Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Hand written Answer please Question 1 (15 marks) Use the following information to answer a). WOW Ltd S&P/ASX 200 Monthly average return 1.25% 0.66% Standard

Hand written Answer please

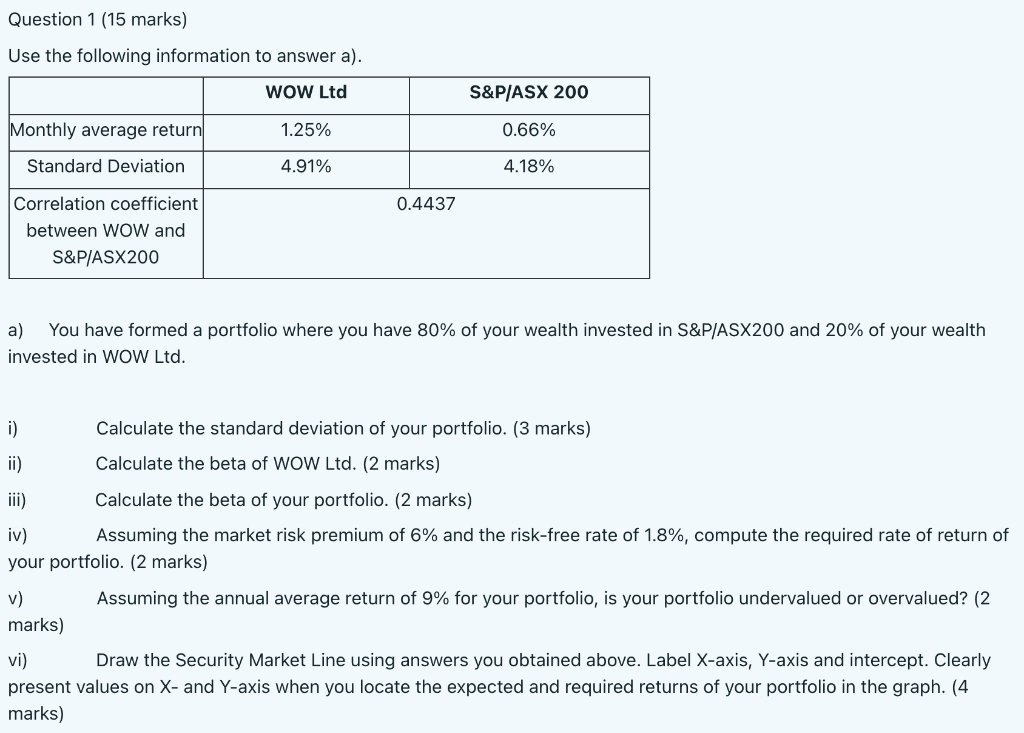

Question 1 (15 marks) Use the following information to answer a). WOW Ltd S&P/ASX 200 Monthly average return 1.25% 0.66% Standard Deviation 4.91% 4.18% 0.4437 Correlation coefficient between WOW and S&P/ASX200 a) You have formed a portfolio where you have 80% of your wealth invested in S&P/ASX200 and 20% of your wealth invested in WOW Ltd. i) ii) Calculate the standard deviation of your portfolio. (3 marks) Calculate the beta of WOW Ltd. (2 marks) Calculate the beta of your portfolio. (2 marks) iii) iv) Assuming the market risk premium of 6% and the risk-free rate of 1.8%, compute the required rate of return of your portfolio. (2 marks) v) Assuming the annual average return of 9% for your portfolio, is your portfolio undervalued or overvalued? (2 marks) vi) Draw the Security Market Line using answers you obtained above. Label X-axis, Y-axis and intercept. Clearly present values on - and Y-axis when you locate the expected and required returns of your portfolio in the graph. (4 marks)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Elements Of Structured Finance

Authors: Ann Rutledge, Sylvain Raynes

1st Edition

0195179986, 978-0195179989