Answered step by step

Verified Expert Solution

Question

1 Approved Answer

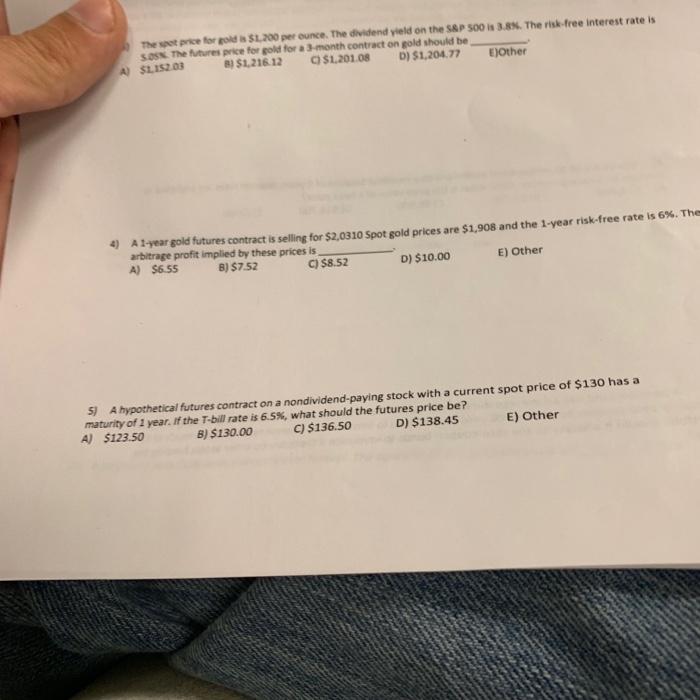

The spot price for gold is $1,200 per ounce. The dividend yield on the S&P 500 is 3.8%. The risk-free interest rate is S05%.

The spot price for gold is $1,200 per ounce. The dividend yield on the S&P 500 is 3.8%. The risk-free interest rate is S05%. The futures price for gold for a 3-month contract on gold should be, $1,201.08 D) $1,204.77 8) $1,216.12 A) $1,152.03 E)Other 4) A 1-year gold futures contract is selling for $2,0310 Spot gold prices are $1,908 and the 1-year risk-free rate is 6%. The arbitrage profit implied by these prices is A) $6.55 B) $7.52 C) $8.52 D) $10.00 E) Other S) A hypothetical futures contract on a nondividend-paying stock with a current spot price of $130 has a maturity of 1 year. If the T-bill rate is 6.5%, what should the futures price be? A) $123.50 B) $130.00 C) $136.50 D) $138.45 E) Other

Step by Step Solution

★★★★★

3.43 Rating (172 Votes )

There are 3 Steps involved in it

Step: 1

3 E Other Explanation Future price spot price 1 risk free rate time to maturity Future price 1200 15...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Accounting IFRS

Authors: Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield

3rd edition

1119372933, 978-1119372936