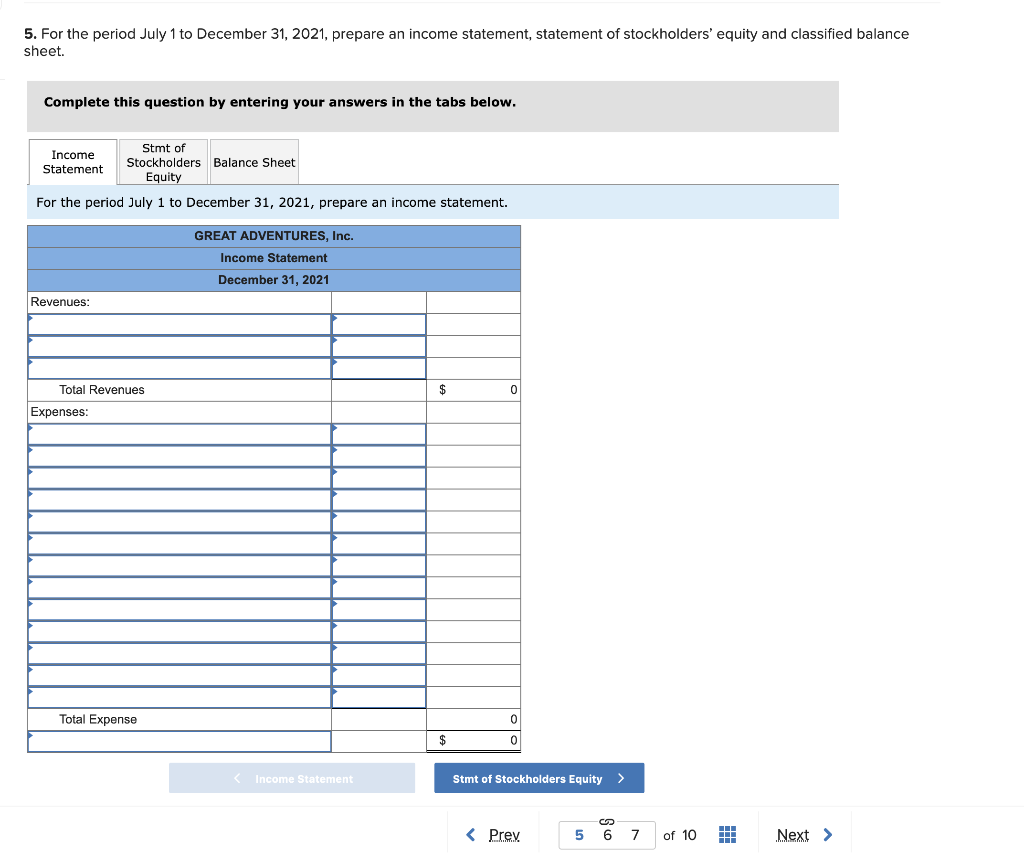

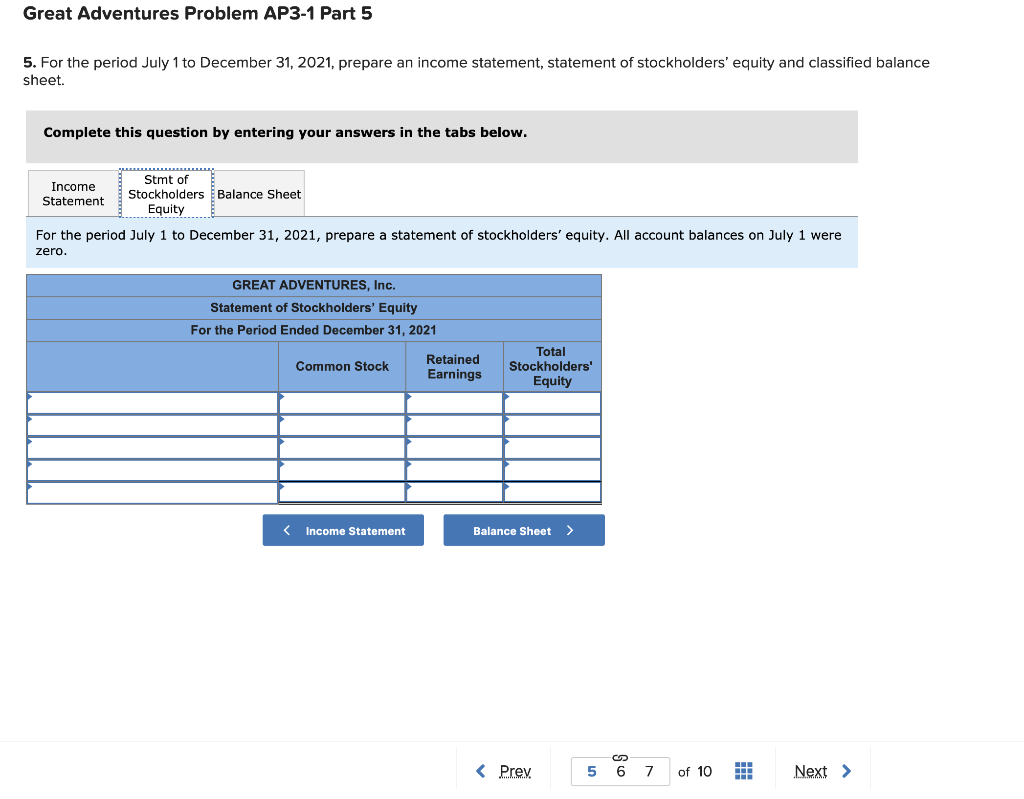

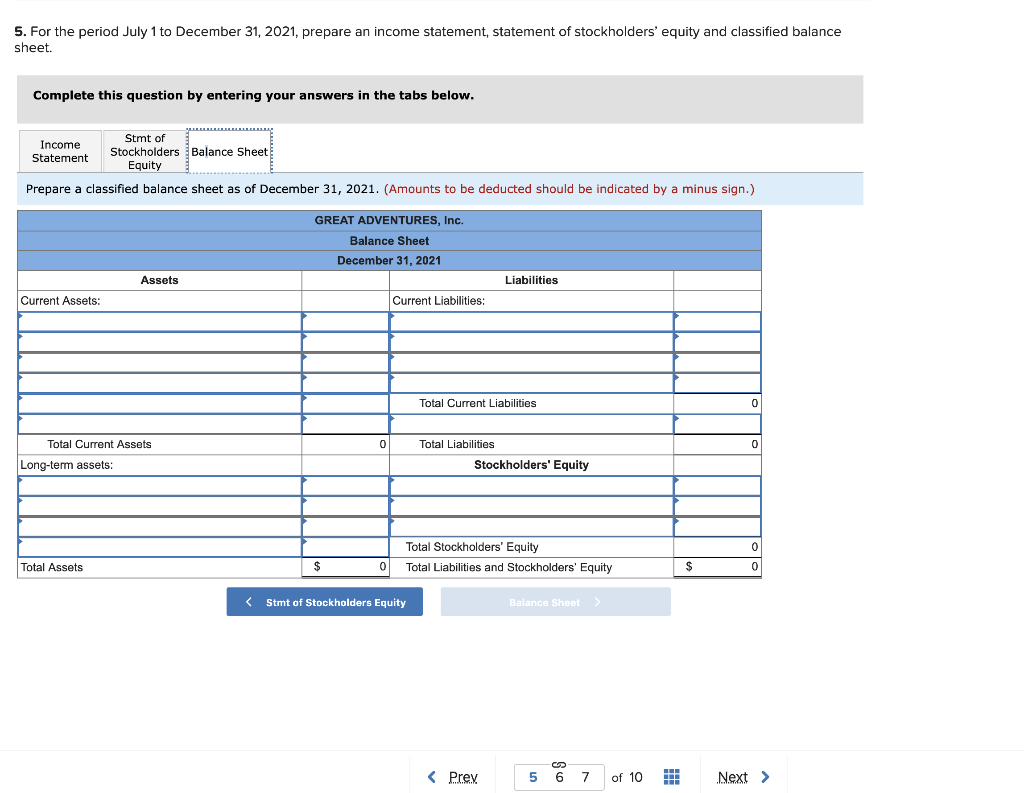

Question

Great Adventures Problem AP3-1 [The following information applies to the questions displayed below.] Tony and Suzie graduate from college in May 2021 and begin developing

Great Adventures Problem AP3-1

[The following information applies to the questions displayed below.]

Tony and Suzie graduate from college in May 2021 and begin developing their new business. They begin by offering clinics for basic outdoor activities such as mountain biking or kayaking. Upon developing a customer base, theyll hold their first adventure races. These races will involve four-person teams that race from one checkpoint to the next using a combination of kayaking, mountain biking, orienteering, and trail running. In the long run, they plan to sell outdoor gear and develop a ropes course for outdoor enthusiasts.

