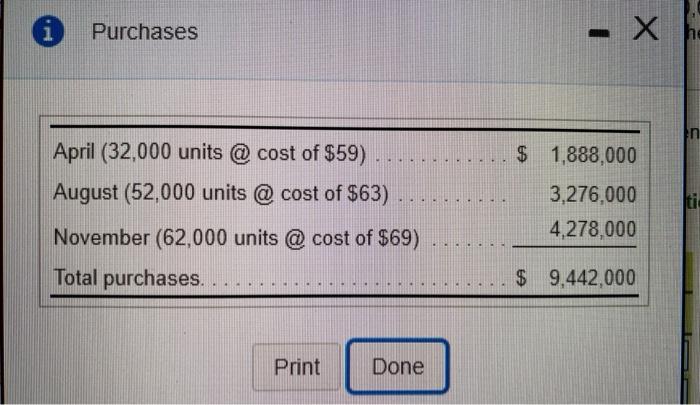

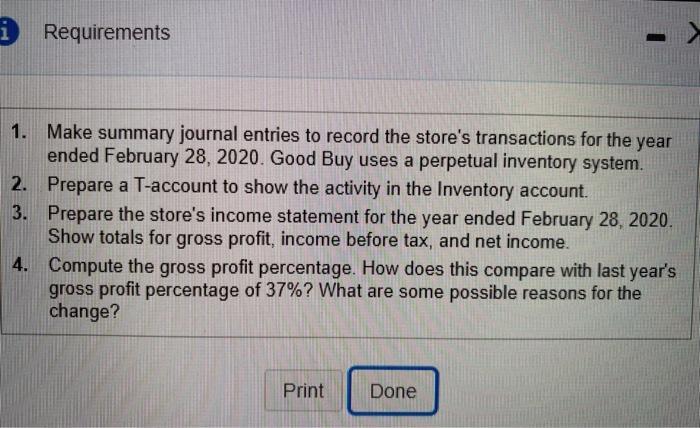

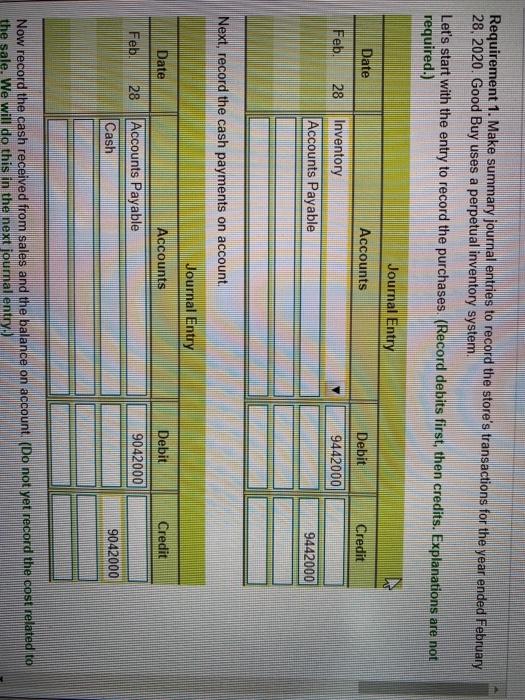

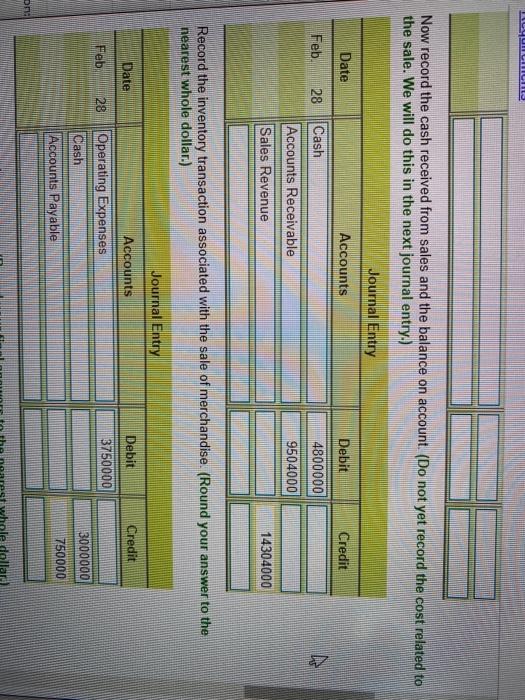

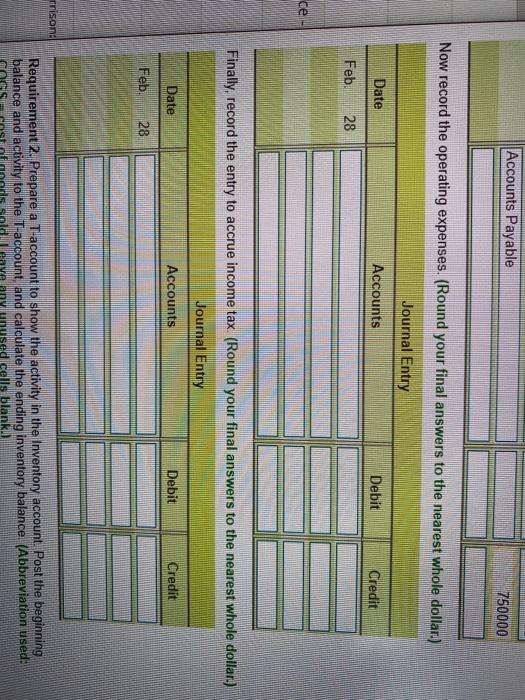

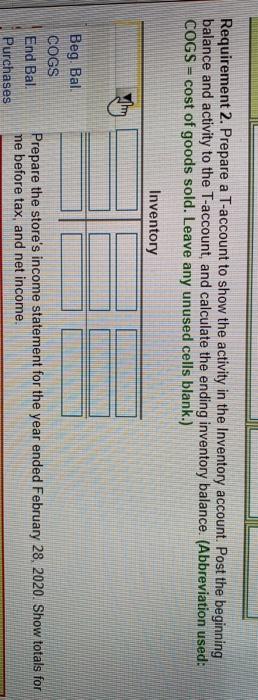

Good Buy purchases merchandise inventory by the crate each crate of inventory is a unit. The fiscal year of Good Buy ends each February 28. Assume you are dealing with a single Good Buy store in Whitehorse, Yukon, and that the store experienced the following: The store began fiscal year 2020 with an inventory of 21.000 units that cost a total of $1,050,000. During the year, the store purchased merchandise on account as follows: BE! (Click the icon to view the purchases.) Cash payments on account totalled $9,042,000. During fiscal year 2020, the store sold 149.000 units of merchandise for $14. 304,000. Cash accounted for $4,800.000 of this, and the balance was on account. Good Buy uses the FIFO method for inventories. Operating expenses for the year were $3,750,000. The store paid 80% in cash and accrued the rest as accrued liabilities. The store accrued income tax at the rate of 35%. Requirements Purchases - X $ 1,888,000 April (32,000 units @ cost of $59) ... August (52,000 units @ cost of $63) . . 3,276,000 4,278,000 November (62,000 units @ cost of $69) Total purchases. $ 9,442,000 - Print Done i Requirements 1. Make summary journal entries to record the store's transactions for the year ended February 28, 2020. Good Buy uses a perpetual inventory system. 2. Prepare a T-account to show the activity in the Inventory account. 3. Prepare the store's income statement for the year ended February 28, 2020. Show totals for gross profit, income before tax, and net income. 4. Compute the gross profit percentage. How does this compare with last year's gross profit percentage of 37%? What are some possible reasons for the change? Print Done Requirement 1. Make summary journal entries to record the store's transactions for the year ended February 28, 2020. Good Buy uses a perpetual inventory system. Let's start with the entry to record the purchases. (Record debits first, then credits. Explanations are not required.) Journal Entry Date Accounts Debit Credit Feb. 28 9442000 Inventory Accounts Payable 9442000 Next, record the cash payments on account Journal Entry Date Accounts Debit Credit Feb 28 9042000 Accounts Payable Cash 9042000 Now record the cash received from sales and the balance on account (Do not yet record the cost related to the sale. We will do this in the next journal entry.) CYCLO Now record the cash received from sales