Answered step by step

Verified Expert Solution

Question

1 Approved Answer

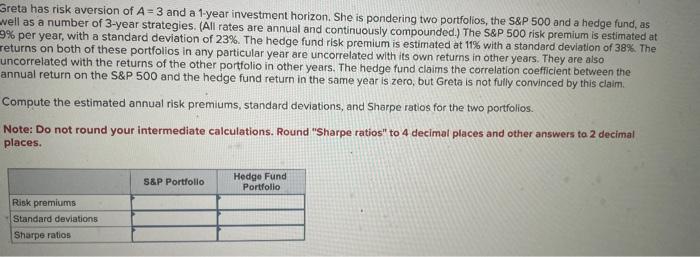

Greta has risk aversion of A=3 and a 1-year investment horizon. She is pondering two portfolios, the S&P 500 and a hedge fund, as vell

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Bank Behaviour And Resilience The Effect Of Structures Institutions And Agents

Authors: C. Bakir

1st Edition

0230202470,1137308168