Having trouble with D, creating efficiency frontier and CAL. Could someone show how to integrate CAL into the eff. frontier graph? Please show steps. No risk free rate given.

Having trouble with D, creating efficiency frontier and CAL. Could someone show how to integrate CAL into the eff. frontier graph? Please show steps. No risk free rate given.

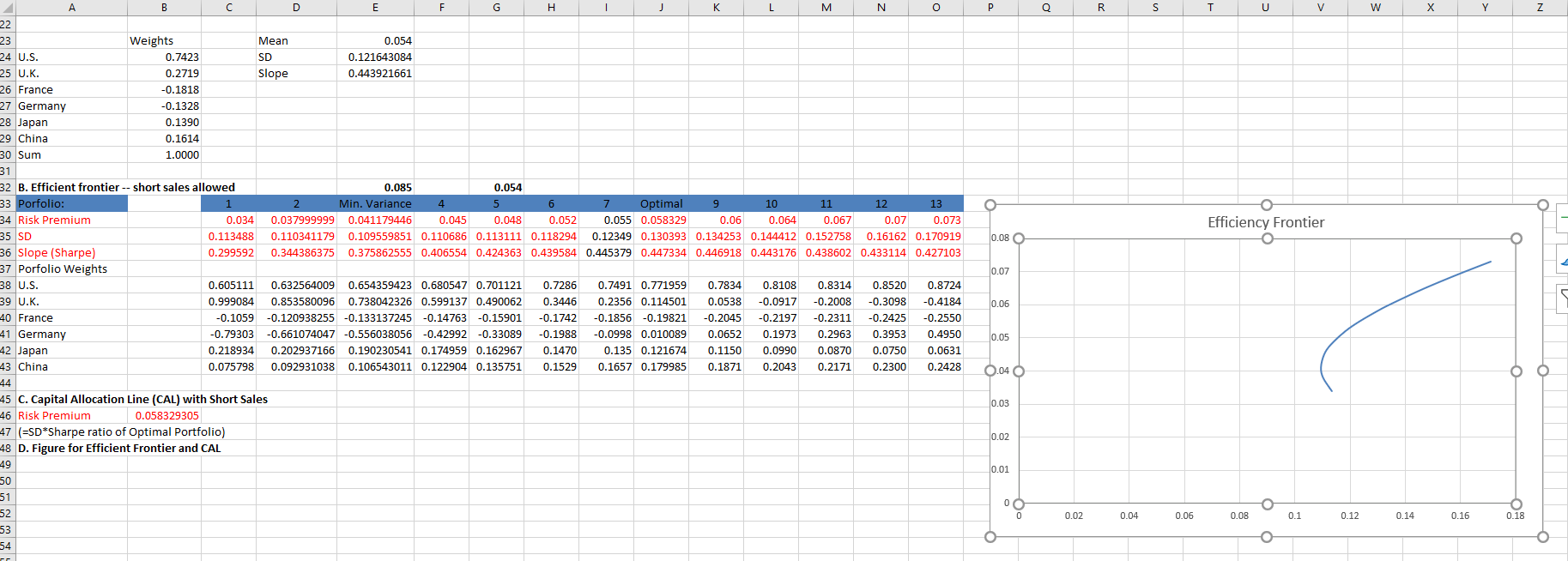

z - o R S T T U V w x Y z Efficiency Frontier 00 0.08 0.07 A B D E F G H j K L M N o 22 23 Weights Mean 0.054 24 U.S. 0.7423 SD 0.121643084 25 U.K. 0.2719 Slope 0.443921661 26 France -0.1818 27 Germany -0.1328 28 Japan 0.1390 29 China 0.1614 30 Sum 1.0000 31 32 B. Efficient frontier -- short sales allowed 0.085 0.054 33 Porfolio: 1 2 Min. Variance 4 5 6 7 Optimal 9 10 11 12 13 34 Risk Premium 0.034 0.037999999 0.041179446 0.045 0.048 0.052 0.055 0.058329 0.06 0.064 0.067 0.07 0.073 35 SD 0.113488 0.110341179 0.109559851 0.110686 0.113111 0.118294 0.12349 0.130393 0.134253 0.144412 0.152758 0.16162 0.170919 36 Slope (Sharpe) 0.299592 0.344386375 0.375862555 0.406554 0.424363 0.439584 0.445379 0.447334 0.446918 0.443176 0.438602 0.433114 0.427103 37 Porfolio Weights 38 U.S. 0.605111 0.632564009 0.654359423 0.680547 0.701121 0.7286 0.7491 0.771959 0.7834 0.8108 0.8314 0.8520 0.8724 39 U.K. 0.999084 0.853580096 0.738042326 0.599137 0.490062 0.3446 0.2356 0.114501 0.0538 -0.0917 -0.2008 -0.3098 -0.4184 40 France -0.1059 -0.120938255 -0.133137245 -0.14763 -0.15901 -0.1742 -0.1856 -0.19821 -0.2045 -0.2197 -0.2311 -0.2425 -0.2550 41 Germany -0.79303 -0.661074047 -0.556038056 -0.42992 -0.33089 -0.1988 -0.0998 0.010089 0.0652 0.1973 0.2963 0.3953 0.4950 42 Japan 0.218934 0.202937166 0.190230541 0.174959 0.162967 0.1470 0.135 0.121674 0.1150 0.0990 0.0870 0.0750 0.0631 43 China 0.075798 0.092931038 0.106543011 0.122904 0.135751 0.1529 0.1657 0.179985 0.1871 0.2043 0.2171 0.2300 0.2428 44 45 C. Capital Allocation Line (CAL) with Short Sales 46 Risk Premium 