Handout:

Handout:

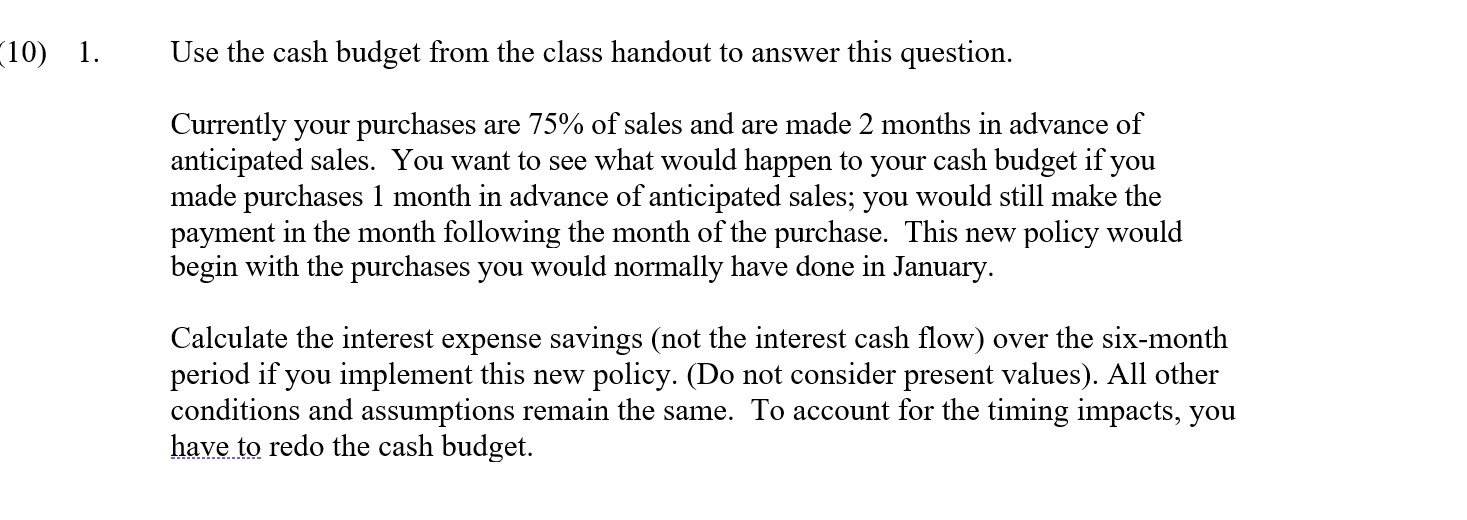

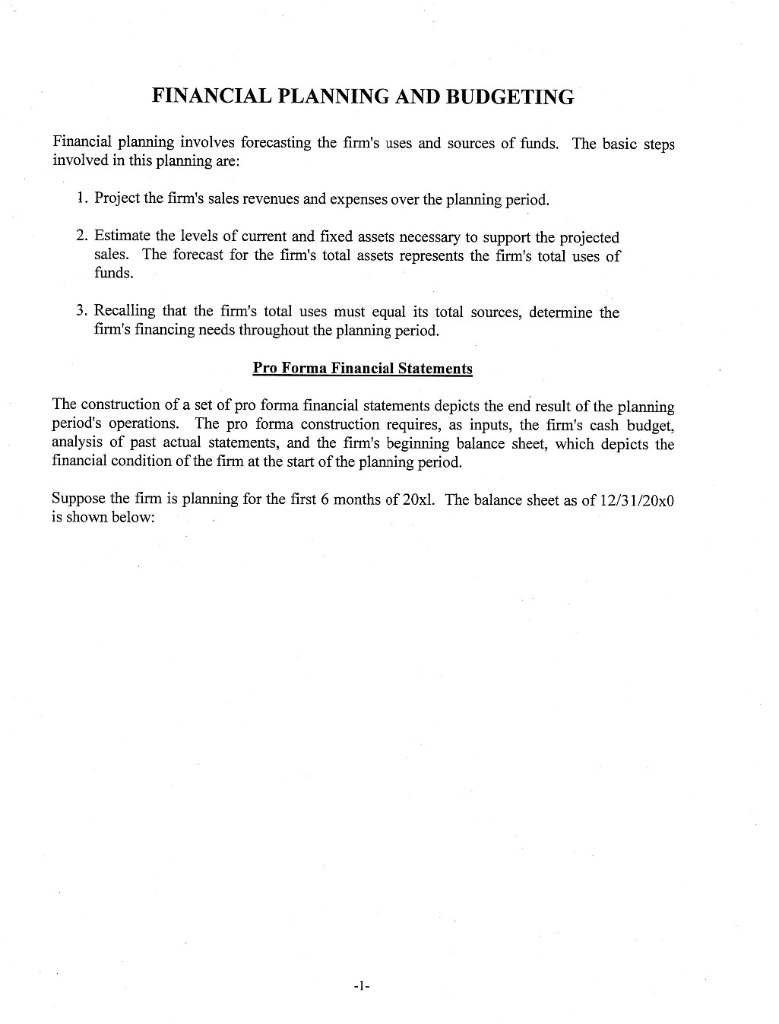

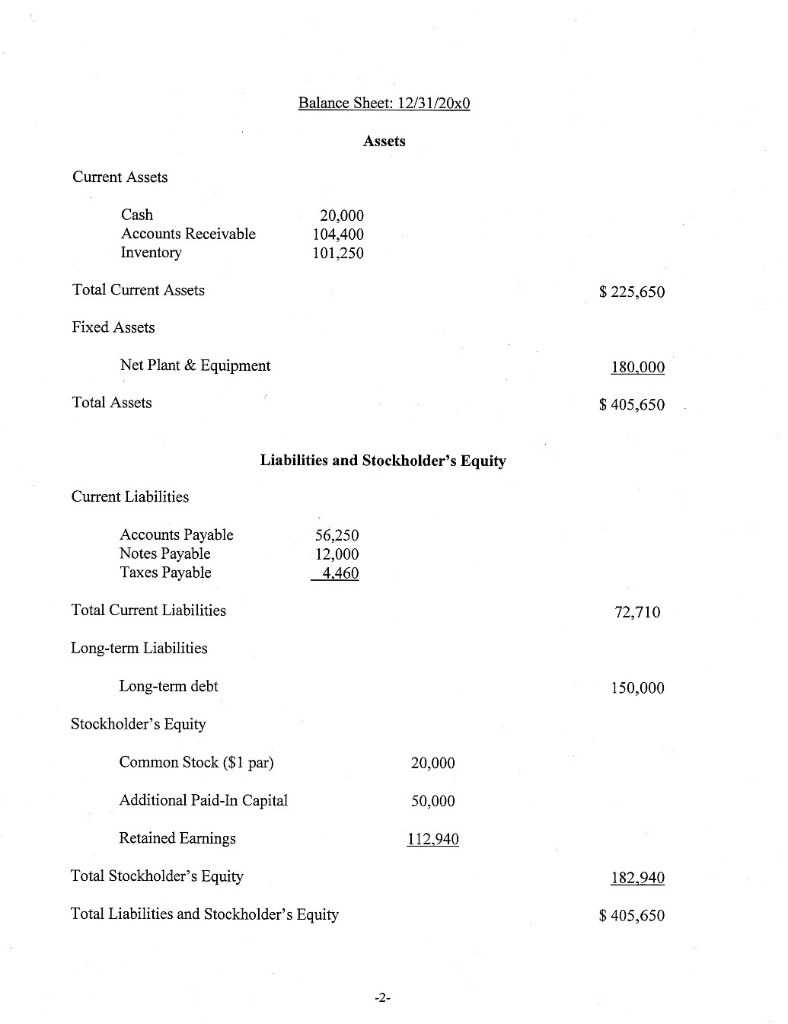

10) 1. Use the cash budget from the class handout to answer this question. Currently your purchases are 75% of sales and are made 2 months in advance of anticipated sales. You want to see what would happen to your cash budget if you made purchases 1 month in advance of anticipated sales; you would still make the payment in the month following the month of the purchase. This new policy would begin with the purchases you would normally have done in January. Calculate the interest expense savings (not the interest cash flow) over the six-month period if you implement this new policy. (Do not consider present values). All other conditions and assumptions remain the same. To account for the timing impacts, you have to redo the cash budget. FINANCIAL PLANNING AND BUDGETING Financial planning involves forecasting the firm's uses and sources of funds. The basic steps involved in this planning are: 1. Project the firm's sales revenues and expenses over the planning period. 2. Estimate the levels of current and fixed assets necessary to support the projected sales. The forecast for the firm's total assets represents the firm's total uses of funds. 3. Recalling that the firm's total uses must equal its total sources, determine the firm's financing needs throughout the planning period. Pro Forma Financial Statements The construction of a set of pro forma financial statements depicts the end result of the planning period's operations. The pro forma construction requires, as inputs, the firm's cash budget, analysis of past actual statements, and the firm's beginning balance sheet, which depicts the financial condition of the firm at the start of the planning period. Suppose the firm is planning for the first 6 months of 20xl. The balance sheet as of 12/31/20x0 is shown below: -1- Balance Sheet: 12/31/20x0 Assets Current Assets Cash Accounts Receivable Inventory 20,000 104,400 101.250 Total Current Assets $ 225,650 Fixed Assets Net Plant & Equipment 180,000 Total Assets $ 405,650 Liabilities and Stockholder's Equity Current Liabilities Accounts Payable Notes Payable Taxes Payable 56,250 12.000 4,460 Total Current Liabilities 72,710 Long-term Liabilities Long-term debt 150,000 Stockholder's Equity Common Stock ($1 par) 20,000 Additional Paid-In Capital 50,000 Retained Earnings 112,940 Total Stockholder's Equity 182,940 Total Liabilities and Stockholder's Equity $ 405,650 -2- Determining the Pro Forma Income Statement: The pro forma income statement predicts the profit or loss for the planning period. Much of the information comes from the firm's cash budgeting process. An example, with the source of each item identified, is below: Pro Forma Income Statement 1/1/20x1 to 6/30/20x1 Sales from cash budget and sales plan $533,000 Cost of Goods Sold determined to be 75% of sales 399.750 Gross Profit 133,250 Operating Expenses Depreciation Wages & Salaries Rent Other Expenses Total from fixed assets and depreciation schedules from cash budget from cash budget from cash budget 8,830 38,000 24,000 6,900 77.730 Net Operating Income (EBIT) 55,520 Interest Expense from debt obligations 11,764 Earnings Before Taxes (EBT) 43,756 Taxes 40% tax rate 17,502 Net Income (EAT) $26,254 -3- Determining the Proforma Balance Sheet: The pro forma balance sheet relies on the information from the cash budget, the beginning balance sheet, and the pro forma income statement. Each account is predicted by looking at its initial value, estimating what will cause it to change, and then determining the ending value. Doing this for each account in the balance