On July 1, 2021, Tony and Suzie organize their new company as a corporation, Great Adventures Inc. The articles of incorporation state that the corporation will sell 29,000 shares of common stock for $1 each. Each share of stock represents a unit of ownership. Tony and Suzie will act as co-presidents of the company. The following transactions occur from July 1 through December 31.

| Jul. | 1 | Sell $14,500 of common stock to Suzie. | ||

| Jul. | 1 | Sell $14,500 of common stock to Tony. | ||

| Jul. | 1 | Purchase a one-year insurance policy for $3,600 ($300 per month) to cover injuries to participants during outdoor clinics. | ||

| Jul. | 2 | Pay legal fees of $1,600 associated with incorporation. | ||

| Jul. | 4 | Purchase office supplies of $1,800 on account. | ||

| Jul. | 7 | Pay for advertising of $360 to a local newspaper for an upcoming mountain biking clinic to be held on July 15. Attendees will be charged $50 on the day of the clinic. | ||

| Jul. | 8 | Purchase 10 mountain bikes, paying $10,000 cash. | ||

| Jul. | 15 | On the day of the clinic, Great Adventures receives cash of $2,000 from 40 bikers. Tony conducts the mountain biking clinic. | ||

| Jul. | 22 | Because of the success of the first mountain biking clinic, Tony holds another mountain biking clinic and the company receives $2,400. | ||

| Jul. | 24 | Pay $850 to a local radio station for advertising to appear immediately. A kayaking clinic will be held on August 10, and attendees can pay $130 in advance or $180 on the day of the clinic. | ||

| Jul. | 30 | Great Adventures receives cash of $6,500 in advance from 50 kayakers for the upcoming kayak clinic. | ||

| Aug. | 1 | Great Adventures obtains a $44,000 low-interest loan for the company from the city council, which has recently passed an initiative encouraging business development related to outdoor activities. The loan is due in three years, and 6% annual interest is due each year on July 31. | ||

| Aug. | 4 | The company purchases 14 kayaks, paying $11,000 cash. | ||

| Aug. | 10 | Twenty additional kayakers pay $3,600 ($180 each), in addition to the $6,500 that was paid in advance on July 30, on the day of the clinic. Tony conducts the first kayak clinic. | ||

| Aug. | 17 | Tony conducts a second kayak clinic, and the company receives $11,100 cash. | ||

| Aug. | 24 | Office supplies of $1,800 purchased on July 4 are paid in full. | ||

| Sep. | 1 | To provide better storage of mountain bikes and kayaks when not in use, the company rents a storage shed for one year, paying $3,840 ($320 per month) in advance. | ||

| Sep. | 21 | Tony conducts a rock-climbing clinic. The company receives $15,100 cash. | ||

| Oct. | 17 | Tony conducts an orienteering clinic. Participants practice how to understand a topographical map, read an altimeter, use a compass, and orient through heavily wooded areas. The company receives $18,600 cash. | ||

| Dec. | 1 | Tony decides to hold the companys first adventure race on December 15. Four-person teams will race from checkpoint to checkpoint using a combination of mountain biking, kayaking, orienteering, trail running, and rock-climbing skills. The first team in each category to complete all checkpoints in order wins. The entry fee for each team is $560. | ||

| Dec. | 5 | To help organize and promote the race, Tony hires his college roommate, Victor. Victor will be paid $40 in salary for each team that competes in the race. His salary will be paid after the race. | ||

| Dec. | 8 | The company pays $1,600 to purchase a permit from a state park where the race will be held. The amount is recorded as a miscellaneous expense. | ||

| Dec. | 12 | The company purchases racing supplies for $2,900 on account due in 30 days. Supplies include trophies for the top-finishing teams in each category, promotional shirts, snack foods and drinks for participants, and field markers to prepare the racecourse. | ||

| Dec. | 15 | The company receives $22,400 cash from a total of forty teams, and the race is held. | ||

| Dec. | 16 | The company pays Victors salary of $1,600. | ||

| Dec. | 31 | The company pays a dividend of $4,200 ($2,100 to Tony and $2,100 to Suzie). | ||

| Dec. | 31 | Using his personal money, Tony purchases a diamond ring for $3,900. Tony surprises Suzie by proposing that they get married. Suzie accepts and they get married! |

The following information relates to year-end adjusting entries as of December 31, 2021.

- Depreciation of the mountain bikes purchased on July 8 and kayaks purchased on August 4 totals $8,700.

- Six months of the one-year insurance policy purchased on July 1 has expired.

- Four months of the one-year rental agreement purchased on September 1 has expired.

- Of the $1,800 of office supplies purchased on July 4, $320 remains.

- Interest expense on the $44,000 loan obtained from the city council on August 1 should be recorded.

- Of the $2,900 of racing supplies purchased on December 12, $260 remains.

- Suzie calculates that the company owes $14,700 in income taxes.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing Information Systems

Authors: Mario Piattini

1st Edition

1878289756, 9781878289759