and the balance on account. (Do not yet record the cost related to the sale. We will do this in the next journal entry.) Joumal Entry Date Accounts Debit Credit Feb 28 Cash 4800000 Accounts Receivable 9504000 Sales Revenue 14304000 Record the inventory transaction associated with the sale of merchandise. (Round your answer to the nearest whole dollar.) Journal Entry Date Debit Credit Feb 29 3750000 Accounts Operating Expenses Cash Accounts Payable 13000000 750000 Accounts Payable 750000 Now record the operating expenses. (Round your final answers to the nearest whole dollar.) Journal Entry Date Accounts Debit Credit Feb. 28 ce Finally, record the entry to accrue income tax (Round your final answers to the nearest whole dollar) Journal Entry Date Accounts Debit Credit Feb 28 rrison Requirement 2. Prepare a T-account to show the activity in the Inventory account. Post the beginning balance and activity to the T-account and calculate the ending inventory balance (Abbreviation used: unused cells blank Requirement 2. Prepare a T-account to show the activity in the Inventory account. Post the beginning balance and activity to the T-account, and calculate the ending inventory balance. (Abbreviation used: COGS = cost of goods sold. Leave any unused cells blank.) Inventory Beg. Bal COGS End Bal. Purchases Prepare the store's income statement for the year ended February 28, 2020. Show totals for ne before tax, and net income. Good Buy purchases merchandise inventory by the crate each crate of inventory is a unit. The fiscal year of Good Buy ends each February 28. Assume you are dealing with a single Good Buy store in Whitehorse, Yukon, and that the store experienced the following: The store began fiscal year 2020 with an inventory of 21.000 units that cost a total of $1,050,000. During the year, the store purchased merchandise on account as follows: BE! (Click the icon to view the purchases.) Cash payments on account totalled $9,042,000. During fiscal year 2020, the store sold 149.000 units of merchandise for $14. 304,000. Cash accounted for $4,800.000 of this, and the balance was on account. Good Buy uses the FIFO method for inventories. Operating expenses for the year were $3,750,000. The store paid 80% in cash and accrued the rest as accrued liabilities. The store accrued income tax at the rate of 35%. Requirements Purchases - X $ 1,888,000 April (32,000 units @ cost of $59) ... August (52,000 units @ cost of $63) . . 3,276,000 4,278,000 November (62,000 units @ cost of $69) Total purchases. $ 9,442,000 - Print Done i Requirements 1. Make summary journal entries to record the store's transactions for the year ended February 28, 2020. Good Buy uses a perpetual inventory system. 