Question: HALF & FULL A Venture Capital and LBO Case Study In December of 2010, Ms. Jennifer Half was walking her dog along the Lake Ontario

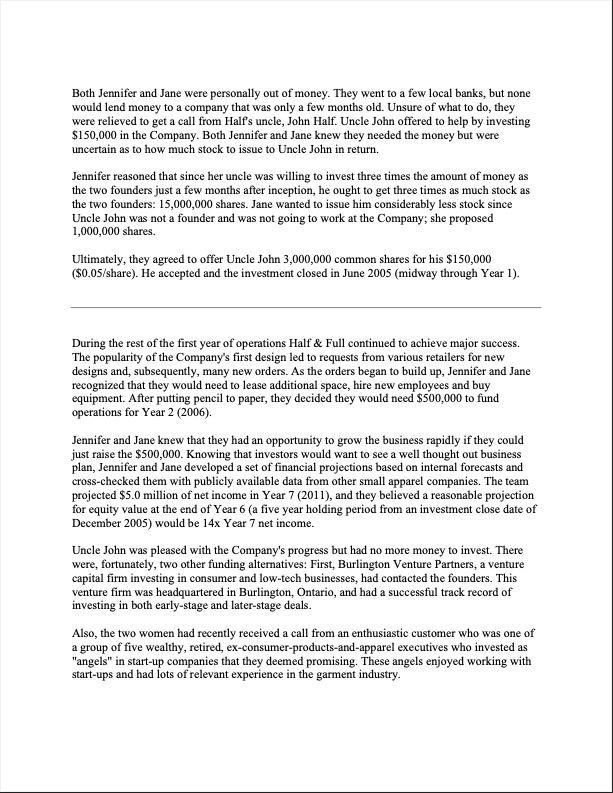

HALF & FULL A Venture Capital and LBO Case Study In December of 2010, Ms. Jennifer Half was walking her dog along the Lake Ontario shoreline, wondering what to do with her company, Half & Full, Inc. ("Half & Full"). As the co-founder and CEO of Half & Full, she felt she had built a successful business, handling many challenges over the past six years. Now, faced with the decision of whether to continue running the business or sell the company outright, she knew a poor decision might limit the future success of Half & Full. HISTORY Half had always enjoyed designing clothing. After graduating from McMaster in 2004, she decided to go into business with her best friend from school, Ms. Jane Full. They pulled together all the money they had and formed Half & Full, an apparel company for women, in January 2005 (the beginning of Year 1). Half contributed $30,000 and Full contributed $20,000. They were the only two founders and each "bought" founder stock at $0.01/share. As such, the initial capitalization and ownership of the Company was as follows: Shareholders Price Capital Shares Contributed Jennifer Half 3,000,000 $0.01 $30,000 Jane Full 2,000,000 $0.01 $20,000 Total 5,000,000 $50.000 Half & Full quickly became a success. The Company's first design, an evening gown decorated with Mac the Marauder, was well received by local retailers. Working at a feverish pace, the two women sewed these first dresses themselves and shipped their first order by the end of January. Additional orders were received soon thereafter. Exhausted after delivering the first order, Jennifer and Jane were horrified to realize that they were already nearly out of money - the fabric had cost over $30,000 and to keep up with demand they needed to buy high-powered cutting and sewing machines which would cost $80,000. Not expecting payment on the dresses for 90 days, they became concerned.Both Jennifer and Jane were personally out of money. They went to a few local banks, but none would lend money to a company that was only a few months old. Unsure of what to do, they were relieved to get a call from Half's uncle, John Half. Uncle John offered to help by investing $150,000 in the Company. Both Jennifer and Jane knew they needed the money but were uncertain as to how much stock to issue to Uncle John in return. Jennifer reasoned that since her uncle was willing to invest three times the amount of money as the two founders just a few months after inception, he ought to get three times as much stock as the two founders: 15,000,000 shares. Jane wanted to issue him considerably less stock since Uncle John was not a founder and was not going to work at the Company; she proposed 1,000,000 shares. Ultimately, they agreed to offer Uncle John 3,000,000 common shares for his $150,000 ($0.05/share). He accepted and the investment closed in June 2005 (midway through Year 1). During the rest of the first year of operations Half & Full continued to achieve major success. The popularity of the Company's first design led to requests from various retailers for new designs and, subsequently, many new orders. As the orders began to build up, Jennifer and Jane recognized that they would need to lease additional space, hire new employees and buy equipment. After putting pencil to paper, they decided they would need $500,000 to fund operations for Year 2 (2006). Jennifer and Jane knew that they had an opportunity to grow the business rapidly if they could just raise the $500,000. Knowing that investors would want to see a well thought out business plan, Jennifer and Jane developed a set of financial projections based on internal forecasts and cross-checked them with publicly available data from other small apparel companies. The team projected $5.0 million of net income in Year 7 (2011), and they believed a reasonable projection for equity value at the end of Year 6 (a five year holding period from an investment close date of December 2005) would be 14x Year 7 net income. Uncle John was pleased with the Company's progress but had no more money to invest. There were, fortunately, two other funding alternatives: First, Burlington Venture Partners, a venture capital firm investing in consumer and low-tech businesses, had contacted the founders. This venture firm was headquartered in Burlington, Ontario, and had a successful track record of investing in both early-stage and later-stage deals. Also, the two women had recently received a call from an enthusiastic customer who was one of a group of five wealthy, retired, ex-consumer-products-and-apparel executives who invested as "angels" in start-up companies that they deemed promising. These angels enjoyed working with start-ups and had lots of relevant experience in the garment industry.After meeting with the angel investors, Jennifer and Jane were leaning towards accepting the angel-funding alternative. The angels seemed to understand the apparel business and had some great ideas how to improve and grow Half & Full. The angels thought Jennifer and Jane were talented and energetic, and the angels thought that the financial projections were reasonable. Jennifer and Jane understood that angels generally require a 70% internal rate of return on their investments. In anticipation of their next meeting the two women decided to model the impact on the Company's capitalization of raising $500,000 from the angels in December 2005. The second meeting with the angels went even better than the first, and Jennifer and Jane invited the angels to invest on the terms calculated above. The angels, however, had one major concern: the deal did not meet their hurdle rate. The angels explained that in order for the Company to achieve its financial projections, the Company was almost certainly going to have to raise an additional $2,500,000 at the end of Year 2, thereby diluting the angels' ownership position. Such a large amount of money would most likely come from a venture capital firm. Unlike Jennifer and Jane's earlier calculation, the angels wanted a 70% IRR after taking into account this anticipated dilution. Jennifer and Jane quickly revised their calculation to understand the impact of these new terms on the Company's capitalization. Despite the less attractive terms, Jennifer and Jane still thought that their best course of action was to work with the angels, and the angels made a $500,000 investment in December 2005. Jennifer and Jane were initially able to grow their Company as they had hoped. They moved into larger offices, hired additional staff, expanded the number of designs they offered and increased the number of retailers they serviced. However, cash remained tight given how quickly Half & Full was growing and the resulting working capital needs of the business. Throughout 2006 (Year 2), as the company recorded success after success, Burlington Venture Partners stayed in touch with Jennifer and Jane, hoping that the Company might once again seek to raise outside capital. In August 2006, Half & Full secured Clothes "R" Us, a major American retailer, as their first major national reseller. This was their big break! Jennifer and Jane were at first delighted, but after reviewing the proposed contract, they concluded that Half & Full did not have the resources required to adequately support this new, large customer. They estimated that the Company would need $3.0 million to meet its obligations under the contract. Once again, Jennifer and Jane would have to seek outside capital. They consulted their angel investors who advised that now was the right time to raise venture capital from an institutional investor. After preliminary due diligence focused on the quality of the founding team, the market potential of the business, and the major trends and risk factors in women's apparel, Burlington VenturePartners expressed an interest in investing but thought the Company might need significantly more than $3.0 million to achieve its milestones. Burlington submitted a list of additional questions to Jennifer and Jane, in order to open a dialogue and resolve some of Burlington's outstanding diligence items. Jennifer and Jane were inclined to simply work with Burlington and conclude an investment deal quickly. However, the angels advised that it would be to the advantage of Half & Full to seek competitive offers from other venture capital firms. The angels provided several introductions and after numerous presentations to the VC firms, Jennifer and Jane received two firm investment proposals (known as "term sheets") - one from Burlington Venture Partners and one from DeGroote Venture Capital. The terms under which Burlington and DeGroote proposed to invest, however, were a bit more complicated than the relatively simple terms that had been acceptable to Uncle John and the angels. As is customary in venture capital deals, both firms proposed to purchase Series A convertible preferred stock. "Series A" meant it was the first series of preferred stock to be sold by Half & Full. As preferred stock, it would have a senior claim to all of the assets of Half & Full and it would also contain a number of features that are typical of a preferred security. Moreover, the investment terms proposed by Burlington were considerably different than the terms proposed by DeGroote. For example, Burlington was offering to pay $3.00 per share, while DeGroote was offering to pay $3.75. The term sheets from the VC firms are attached as Exhibits I and II. Half & Full chose to accept Burlington's term sheet, and the investment was completed in December 2006. Soon thereafter, Jane Full announced that she would leave the Company in mid- 2007 to pursue an MBA in Toronto. The Board of Directors vested all of her stock. Realizing the need for additional professional management and heeding the Board's suggestion to strengthen the management team, Jennifer hired a VP of Finance and a Chief Operating Officer (COO). The COO was interested in Half & Full because of the challenges, excitement and potential financial upside and wanted to participate in the upside potential of the Company through equity incentives. The Board granted Quarter and the VP of Finance significant option packages from the option pool established in conjunction with Burlington's financing. However, despite the more experienced management team, and much to the chagrin of the partners at Burlington, several serious challenges arose at Half & Full within the first six months after their investment closed: a large customer who owed the company a significant amount of money asked for a six month payment moratorium; a supply contract with a second major national reseller (key to the Company's growth plans) was awarded to a competitor; and the VP of Finance reported that the distribution expansion project required more capital than originally budgeted. Combined, these factors would lead to a major cash shortfall