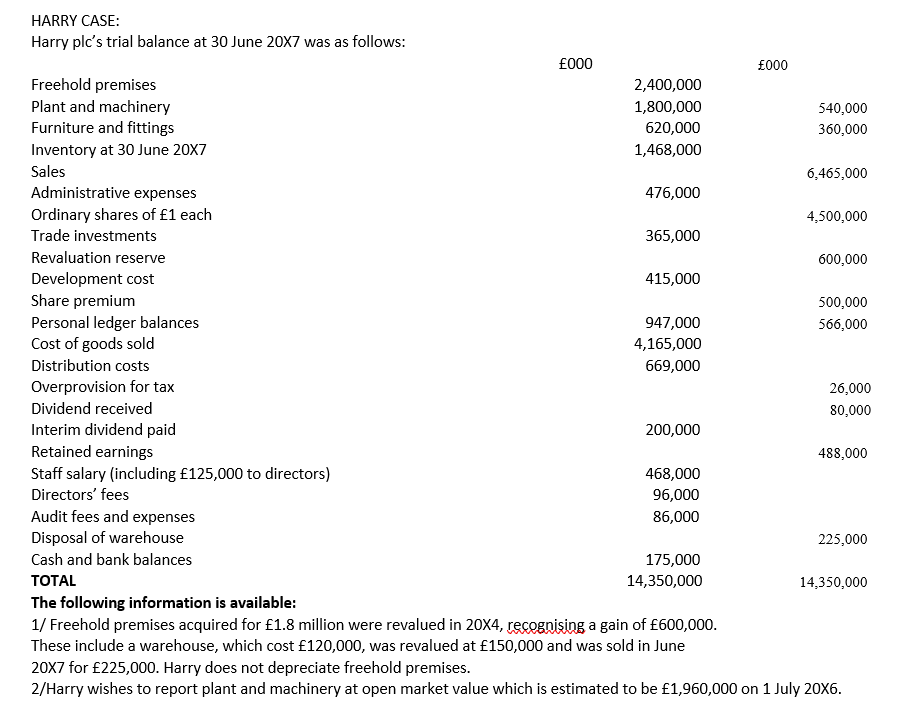

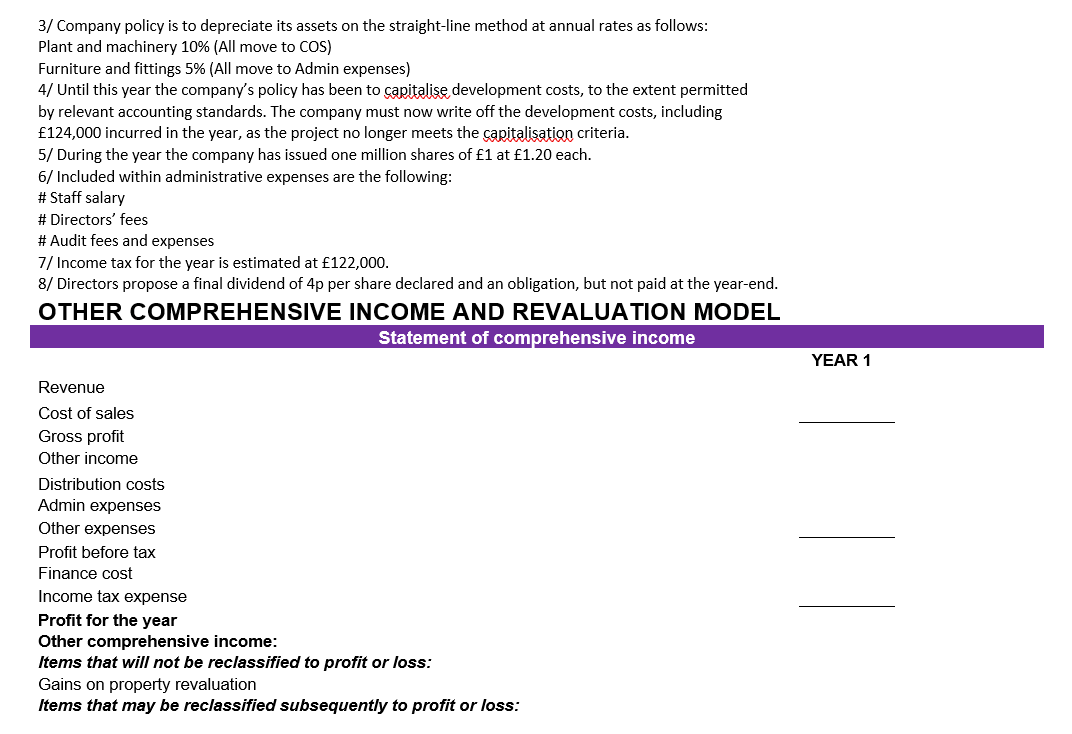

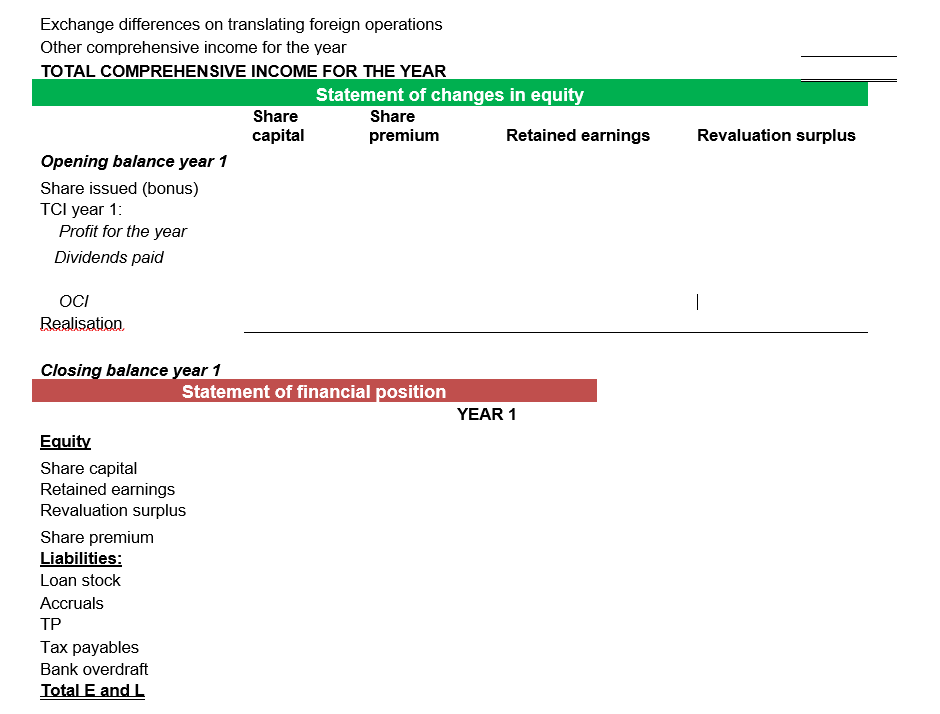

HARRY CASE: Harry ple's trial balance at 30 June 20x7 was as follows: 000 000 Freehold premises 2,400,000 Plant and machinery 1,800,000 540,000 Furniture and fittings 620,000 360,000 Inventory at 30 June 20X7 1,468,000 Sales 6,465,000 Administrative expenses 476,000 Ordinary shares of 1 each 4,500,000 Trade investments 365,000 Revaluation reserve 600,000 Development cost 415,000 Share premium 500,000 Personal ledger balances 947,000 566,000 Cost of goods sold 4,165,000 Distribution costs 669,000 Overprovision for tax 26,000 Dividend received 80,000 Interim dividend paid 200,000 Retained earnings 488,000 Staff salary (including 125,000 to directors) 468,000 Directors' fees 96,000 Audit fees and expenses 86,000 Disposal of warehouse 225,000 Cash and bank balances 175,000 TOTAL 14,350,000 14,350,000 The following information is available: 1/ Freehold premises acquired for 1.8 million were revalued in 20X4, recognising a gain of 600,000. These include a warehouse, which cost 120,000, was revalued at 150,000 and was sold in June 20x7 for 225,000. Harry does not depreciate freehold premises. 2/Harry wishes to report plant and machinery at open market value which is estimated to be 1,960,000 on 1 July 20x6. 3/ Company policy is to depreciate its assets on the straight-line method at annual rates as follows: Plant and machinery 10% (All move to COS) Furniture and fittings 5% (All move to Admin expenses) 4/ Until this year the company's policy has been