2. Prepare a T-account to show the activity in the Inventory account. 3. Prepare the store's income statement for the year ended February 28, 2020. Show totals for gross profit, income before tax, and net income. 4. Compute the gross profit percentage. How does this compare with last year's gross profit percentage of 37%? What are some possible reasons for the change? Print Done Requirement 1. Make summary journal entries to record the store's transactions for the year ended February 28, 2020. Good Buy uses a perpetual inventory system. Let's start with the entry to record the purchases. (Record debits first, then credits. Explanations are not required.) Journal Entry Date Accounts Debit Credit Feb. 28 9442000 Inventory Accounts Payable 9442000 Next, record the cash payments on account Journal Entry Date Accounts Debit Credit Feb 28 9042000 Accounts Payable Cash 9042000 Now record the cash received from sales and the balance on account (Do not yet record the cost related to the sale. We will do this in the next journal entry.) CYCLO Now record the cash received from sales and the balance on account. (Do not yet record the cost related to the sale. We will do this in the next journal entry.) Joumal Entry Date Accounts Debit Credit Feb 28 Cash 4800000 Accounts Receivable 9504000 Sales Revenue 14304000 Record the inventory transaction associated with the sale of merchandise. (Round your answer to the nearest whole dollar.) Journal Entry Date Debit Credit Feb 29 3750000 Accounts Operating Expenses Cash Accounts Payable 13000000 750000 Accounts Payable 750000 Now record the operating expenses. (Round your final answers to the nearest whole dollar.) Journal Entry Date Accounts Debit Credit Feb. 28 ce Finally, record the entry to accrue income tax (Round your final answers to the nearest whole dollar) Journal Entry Date Accounts Debit Credit Feb 28 rrison Requirement 2. Prepare a T-account to show the activity in the Inventory account. Post the beginning balance and activity to the T-account and calculate the ending inventory balance (Abbreviation used: unused cells blank Requirement 2. Prepare a T-account to show the activity in the Inventory account. Post the beginning balance and activity to the T-account, and calculate the ending inventory balance. (Abbreviation used: COGS = cost of goods sold. Leave any unused cells blank.) Inventory Beg. Bal COGS End Bal. Purchases Prepare the store's income statement for the year ended February 28, 2020. Show totals for ne before tax, and net income