Hello, can you help me please in solving this questions ?

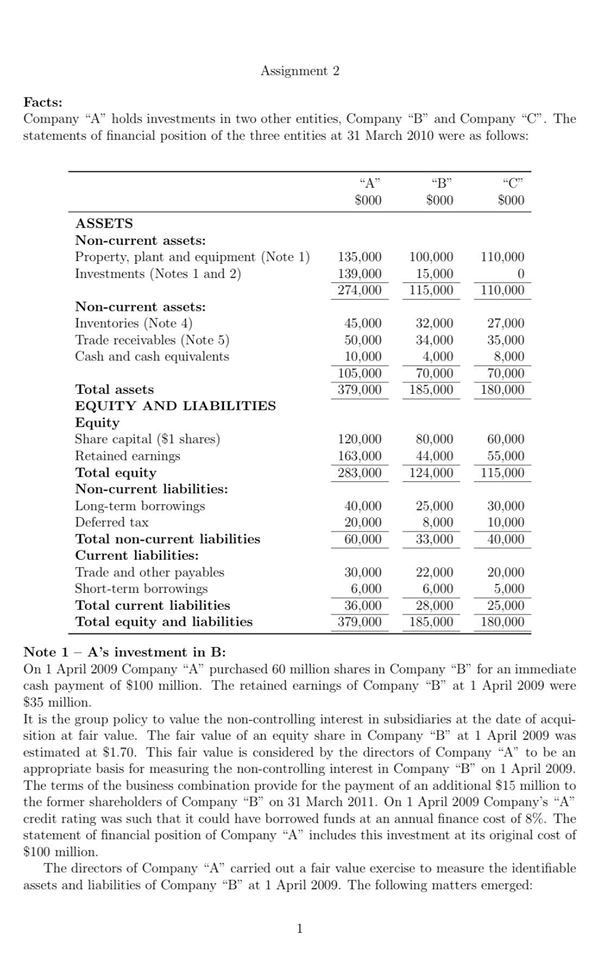

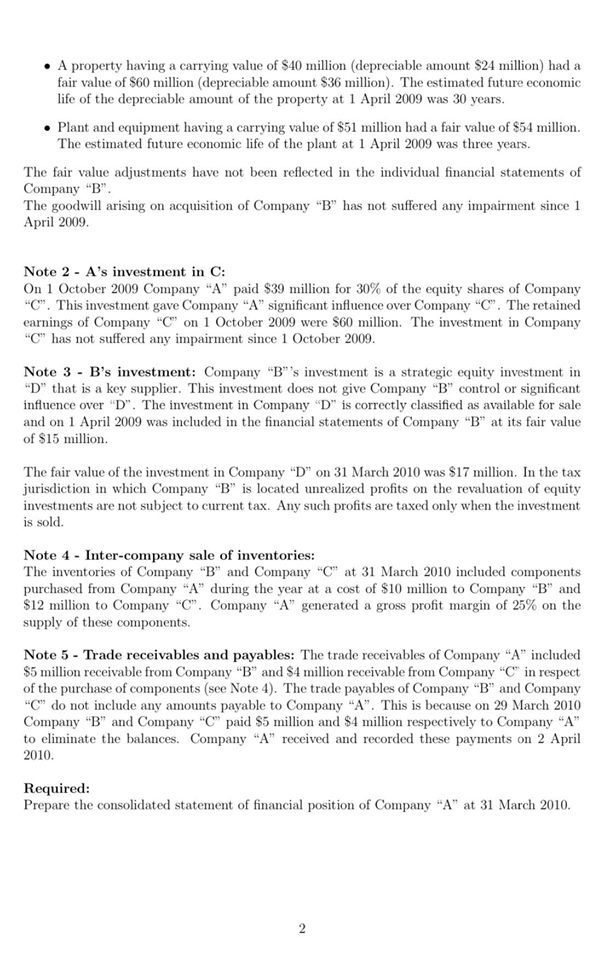

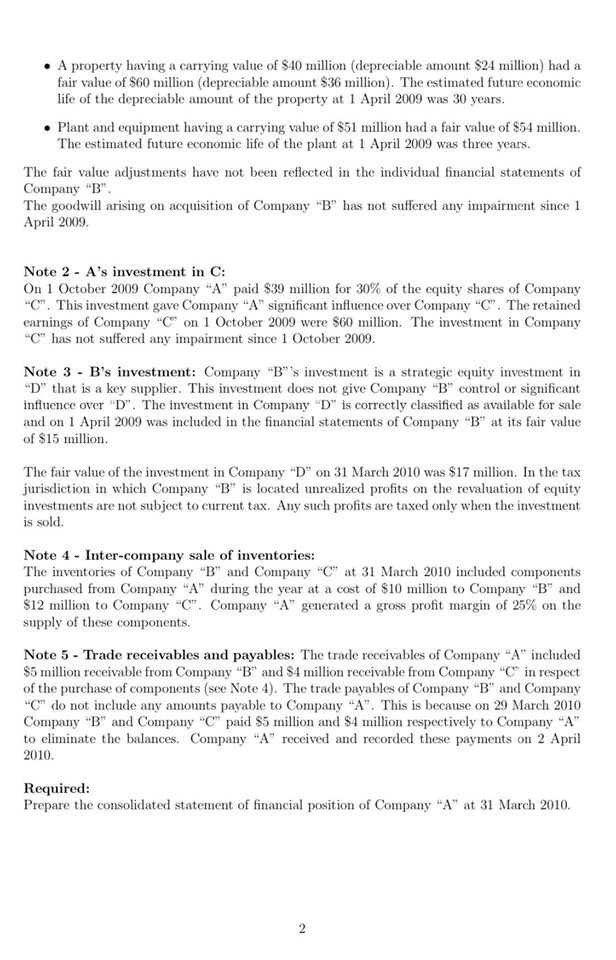

Assignment 2 Facts: Company "A" holds investments in two other entities, Company "B" and Company "C". The statements of financial position of the three entities at 31 March 2010 were as follows: "A" "B' $000 $000 $000 ASSETS Non-current assets: Property, plant and equipment (Note 1) 135,000 100,000 110,000 Investments (Notes 1 and 2) 139,000 15,000 274,000 115,000 110,000 Non-current assets: Inventories (Note 4) 45,000 32,000 27,000 Trade receivables (Note 5) 50,000 34,000 35,000 Cash and cash equivalents 10,000 4,000 8.000 105,000 70,000 70,000 Total assets 379,000 185,000 180.000 EQUITY AND LIABILITIES Equity Share capital ($1 shares) 120,000 80,000 60,000 Retained earnings 163,000 44,000 55,000 Total equity 283,000 124,000 115,000 Non-current liabilities: Long-term borrowings 40,000 25,000 30.000 Deferred tax 20.000 8,000 10.000 Total non-current liabilities 60.000 33,000 10,000 Current liabilities: Trade and other payables 30,000 22,000 20,000 Short-term borrowings 6.000 6,000 5.000 Total current liabilities 36,000 28,000 25,000 Total equity and liabilities 379,000 185,000 180,000 Note 1 - A's investment in B: On 1 April 2009 Company "A" purchased 60 million shares in Company "B" for an immediate cash payment of $100 million. The retained earnings of Company "B" at 1 April 2009 were $35 million. It is the group policy to value the non-controlling interest in subsidiaries at the date of acqui- sition at fair value. The fair value of an equity share in