sheet is illustrated below: Cash: the firm desires a balance of $10,000; this ending value was also the ending value from the cash budget 12/31/20x0 Accounts Receivable: + Credit Sales Collections Accounts Receivable 104,400 +533,000 -440.400 from cash budget 6/30/20x1 $ 197,000 Inventory: + Purchases Cost of Good Sold Inventory 12/31/20x0 from cash budget from pro forma income stmt. 6/30/20x1 101,250 +414,750 -399.750 $ 116,250 12/31/20x0 180,000 Net Plant & Equip. + Purchases of Plant and Equipment Depreciation Exp. Net Plant & Equip from cash budget from pro forma income stmt. 6/30/20x1 +14,000 - 8.830 $ 185,170 12/31/20x0 Accounts Payable + Purchases Payment Accounts Payable from cash budget 6/30/20x1 56,250 + 414,750 - 414.750 $ 56,250 Notes Payable + Borrowing Payments Notes Payable 12/31/20x0 none planned-to be determined from cash budget 6/30/20x1 12,000 + 0 - 12.000 $ 0 + 0 Accrued Interest + Interest Expense Not Yet Paid Accrued Interest 12/31/20x0 from cash budget + 6/30/20x1 799 799 $ 4,460 +17,502 Taxes Payable + Tax Liability for the period - Tax Payment Taxes Payable 12/31/20x0 from pro forma income statement from cash budget 6/30/20x1 - 9.660 $ 12,302 -4- Long-Term Debt + New Borrowings - Payments Long-Term Debt 12/31/20x0 from cash budget from cash budget 6/30/20x1 150,000 + 0 0 $ 150,000 12/31/20x0 from cash budget 70,000 + 0 Common Stock and Additional Paid-In Capital + New Issues - Retirement (Treasury Stock Purchases) Common Stock and Additional Paid-In capital from cash budget + 0 6/30/20x1 $ 70,000 Retained Earnings + Net Income - Dividends Retained Earnings 12/31/20x0 from pro forma income statement from cash budget 6/30/20x1 $ 112,940 26,254 0 $ 139,194 Comparing the forecast values for total. assets and for all the liability and stockholders' equity accounts allows us to determine the value for additional financing necessary; that is: Additional Financing Necessary = Total Assets - (Total Current Liabilities + Long-Term Debt + Common Stock and Paid-In Capital + Retained Earnings) Additional Financing Necessary = $508,420 -(69,351 + 150,000 + 70,000 + 139,194) = $508,420 - $428,545 = $79,875 In this example, the firm must determine a source for the $79,875 of additional financing necessary. We will assume that the source will be Notes Payable. Thus, the final value for Notes Payable will be the original forecast value of: $0 + $79,875 = $79,875. The complete pro forma balance sheet for 6/30/20xl can now be shown below: Pro Forma Balance Sheet 6/30/20xl Assets: Current Assets Cash Accounts Receivable Inventory 10,000 197,000 116.250 Total current Assets 323,250 Fixed Assets Net Plant and Equipment 185,170 Total Assets $508,420 Liablilities and Stockholder's Equity: Current Liabilities Accounts Payable Notes Payable Accrued Interest Taxes Payable 56,250 79,875 799 12,302 Total Current Liabilities 149,226 Long-term Liabilities Long-term Debt 150,000 Stockholder's Equity 209,194 Common Stock ($1 par) Additional Paid-in cap. Retained Earnings 20,000 50,000 139,194 Total Stockholder's Equity 209,194 Total Liabilities and Stockholder's Equity $ 508,420 CASH PLANNING The management of cash is critical to the life of any organization. Unfortunately, there are many examples of profitable firms that have gone bankrupt! How can this be? Profits are not necessarily cash. There may be large time discrepancies between the accountant's recording of earned profit and the firm's receipt of cash. The monitoring of the firm's cash position requires the creation of the cash budget. Cash Budget The cash budget represents a detailed plan of the firm's future cash flows and is composed of four elements: cash receipts, cash disbursements, net change in cash