by the first half of 2008.As Jennifer and her team assessed the increasingly challenging situation, they realized additional funding was needed to overcome the looming cash crunch and get the Company "back on track'. The managers saw two main alternatives: raise an additional $2.0 million by selling Series B preferred stock or seek a bank line of credit (most likely no more than $1,250,000). After some preliminary discussions, it was clear that all VCs would insist on harsher terms and a much lower company valuation when pricing the Series B round (a so-called "down round"). Similarly, all lenders would insist that the bank line contain onerous covenants requiring a significant reduction in operating expenses immediately. It was an ugly set of choices. After discussing each alternative, management and the Board of Directors decided to raise $2.0 million in venture capital. The Board of Directors was concerned that the bank loan would not be sufficient to cover the full funding need, leaving the company in the position of raising yet another round of capital on disadvantageous terms. Additionally, the Board noted that the Company had some key decisions on the horizon, and the bank's financial covenants might restrict the strategy or operations of the business more so than additional venture money, since venture investors would likely have a higher risk tolerance and be more focused on growth potential. Jennifer approached Burlington Ventures, as Burlington's knowledge of the Company, its deep pockets, and its desire to protect its initial investment made Burlington the most logical source of additional equity capital. At Burlington's Monday meeting, the deal team shared with their partners the disappointing news regarding Half & Full's need for additional capital. After discussing the team's recommendation, the partners authorized the negotiation of a term sheet to purchase $2.0 million of Series B preferred stock from Half & Full. In order to finalize the investment, the Burlington team worked with Jennifer to revise the Company's projections. After detailed analysis, they projected 2010 (Year 6) net income would be $4.0 million and projected 2011 (Year 7) net income would be $5.0 million. In determining the valuation and associated conversion price for the new Series B convertible preferred shares, Burlington and the Company negotiated and agreed to the following terms and conditions: $2 million cash investment (with the transaction to close at year-end 2007 - Year 3); $12.0 million pre-money valuation for the investment (as Burlington was targeting an IRR of just over 60% on the new investment assuming a 3-year holding period and an exit value of 12 times Year 7 net income); Exercise of the full-ratchet provision on the previous $3.5 million Series A investment; 3.0x senior liquidation preference on the new Series B investment (assuming that Series B does not receive dividends); and An additional seat on the Board of Directors.QUESTION 6 In the ensuing months and years, the Company overcame the cash crunch and experienced significant success. Half & Full aggressively expanded its international distribution infrastructure and built a few corporate-owned retail locations in the U.S. in high end shopping areas. The company showed the potential of becoming the next DKNY or Calvin Klein. Unexpectedly, in November 2010, two interested parties approached Half and proposed strategic transactions. Clothes "R" Us expressed interest in making a strategic investment and a private equity investment firm named Buyouts V asked Half if she would consider selling the entire Company in an all-cash transaction. Buyouts V had extensive experience in the apparel industry and had acquired several apparel companies over the years. Jennifer knew that Uncle John and the angel investors liked the idea of "cashing out" via an IPO or sale of the Company; some wanted to reinvest their profits into other early stage deals while others simply wanted to lock in a profit. Burlington Venture Partners, impressed with Jennifer's handling of the previous challenges, said the decision was up to her. Jennifer wasn't sure what she wanted herself. As she walked along the lake, she contemplated her options. Ultimately in early December 2010, Jennifer decided that an all-cash sale to Buyouts V could be very attractive. She expected that Buyouts V would place a high enterprise value on the firm and the Company had no debt. Jennifer was also beginning to worry that her management team might not be strong enough to run a much larger company, and prudence dictated that she get the best price she could now for the shareholders. Half called Buyouts V and told them she was open to considering an offer and would like them to present their offer at next week's Board meeting. The managers of Buyouts V (known as the "General Partners") strive to deliver an attractive rate of return to the investors in Buyouts V (known as "Limited Partners"). Buyout V's Limited Partners have traditionally required a 20% net IRR (i.e., after carried interest and assuming a 2% annual management fees over a 5-year investment horizon). Under the terms of the Buyouts V Partnership Agreement, the General Partners are entitled to a "carried interest" of 20% of the profits, or capital gain. Required: (6A) Given the target net return of 20% to the Limited Partners, what "deal-level" multiple of investment and IRR should Buyouts V target for the acquisition of Half and Full

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!