/15154% 15.7% 13.0% 17.2% 12% 12.5% 13.1% 14.6% 13.5% 13,3% 12,3% 9.5 10.0% Retained to Com E (SLL) 52% 52% 50% 50% 50% 50% 48% 51% 53% 59% 6 65% All Div'ds to Net Prol 4873 4466 4976 BUSINESS: The Coca-Cola Company is the world's largest int markets accounted for 57% of 2014 nel sales: Advertising ex LS Cashles 121 1801 16514 P art 129 259 Obes 1.15 11390 500 1.921.87 29 29.2 331 3.45 3.65 4.60 4.43 5.386.76 6.9 7.34 .7.54 6.94 7.30 7.55 Book Value per sh 49432 4968.5 4972549420 483.1 4818.7 47330 465.0 46.0 4624.0 45000 4584045260 440 44620 4566.0 43000 4300.0 Common Shs Outsi 475 37513113021251261171105 4150.0 21017.8. 166 16217418.8 19.1 2010 Bold Golres TAVO ARIPLE Halla TBD 2.71 2.44 156 1.65 129 1.19 1.05 1.00 1.11 1.07 1.11 1.03 1.09 120 107 108 Line Relative PF Reto 1.0% 1.2% 15% 16% 20% 22% 2.5% 2.5% 2.5% 2.8% 3.4% 3.1% 2.8% 28% 28% 30% stimates Avg Ann'l Divd Yield CAPITAL STRUCTURE as of 7/3/15 | 23104 2408828857319443099035123 | 465544801746854 45990 45000 45750 Sales (Smil Total Debt $44 314 . Due in 5 Yrs. 531,0 bil 30.8% 31.3% 30.0% 30.3% 30.5% 31.4% 27.9% 266% 23% Total Int. $5700 mil 28,1% 27.5% LT Debt $25.977 BIL 29.0% 28.0% Operating Margin 9320 930116301228012360 143.0 1954.0 1982.0 1977 1976.0 (Total interest coverage: 16.1x) 2025 2100 Depreciation (Smith [48% af Capt 5196.0 556.0 58810 7050.0 68240 8144.0 1932.0.9019.0 3374090910 6825 9280 Net Profit (Smil 23.5% 22.4% 24.0% 22.2% 22.8% 22.7% 23.9% 23.1% 23.0% 22.5% 22.5% 23.0% Income Tax Rate 23.0% Pension Assets-12/14 $9.9 bill. Oblig: $10.3 bil. 22.5% 28.1% 20.7% 221% 220% 2 23% 19.2% 18.8% 200% 19.8% 19.6% 20.3% Net Prola Marin 21.4% 4140 64490 0112068120 38300 3071.0 1214,0 2507.0 3493 6120 750 750 Working Cap' (Smil) Pld Stock None 1154013140 3277 2781.0 50590140411365614736 191541906319000 19000 Long-Term Debt (Smith) 19500 16355 1692021744 20472 24799 31003 Common Stock 4,349,000,000 shs. 3163532790 33173 3032031035 32515 Shr. Equity (Smil 35290 29.8% 30.7% 242% 30.6% 23.4% 18.5% 20.2% 19.4% 18.3% 18.7% 18.0% 18.5% Return on Total Cap' 21.5% MARKET CAP: 5181 billion (Large Cap) 31.8% 2,9% 27.5% 34.4% 21.5% 26.3% 28.2% 27.5% 28.3% 30.0% 28.0% 28.5Return on Sht. Equity 32.5% CURRENT POSITION 2013 2014 7/8/15154% 15,7% 13.0% 17.2% 12% 13.15 14.6% 13.5% 13.3% 12,3% 9.55 10.0% Retained to Com E 1 25% SALI 52% 52% 53% 16514 50% 56% 50% 48% 51% 18010 53% 59% 65% 65% A1 Div ds to Net Prof. Cash Assets 62% 17121 Receivables 4873 4466 4976 BUSINESS: The Coca-Cola Company is the world's largest in markets accounted for 57% of 2014 net sales Advertising ex. Inventory (Avg Csl) 3277 3100 3224 beverage company. Markets over 500 nonalcoholic beverage penses, 7.6% of 2014 revenues. His about 129 250 employees Other 6033 7089 7410 brands through a network of company-owned and independent Directors and Oicers own 1.5% of stock Berkshire Hathaway Current Assets 37304 32986 32803 bottlers/distributors, wholesalers, and retailers. Leading compa 9.2% Vanguard, 5.6% Black Rock, 5.4% (3/15 Proxyl Chairman Accts Payable 1933 2089 2250 De Due 17925 92612 10337 nwicensed bands include Coca-Cola, Diet Coke, Sante Fanta and CEO: Muhtar Kent Inc: DE, Address: One Coca Cola Plaza Other 7953 76038265 Fresca, Dasanl placeau wamin waterPowevade, and Minute Mald Atlanta, GA 30313. Tel: 404-676 2121 Web: www.coca cola com Current Lab 27877 3237 28 Earnings at The Coca-Cola Company Coke has announced plans to shed ANNUAL RATES Past Past. Ed 12-14 are likely to remain in a holding pat. more assets. In August, the coinpany's dl change per 10 Yrs. Yes, 120 tern in 2015. As with many Sales 9.5 10.0% U.S. German business agreed to be part of a 30% -Cash Flow ,5% 8.5% 2.5% businesses that have significant overseas merger with two other European bottlers, Earnings 3.0% 7.5% 50% exposure, the strong dollar is taking a big Coca-Cola Enterprises and Coca-Cola DiNidends 9.5% 8.5% 20% Book Value bite out