for the period, and new financing needed. Since the cash position is so important, the planning period for the cash budget is usually shorter than for other budgets. The cash budget is usually calculated monthly. The cash budget concept is illustrated with an example that covers a 6-month planning horizon with 6 monthly cash budgets. The example firm has highly seasonal sales, with sales peaking in the months of March through May. All sales are sold on a credit basis. The firm collects on these accounts receivable in the following pattern: 30% collected in the month following the month of the sale, 50% collected two months after the sale, and 20% collected during the third month after the sale. The firm attempts to match its purchases of materials with its forecast for future sales. Purchases equal 75% of sales and are made 2 months in advance of anticipated sales. Payments for purchases are made in the month following the month of the purchases. Wages, salaries, rent and other cash expenses are recorded in the months and amounts expected. Additional cash expenditures of $14,000 in February for capital equipment and the repayment in May of a $12,000 short-term note payable are also recorded. In June, the firm will pay $7,500 interest on its $150,000 of long-term debt. Interest on the $12,000 short-term note is $600 and will be paid in May. Cash payments for taxes will be $4460 in March and $5200 in June. The firm presently (12/31/20x0) has a cash balance of $20,000 and wants to maintain a minimum cash balance of $10,000. Any borrowing necessary to maintain this balance is calculated in the cash budget. It is assumed that borrowing takes place at the beginning of the month in which funds are needed. In this example, interest on borrowed funds equals 12% per year or 1% per month and is paid in the month following the month in which funds are borrowed. In the illustration below, the Financing Needed line on the cash budget indicates that the firm will need to borrow $36,350 in February, $29,524 in March, $20,759 in April and $10,966 in May. Only in June will the firm be able to reduce its cumulative borrowing down to $79,875. It is important to note that the cash budget indicates not only the amount of financing needed during the period, but it also shows when the funds will be needed. The information below shows the monthly sales forecast for the 6-month planning horizon. The actual sales figures for October, November, and December were $55,000, $62,000, and $50,000. Sales Forecast Month Sales Month Sales January February March $60,000 $75,000 $88,000 April May June $100,000 $110,000 $100,000 The format for the cash budget is illustrated below: Month (1) Cash Receipts (2) Cash Disbursements (3) Net Monthly Cash Change (or Cash Flow) (4) + Beginning Cash Balance (5) Ending Cash Balance (without Borrowing) (6) - Desired Cash Balance (7) Surplus Cash (if this figure is positive) OR Financing Needed (if this figure is negative) NOTE: Item numbers correspond to the budget on the next page. Cash receipts are all the inflows of cash into the organization. Examples of items that cause cash to flow into the organization include: 1. 2. 3. 4. 5. 6. 7. 