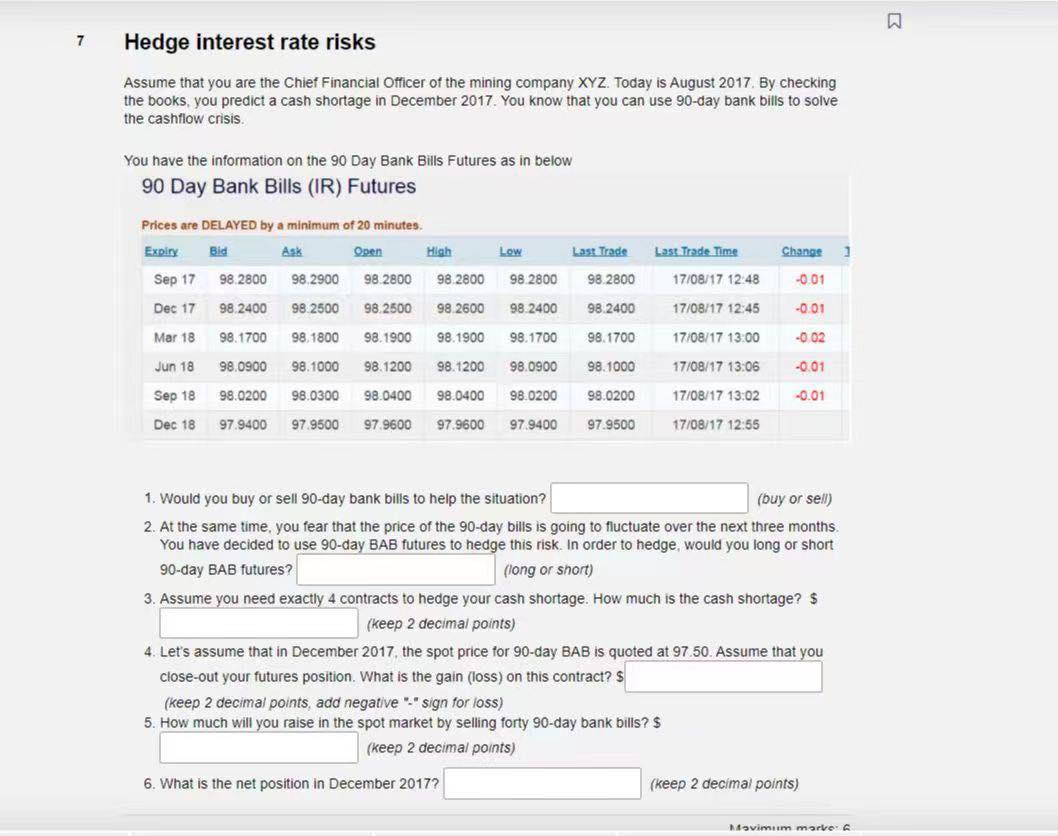

Hedge interest rate risks Assume that you are the Chief Financial Officer of the mining company XYZ. Today is August 2017. By checking the books, you predict a cash shortage in December 2017 . You know that you can use 90 -day bank bills to solve the cashflow crisis. You have the information on the 90 Day Bank Bills Futures as in below 90 Day Bank Bills (IR) Futures Prices are DELAYED by a minimum of 20 minutes. 1. Would you buy or sell 90 -day bank bills to help the situation? (buy or sell) 2. At the same time, you fear that the price of the 90 -day bills is going to fluctuate over the next three months. You have decided to use 90 -day BAB futures to hedge this risk. In order to hedge, would you long or short 90-day BAB futures? (long or short) 3. Assume you need exactly 4 contracts to hedge your cash shortage. How much is the cash shortage? $ (keep 2 decimal points) 4. Let's assume that in December 2017, the spot price for 90-day BAB is quoted at 97.50. Assume that you close-out your futures position. What is the gain (loss) on this contract? $ (keep 2 decimal points, add negative "-" sign for loss) 5. How much will you raise in the spot market by selling forty 90 -day bank bills? $ (keep 2 decimal points) 6. What is the net position in December 2017 ? (keep 2 decimal points) Hedge interest rate risks Assume that you are the Chief Financial Officer of the mining company XYZ. Today is August 2017. By checking the books, you predict a cash shortage in December 2017 . You know that you can use 90 -day bank bills to solve the cashflow crisis. You have the information on the 90 Day Bank Bills Futures as in below 90 Day Bank Bills (IR) Futures Prices are DELAYED by a minimum of 20 minutes. 1. Would you buy or sell 90 -day bank bills to help the situation? (buy or sell) 2. At the same time, you fear that the price of the 90 -day bills is going to fluctuate over the next three months. You have decided to use 90 -day BAB futures to hedge this risk. In order to hedge, would you long or short 90-day BAB futures? (long or short) 3. Assume you need exactly 4 contracts to hedge your cash shortage. How much is the cash shortage? $ (keep 2 decimal points) 4. Let's assume that in December 2017, the spot price for 90-day BAB is quoted at 97.50. Assume that you close-out your futures position. What is the gain (loss) on this contract? $ (keep 2 decimal points, add negative "-" sign for loss) 5. How much will you raise in the spot market by selling forty 90 -day bank bills? $ (keep 2 decimal points) 6. What is the net position in December 2017 ? (keep 2 decimal points)