of reported results. In all, cur 2.5% 100% 2.5% Iberian Partners. The combined entity, in rency translation effects figure to reduce which Coke would own an 18% stake, Cal. QUARTERLY SALESIS mill) Full 2015 full-year revenues 6% and operating should help strengthen the Coca-Cola sys- endar Mar Per Jun.Per Sep.Per Dec.Perl Year profits 11%. Increased marketing spending tem in Western Europe, while also creat 2012 11137 13085 12340 11455 48017 has been another drag, though these in ing the potential for upward of $375 mil- 2013 (11035 12749., 12050 1104045854vestments should pay off down the road. lion in operating synergies. Back in the 2014 (10576 12574 11976 10872 45098 The company has been malcing solid 45998 U.S., the company recent revealed plans to 2015 (1071112156 11650 10483 45000 progress at home, Unit case volume in 2016 10500 12500 11750 sell nine manufacturing facilities to three 11000 45750 North America rose only 1% in the first of its domestic bottlers. EARNINGS PER SHARE A Full half of 2015, but pretex profits climbed Coke 'stock continues to trade in a endar Mar.Per Jun.Per Sep.Per Dec.Per Year 15% (on comparable-currency neutral narrow range. This issue's defensive at 2012 45 61 50 411.97 basis), thanks to improved pricing and tributes (Safety: 1, Highest) and attractive 2013 46 53 2.08 mix, lower input costs, and the benefits of dividend would likely take on added ap. 2014 44 64 2.04 productivity initiatives. Europe, mean- peal if the broader market were to sustain 2015 4B 63 50 while, has struggled, with higher input its rcent uptick in volatility. Otherwise, ,65 .45 55 215 costs and increased marketing invest-' though, appreciation potential to 2018- C Q UARTERLY DIVIDENDS PAID . Full ments holding downs profits there. Too, 2020 for this untimely equity looks mod- endar Mar 31 Jun 30 Sep.30 Dec 31 Year unit sales volume in several key emerging est, partly reflecting concerns on our part 285 285 47 1 94 markets took a step back in the June that shifting consumer preferences, partic 2012 255 256 51 1.02 quarter, though the weakness didn't ex- ularly in established markets, toward 205 2016 50% WIDU LULU JIU 200 23.5% Promil 11390 224% 24.0% 22.7% 22.8% 22.7% 23.9% 23.1% 20% 22.5% 22.5 Pension Assets-12/14 58.9 bil. Oblig. $10.3 bil. 22.5% 23,1% 23.0% Income Tax Rate 23.0% 20.7% 22.1% 20% 23.2% 19.2% 18.8% 20.0% 19.8% 19.5% 20.3% Net Proft Margin 414 21.4% 490 01120 8120 3830.0 3071,0 1214.0 2507.0 3493.0 6120 Pld Stock None 11540 13140 samo 27810 50590140411355614736191541906319000 19000 Long Term Debt Smith 750 750 Working Cap'l (Smil 500 19500 Common Stock 4,349,000,000 sh. 163551892021744 20472 24799 31003 31635 32790 33173 30020 31635 32515 Shr. Equity (Smil 29, 35290 30,78242 3 01 23.4% 85% 20.2% 19.4% 18.3% 18.7% 100% 1858 Return on Total Cap 2155 MARKET CAP: 5181 billion (Large Cap) 31.8% 32,9% 27.5% 34.4% 27.5% 26.3% 282% 27.5% 28.3% 30.0% 28.0% 28.5 Return on Shr, Equity 32.5% CURRENT POSITION 2013 2014 7/115 15.4% 15.7% 13.0% 17.2% 12.2% 13.1% 146% 135% 133% 123% 123% 9.5% 95% 100% Retained in Como 10.0% Retained to Com Eg 125% SHILL) 52% 52% Cash Assets 16514 53% 18010 50% 56% 50% 17121 48% 51% 53% 59% 65% 65% A DIVds to Net Prot 62% Receivables 4873 4466 4976 BUSINESS: The Coca-Cola Company is the world's largest int markets accounted for 57% of 2014 net sales Advertising er Inventory (Avg Csl) 32773100 Other 9 3 beverage company, Markets over 500 nonalcoholic beverage 7410 7089 penses, 7.6% of 2014 revenues. Has about 129 250 erclovees. Current Assets 31304 3298632803 brands through a network of company-owned and independent Directors and Officers own 1.5% of stock, Berkshire Hathaway Accts Payable 1933 2089 2250 bottlers/distributors, wholesalers, and retailers. Leading compa: 9.2% Vanguard, 5.6% Black Rock, 5.4% 9/15 Poryl, Chairman Debt Due 17025 222 1837 licensed brands include Coca-Cola, Diet