8. Cash sales Collections of accounts receivable Receipt of interest Receipt of dividends Sale of marketable securities Sale of fixed assets Proceeds from borrowings Proceeds from stock issues Cash disbursements are all the outflows of cash from the organization. Examples of items that cause cash to flow out of the organization include: 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. Cash purchases Payments of accounts payable Payments for wages and salaries Payments for expenses such as rent, utilities, insurance, etc. Interest payments Dividend payments Tax payments Purchases of marketable securities Purchases of fixed assets Repayment of borrowings Retirement of stock Cash Receipts from Sales: NOV DEC JAN FEB MAR APR MAY JUNE Sales $55,000 $62,000 $50,000 $60,000 $75,000 $88,000 $100,000 $110,000 $100,000 Collections of December Sales: First month (30%) 15,000 Second month (50%) 25,000 Third month (20%) 10,000 OCT NOV DEC JAN FEB MAR APR MAY JUNE* Sales $55,000 $62,000 $50,000 $60,000 $75,000 $88,000 $100,000 $110,000 $100,000 Collections: First month (30%) 15,000 18,000 22,500 26,400 30,000 33,000 Second month (50%) 31,000 25,000 30,000 37,500 44,000 50,000 Third month (20%) 11,000 12.400 10,000 12,000 15,000 17,600 Total Collections 57,000 55,400 62,500 75,900 89,000 100,600 * At the end of June, the firm will have accounts receivable of (-20) (100,000) from April, (.70)(110,000) from May, and 100,000 from June for a total of $197,000. Purchases and Payments: OCT NOV DEC JAN FEB MAR APR MAY JUNE Sales $55,000 $62,000 $50,000 $60,000 $75,000 $88,000 $100,000 $110,000 $100,000 Purchases (75% future 2 months) 66,000 Payments (post, 1 month) 66,000 Purchases 56,250 66,000 75,000 82,500 75,000 60,000* 56,250* Payments 56,250 66,000 75,000 82,500 75,000 60,000 *These numbers are based on forecast sales of $80,000 for July and $75,000 for August. CASH-BUDGET JAN FEB MAR APR MAY JUNE (1) Cash Receipts: Total Collections $57,000 $55,400 $62,500 $75,900 $89,000 $100,600 (2) Cash Disbursements: 56,250 3,000 4,000 1,000 66,000 10,000 4,000 500 75,000 7,000 4,000 1,200 82,500 8,000 4,000 1,500 75,000 6,000 4,000 1,500 600 Purchases Wages and Salaries Rent Other Expenses Interest Expense (Existing Debt) Taxes Purchases of Equipment Loan Repayment Total Disbursements 60,000 4,000 4,000 1,200 7,500 4,460 5,200 14,000 64,250 12.000 99,100 94,500 91,660 96,000 81,900 (3) Cash Flow: (=Receipts-Disbursents) (7,250) (39,100) (29,160) (20,100) (10,100) 18,700 (4) Plus: Beginning Cash Balance 20,000 12,750 10,000 10,000 10,000 10,000 Net: Excess (or Deficit) 12,750 (26,350) (19,160) (10,100) (100) 28,700 Less: Interest on Short-term Borrowing (@1%/mo.): 364 659 866 976 (5) Equals: Ending Cash Balance without borrowing: 12,750 (26,350) (19,524) (10,759) (966) 27,724 (6) Desired Cash Balance: 10,000 10,000 10,000 10,000 10,000 10,000 (7) Surplus/Fin. Needed* 2,750 (36,350) (29,524) (20,759) (10,966) 17,724 Cumulative borrowing 0 36,350 65,874 86,633 97,599 79,875** * The Financing Needed is the amount of financing required to raise'the firm's ending cash balance to the $10,000 desired cash balance. A positive figure for Financing Needed means the firm has excess cash that can retire prior short-term borrowing or be used for investing; in this example, the excess cash in June repaid borrowing. ** This figure results in accrued interest (interest obligated for the month of June but not yet paid) of $799. Statement of Cash Flows For Six-Months Ended 6/30/20x1 $26, 254 Cash flows from operating activities (indirect method) Net Income Adjustments for differences between income flows and Cash flows from operating activities Depreciation expense Increase in accounts receivable Increase in inventory Increase in accounts payable Increase in accrued interest Increase in taxes payable Net cash from operating activities 8,830 (92,600) (15,000) 0 799 7,842 (63,875) Cash flows from investing activities Payment for equipment Net cash used for investing activities (14,000) (14,000) Cash flows from financing activities Increase in notes payable Payment of dividends Increase in long-term debt Increase in common stock Net cash from financing activities 67,875 0 0 0 67,875 Net increase in cash Plus: cash balance, 12/31/20x0 Cash balance, 6/30/20x1 (10,000) 20,000 $10,000 10) 1. Use the cash budget from the class handout to answer this question. Currently your purchases are 75% of sales and are made 2 months in advance of anticipated sales. You want to see what would happen to your cash budget if you made purchases 1 month in advance of anticipated sales; you would still make the payment in the month following the month of the purchase. This new policy would begin with the purchases you would normally have done in January. Calculate the interest expense savings (not the interest cash flow) over the six-month period if you implement this new policy. (Do not consider present values). All other conditions and assumptions remain the same. To account for the timing impacts, you have to redo the cash budget. FINANCIAL PLANNING AND BUDGETING Financial planning involves forecasting the firm's uses and sources of funds. The basic steps involved in this planning are: 1. Project the firm's sales revenues and expenses over the planning period. 2. Estimate the levels of current and fixed assets necessary to support the projected sales. The forecast for the firm's total assets represents the firm's total uses of funds. 3. Recalling that the firm's total uses must equal its total sources, determine the firm's financing needs throughout the planning period. Pro Forma Financial Statements The construction of a set of pro forma financial statements depicts the end result of the planning period's operations. The pro forma construction requires, as inputs, the firm's cash budget, analysis of past actual statements, and the firm's beginning balance sheet, which depicts the financial condition of the firm at the start of the planning period. Suppose the firm is planning for the first 6 months of 20xl. The balance sheet as of 12/31/20x0 is shown below: -1- Balance Sheet: 12/31/20x0 Assets Current Assets Cash Accounts Receivable Inventory 20,000 104,400 101.250 Total Current Assets $ 225,650 Fixed Assets Net Plant & Equipment 180,000 Total Assets $ 405,650 Liabilities and Stockholder's Equity Current Liabilities Accounts Payable Notes Payable Taxes Payable 56,250 12.000 4,460 Total Current Liabilities 72,710 Long-term Liabilities Long-term debt 150,000 Stockholder's Equity Common Stock ($1 par) 20,000 Additional Paid-In Capital 50,000 Retained Earnings 112,940 Total Stockholder's Equity 182,940 Total Liabilities and Stockholder's Equity $ 405,650 -2- Determining the Pro Forma Income Statement: The pro forma income statement predicts the profit or loss for the planning period. Much of the information comes from the firm's cash budgeting process. An example, with the source of each item identified, is below: Pro Forma Income Statement 1/1/20x1 to 6/30/20x1 Sales from cash budget and sales plan $533,000 Cost of Goods Sold determined to be 75% of sales 399.750 Gross Profit 133,250 Operating Expenses Depreciation Wages & Salaries Rent Other Expenses Total from fixed assets and depreciation schedules from cash budget from cash budget from cash budget 8,830 38,000 24,000 6,900 77.730 Net Operating Income (EBIT) 55,520 Interest Expense from debt obligations 11,764 Earnings Before Taxes (EBT) 43,756 Taxes 40% tax rate 17,502 Net Income (EAT) $26,254 -3- Determining the Proforma Balance Sheet: The pro forma balance sheet relies on the information from the cash budget, the beginning balance sheet, and the pro forma income statement. Each account is predicted by looking at its initial value, estimating what will cause it to change, and then determining the ending value. Doing this for each account in the balance sheet is illustrated below: Cash: the firm desires a balance of $10,000; this