Answered step by step

Verified Expert Solution

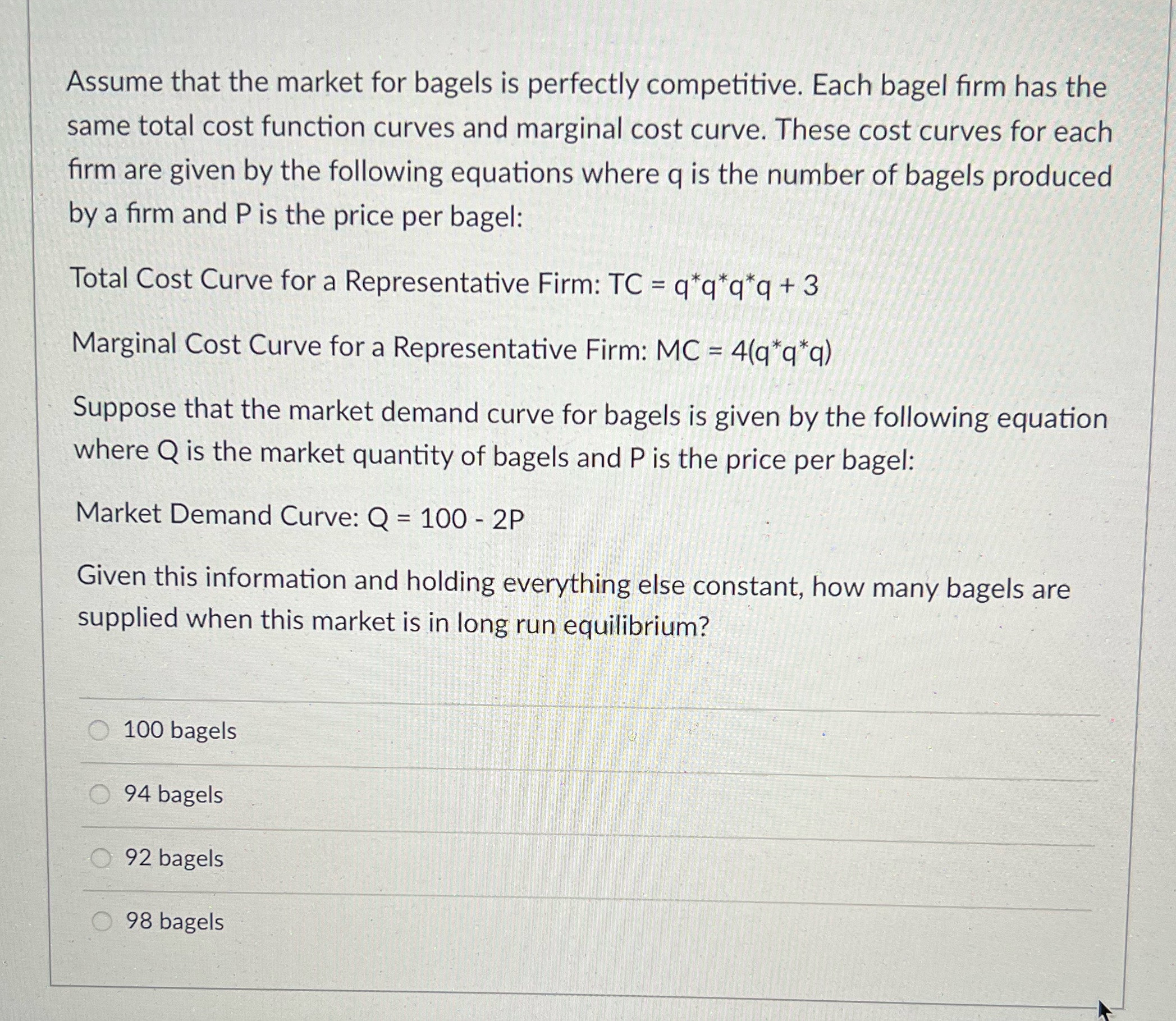

Question

1 Approved Answer

Given this information and holding everything else constant, how many bagels are supplied when this market is in long run equilibrium? Assume that the market

Given this information and holding everything else constant, how many bagels are supplied when this market is in long run equilibrium?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Econometrics By Example

Authors: Damodar Gujarati

2nd Edition

1137375019, 9781137375018