Coke, Sprite, Fanta, and CEO: Muhtar Kent Inc.: DE, Address One Coca Cola Plaza Other -7953 7603 8 265 Fresca, Dasanl glace vitaminwater Powerade and Minute Maid Atlanta, GA 30313. Tel: 404-676-2121. Web www.coca-cola.com Current Lab. 271 37274209 Earnings at The Coca-Cola Company Coke has announced plans to shed ANNUAL RATES Past. Past Esrd 12-14 are likely to remain in a holding pat more assets. In August, the company's al change per sh 10 Yrs. Yes, 18-20 tern 3.0% in 2015. As with many 9.5% U.S. German business agreed to be part of a 10.0% "Cash Flow - 8.5% 0.5% 4.5% businesses that have significant overseas merger with two other European bottlers, 8.0% exposure, the strong dollar is taking a big Coca-Cola Enterprises and Coca-Cola Dividends 9.5% 8.5% 70% Book Value 10.0% 0.5% 2.5% bite out of reported results. In all, cur- Iberian Partners. The combined entity, in rency translation effects figure to reduce which Coke would own an 18% stale. Cal QUARTERLY SALES IS mill) Full 2015 full-year revenues 6% and operating should help strengthen the Coca-Cola sys- endar Mar Per Jun.Per Sep.Per Dec.Perl Year profits 11%. Increased marketing spending tem in Western Europe, while also creat- 2012 (11137 13085 12340 11455 48017 has been another drag, though these in ing the potential for upward of $375 mil- 2013 (11035 12749 12030 11040 46854 vestments should pay off down the road lion in operating synergies. Back in the 2014 (10576 12574 11976 10872 145998 The company has been malcing solid U.S., the company recent revealed plans to 201511071112156 11650 10483 45000 progress at home. Unit case volume in sell nine manufacturing facilities to three 2016 (10500 12500 11750 11000 45750 North America rose only 1% in the first of its domestic bottlers. Cat EARNINGS PER SHARE A Full ball of 2016, but pretax profits climbed Coke stock continues to trade in a endar Mar.Per Jun Per Sep Per Dec.Per Year 15% (on a comparable-currency neutral narrow range. This issue's defensive at 2012 45 61 50 411.97 basis), thanks to improved pricing and tributes (Safety: 1, Highest) and attractive 2013 45 2 3 46 208 mix, lower input costs, and the benefits of dividend would likely take on added ap- 2014 44 64 53 productivity initiatives. Europe, mean- peal if the broader market were to sustain 2.05 while, has struggled, with higher input its rcent uptick in volatility. Otherwise, 2016 50 .65 .55 costs and increased marketing invest- though, appreciation potential to 2018- Cal- QUARTERLY DIVIDENDS PAID. ments holding downs profits there. Too, 2020 for this untimely equity looks mod- ondar Mar 31 Jun 30 Sep 30 Dec 31 Year unit sales volume in several key emerging est, partly reflecting concerns on our part 2011 markets took a step back in the June that shifting consumer preferences, partic- 2012 1.02 quarter, though the weakness didn't ex- ularly in established markets, toward 2013 tend to China, where volumes climbed 6%, healthier beverages will create an ongoing 305 305 51 despite further signs that economic growth headwind. 33 33 2015 66 there.continues to slow. Robert M. Greene October 23, 2015 (A) Based on diluted shares Next earnings 1100 270; 10,704 11. (Be): "13,4186). $0.04sh (D) in mlions (1) Relicis reclass Company's Financial Strength Att od due late October. Excludes normecurring ) Dids storically paid about the former llication of sales and expenses. Stock's Price Stability 100 mainlassesh: 99, (160); 00, 300): 01. (16: July, Oct, Dec, Dvd relwestment planaval 2 1220309:04. (3005, (7): 06, (C) Includes bangles. In '14 $25.4 HII Earnings Predictability 100 W ineh Ali Nerved Face d from suces belevede late and provided without warranties of any kind TOUR IS NOT RESPONSABLE FOR ANY ERRORS OR OMISSONS HOREN. TNS publication is no lor subscrber's ows, noncora wens ho part To Subscribe call CBDD VALUELINE 204 2015 48 2.15 Full 51 28 1.12 1.22 2014 pe Growth Persistence $0