ending value was also the ending value from the cash budget 12/31/20x0 Accounts Receivable: + Credit Sales Collections Accounts Receivable 104,400 +533,000 -440.400 from cash budget 6/30/20x1 $ 197,000 Inventory: + Purchases Cost of Good Sold Inventory 12/31/20x0 from cash budget from pro forma income stmt. 6/30/20x1 101,250 +414,750 -399.750 $ 116,250 12/31/20x0 180,000 Net Plant & Equip. + Purchases of Plant and Equipment Depreciation Exp. Net Plant & Equip from cash budget from pro forma income stmt. 6/30/20x1 +14,000 - 8.830 $ 185,170 12/31/20x0 Accounts Payable + Purchases Payment Accounts Payable from cash budget 6/30/20x1 56,250 + 414,750 - 414.750 $ 56,250 Notes Payable + Borrowing Payments Notes Payable 12/31/20x0 none planned-to be determined from cash budget 6/30/20x1 12,000 + 0 - 12.000 $ 0 + 0 Accrued Interest + Interest Expense Not Yet Paid Accrued Interest 12/31/20x0 from cash budget + 6/30/20x1 799 799 $ 4,460 +17,502 Taxes Payable + Tax Liability for the period - Tax Payment Taxes Payable 12/31/20x0 from pro forma income statement from cash budget 6/30/20x1 - 9.660 $ 12,302 -4- Long-Term Debt + New Borrowings - Payments Long-Term Debt 12/31/20x0 from cash budget from cash budget 6/30/20x1 150,000 + 0 0 $ 150,000 12/31/20x0 from cash budget 70,000 + 0 Common Stock and Additional Paid-In Capital + New Issues - Retirement (Treasury Stock Purchases) Common Stock and Additional Paid-In capital from cash budget + 0 6/30/20x1 $ 70,000 Retained Earnings + Net Income - Dividends Retained Earnings 12/31/20x0 from pro forma income statement from cash budget 6/30/20x1 $ 112,940 26,254 0 $ 139,194 Comparing the forecast values for total. assets and for all the liability and stockholders' equity accounts allows us to determine the value for additional financing necessary; that is: Additional Financing Necessary = Total Assets - (Total Current Liabilities + Long-Term Debt + Common Stock and Paid-In Capital + Retained Earnings) Additional Financing Necessary = $508,420 -(69,351 + 150,000 + 70,000 + 139,194) = $508,420 - $428,545 = $79,875 In this example, the firm must determine a source for the $79,875 of additional financing necessary. We will assume that the source will be Notes Payable. Thus, the final value for Notes Payable will be the original forecast value of: $0 + $79,875 = $79,875. The complete pro forma balance sheet for 6/30/20xl can now be shown below: Pro Forma Balance Sheet 6/30/20xl Assets: Current Assets Cash Accounts Receivable Inventory 10,000 197,000 116.250 Total current Assets 323,250 Fixed Assets Net Plant and Equipment 185,170 Total Assets $508,420 Liablilities and Stockholder's Equity: Current Liabilities Accounts Payable Notes Payable Accrued Interest Taxes Payable 56,250 79,875 799 12,302 Total Current Liabilities 149,226 Long-term Liabilities Long-term Debt 150,000 Stockholder's Equity 209,194 Common Stock ($1 par) Additional Paid-in cap. Retained Earnings 20,000 50,000 139,194 Total Stockholder's Equity 209,194 Total Liabilities and Stockholder's Equity $ 508,420 CASH PLANNING The management of cash is critical to the life of any organization. Unfortunately, there are many examples of profitable firms that have gone bankrupt! How can this be? Profits are not necessarily cash. There may be large time discrepancies between the accountant's recording of earned profit and the firm's receipt of cash. The monitoring of the firm's cash position requires the creation of the cash budget. Cash Budget The cash budget represents a detailed plan of the firm's future cash flows and is composed of four elements: cash receipts, cash disbursements, net change in cash for the period, and new financing needed. Since the cash position is