to capitalise development costs, to the extent permitted by relevant accounting standards. The company must now write off the development costs, including 124,000 incurred in the year, as the project no longer meets the capitalisation criteria. 5/ During the year the company has issued one million shares of 1 at 1.20 each. 6/ Included within administrative expenses are the following: # Staff salary # Directors' fees # Audit fees and expenses 7/ Income tax for the year is estimated at 122,000. 8/ Directors propose a final dividend of 4p per share declared and an obligation, but not paid at the year-end. OTHER COMPREHENSIVE INCOME AND REVALUATION MODEL Statement of comprehensive income YEAR 1 Revenue Cost of sales Gross profit Other income Distribution costs Admin expenses Other expenses Profit before tax Finance cost Income tax expense Profit for the year Other comprehensive income: Items that will not be reclassified to profit or loss: Gains on property revaluation Items that may be reclassified subsequently to profit or loss: Exchange differences on translating foreign operations Other comprehensive income for the year TOTAL COMPREHENSIVE INCOME FOR THE YEAR Statement of changes in equity Share Share capital premium Retained earnings Opening balance year 1 Share issued (bonus) TCI year 1: Profit for the year Dividends paid Revaluation surplus 1 OCI Realisation Closing balance year 1 Statement of financial position YEAR 1 Equity Share capital Retained earnings Revaluation surplus Share premium Liabilities: Loan stock Accruals Tax payables Bank overdraft Total E and L