0.058329305 47 (=SD*Sharpe ratio of Optimal Portfolio) 48 D. Figure for Efficient Frontier and CAL 49 50 51 52 53 54 0.06 0.05 0.040 O 0.03 0.02 0.01 00 0 0.02 0.04 0.06 0.08 0.1 0.12 0.14 0.16 0.18 z - o R S T T U V w x Y z Efficiency Frontier 00 0.08 0.07 A B D E F G H j K L M N o 22 23 Weights Mean 0.054 24 U.S. 0.7423 SD 0.121643084 25 U.K. 0.2719 Slope 0.443921661 26 France -0.1818 27 Germany -0.1328 28 Japan 0.1390 29 China 0.1614 30 Sum 1.0000 31 32 B. Efficient frontier -- short sales allowed 0.085 0.054 33 Porfolio: 1 2 Min. Variance 4 5 6 7 Optimal 9 10 11 12 13 34 Risk Premium 0.034 0.037999999 0.041179446 0.045 0.048 0.052 0.055 0.058329 0.06 0.064 0.067 0.07 0.073 35 SD 0.113488 0.110341179 0.109559851 0.110686 0.113111 0.118294 0.12349 0.130393 0.134253 0.144412 0.152758 0.16162 0.170919 36 Slope (Sharpe) 0.299592 0.344386375 0.375862555 0.406554 0.424363 0.439584 0.445379 0.447334 0.446918 0.443176 0.438602 0.433114 0.427103 37 Porfolio Weights 38 U.S. 0.605111 0.632564009 0.654359423 0.680547 0.701121 0.7286 0.7491 0.771959 0.7834 0.8108 0.8314 0.8520 0.8724 39 U.K. 0.999084 0.853580096 0.738042326 0.599137 0.490062 0.3446 0.2356 0.114501 0.0538 -0.0917 -0.2008 -0.3098 -0.4184 40 France -0.1059 -0.120938255 -0.133137245 -0.14763 -0.15901 -0.1742 -0.1856 -0.19821 -0.2045 -0.2197 -0.2311 -0.2425 -0.2550 41 Germany -0.79303 -0.661074047 -0.556038056 -0.42992 -0.33089 -0.1988 -0.0998 0.010089 0.0652 0.1973 0.2963 0.3953 0.4950 42 Japan 0.218934 0.202937166 0.190230541 0.174959 0.162967 0.1470 0.135 0.121674 0.1150 0.0990 0.0870 0.0750 0.0631 43 China 0.075798 0.092931038 0.106543011 0.122904 0.135751 0.1529 0.1657 0.179985 0.1871 0.2043 0.2171 0.2300 0.2428 44 45 C. Capital Allocation Line (CAL) with Short Sales 46 Risk Premium 0.058329305 47 (=SD*Sharpe ratio of Optimal Portfolio) 48 D. Figure for Efficient Frontier and CAL 49 50 51 52 53 54 0.06 0.05 0.040 O 0.03 0.02 0.01 00 0 0.02 0.04 0.06 0.08 0.1 0.12 0.14 0.16 0.18