so important, the planning period for the cash budget is usually shorter than for other budgets. The cash budget is usually calculated monthly. The cash budget concept is illustrated with an example that covers a 6-month planning horizon with 6 monthly cash budgets. The example firm has highly seasonal sales, with sales peaking in the months of March through May. All sales are sold on a credit basis. The firm collects on these accounts receivable in the following pattern: 30% collected in the month following the month of the sale, 50% collected two months after the sale, and 20% collected during the third month after the sale. The firm attempts to match its purchases of materials with its forecast for future sales. Purchases equal 75% of sales and are made 2 months in advance of anticipated sales. Payments for purchases are made in the month following the month of the purchases. Wages, salaries, rent and other cash expenses are recorded in the months and amounts expected. Additional cash expenditures of $14,000 in February for capital equipment and the repayment in May of a $12,000 short-term note payable are also recorded. In June, the firm will pay $7,500 interest on its $150,000 of long-term debt. Interest on the $12,000 short-term note is $600 and will be paid in May. Cash payments for taxes will be $4460 in March and $5200 in June. The firm presently (12/31/20x0) has a cash balance of $20,000 and wants to maintain a minimum cash balance of $10,000. Any borrowing necessary to maintain this balance is calculated in the cash budget. It is assumed that borrowing takes place at the beginning of the month in which funds are needed. In this example, interest on borrowed funds equals 12% per year or 1% per month and is paid in the month following the month in which funds are borrowed. In the illustration below, the Financing Needed line on the cash budget indicates that the firm will need to borrow $36,350 in February, $29,524 in March, $20,759 in April and $10,966 in May. Only in June will the firm be able to reduce its cumulative borrowing down to $79,875. It is important to note that the cash budget indicates not only the amount of financing needed during the period, but it also shows when the funds will be needed. The information below shows the monthly sales forecast for the 6-month planning horizon. The actual sales figures for October, November, and December were $55,000, $62,000, and $50,000. Sales Forecast Month Sales Month Sales January February March $60,000 $75,000 $88,000 April May June $100,000 $110,000 $100,000 The format for the cash budget is illustrated below: Month (1) Cash Receipts (2) Cash Disbursements (3) Net Monthly Cash Change (or Cash Flow) (4) + Beginning Cash Balance (5) Ending Cash Balance (without Borrowing) (6) - Desired Cash Balance (7) Surplus Cash (if this figure is positive) OR Financing Needed (if this figure is negative) NOTE: Item numbers correspond to the budget on the next page. Cash receipts are all the inflows of cash into the organization. Examples of items that cause cash to flow into the organization include: 1. 2. 3. 4. 5. 6. 7. 8. Cash sales Collections of accounts receivable Receipt of interest Receipt of dividends Sale of marketable securities Sale of fixed assets Proceeds from borrowings Proceeds from stock issues Cash disbursements are all the outflows of cash from the organization. Examples of items that cause cash to flow out of the organization include: 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. Cash purchases Payments of accounts payable Payments for wages and salaries Payments for expenses such as rent, utilities, insurance, etc. Interest payments Dividend payments Tax payments Purchases of marketable securities Purchases of fixed assets Repayment of borrowings Retirement of stock Cash Receipts from Sales: NOV DEC JAN FEB MAR APR MAY JUNE Sales $55,000 $62,000 $50,000 $60,000 $75,000 $88,000 $100,000 $110,000 $100,000 Collections of December Sales: First month (30%) 15,000 Second month (50%) 25,000 Third month (20%) 10,000 OCT NOV DEC JAN FEB MAR APR MAY JUNE* Sales $55,000 $62,000 $50,000 $60,000 $75,000 $88,000 $100,000 $110,000 $100,000 Collections: First month (30%) 15,000 18,000 22,500 26,400 30,000 33,000 Second month (50%) 31,000 25,000 30,000 37,500 44,000 50,000 Third month (20%) 11,000 12.400 10,000 12,000 15,000 17,600 Total Collections 57,000 55,400 62,500 75,900 89,000 100,600 * At the end of June, the firm will have accounts receivable of (-20) (100,000) from April, (.70)(110,000) from May, and 100,000 from June for a total of $197,000. Purchases and Payments: OCT NOV DEC JAN FEB MAR APR MAY JUNE Sales $55,000 $62,000 $50,000 $60,000 $75,000 $88,000 $100,000 $110,000 $100,000 Purchases (75% future 2 months) 66,000 Payments (post, 1 month) 66,000 Purchases 56,250 66,000 75,000 82,500 75,000 60,000* 56,250* Payments 56,250 66,000 75,000 82,500 75,000 60,000 *These numbers are based on forecast sales of $80,000 for July and $75,000 for August. CASH-BUDGET JAN FEB MAR APR MAY JUNE (1) Cash Receipts: Total Collections $57,000 $55,400 $62,500 $75,900 $89,000 $100,600 (2) Cash Disbursements: 56,250 3,000 4,000 1,000 66,000 10,000 4,000 500 75,000 7,000 4,000 1,200 82,500 8,000 4,000 1,500 75,000 6,000 4,000 1,500 600 Purchases Wages and Salaries Rent Other Expenses Interest Expense (Existing Debt) Taxes Purchases of Equipment Loan Repayment Total Disbursements 60,000 4,000 4,000 1,200 7,500 4,460 5,200 14,000 64,250 12.000 99,100 94,500 91,660 96,000 81,900 (3) Cash Flow: (=Receipts-Disbursents) (7,250) (39,100) (29,160) (20,100) (10,100) 18,700 (4) Plus: Beginning Cash Balance 20,000 12,750 10,000 10,000 10,000 10,000 Net: Excess (or Deficit) 12,750 (26,350) (19,160) (10,100) (100) 28,700 Less: Interest on Short-term Borrowing (@1%/mo.): 364 659 866 976 (5) Equals: Ending Cash Balance without borrowing: 12,750 (26,350) (19,524) (10,759) (966) 27,724 (6) Desired Cash Balance: 10,000 10,000 10,000 10,000 10,000 10,000 (7) Surplus/Fin. Needed* 2,750 (36,350) (29,524) (20,759) (10,966) 17,724 Cumulative borrowing 0 36,350 65,874 86,633 97,599 79,875** * The Financing Needed is the amount of financing required to raise'the firm's ending cash balance to the $10,000 desired cash balance. A positive figure for Financing Needed means the firm has excess cash that can retire prior short-term borrowing or be used for investing; in this example, the excess cash in June repaid borrowing. ** This figure results in accrued interest (interest obligated for the month of June but not yet paid) of $799. Statement of Cash Flows For Six-Months Ended 6/30/20x1 $26, 254 Cash flows from operating activities (indirect method) Net Income Adjustments for differences between income flows and Cash flows from operating activities Depreciation expense Increase in accounts receivable Increase in inventory Increase in accounts payable Increase in accrued interest Increase in taxes payable Net cash from operating activities 8,830 (92,600) (15,000) 0 799 7,842 (63,875) Cash flows from investing activities Payment for equipment Net cash used for investing activities (14,000) (14,000) Cash flows from financing activities Increase in notes payable Payment of dividends Increase in long-term debt Increase in common stock Net cash from financing activities 67,875 0 0 0 67,875 Net increase in cash Plus: cash balance, 12/31/20x0 Cash balance, 6/30/20x1 (10,000) 20,000 $10,000