Company "B" at 1 April 2009 was estimated at $1.70. This fair value is considered by the directors of Company "A" to be an appropriate basis for measuring the non-controlling interest in Company "B" on 1 April 2009. The terms of the business combination provide for the payment of an additional $15 million to the former shareholders of Company "B" on 31 March 2011. On 1 April 2009 Company's "A" credit rating was such that it could have borrowed funds at an annual finance cost of 8%. The statement of financial position of Company "A" includes this investment at its original cost of $100 million. The directors of Company "A" carried out a fair value exercise to measure the identifiable assets and liabilities of Company "B" at 1 April 2009. The following matters emerged:. A property having a carrying value of $40 million (depreciable amount $24 million) had a fair value of $60 million (depreciable amount $36 million). The estimated future economic life of the depreciable amount of the property at 1 April 2009 was 30 years. . Plant and equipment having a carrying value of $51 million had a fair value of $54 million. The estimated future economic life of the plant at 1 April 2009 was three years. The fair value adjustments have not been reflected in the individual financial statements of Company "B". The goodwill arising on acquisition of Company "B" has not suffered any impairment since 1 April 2009. Note 2 - A's investment in C: On 1 October 2009 Company "A" paid $39 million for 30% of the equity shares of Company "C". This investment gave Company "A" significant influence over Company "C". The retained earnings of Company "C" on 1 October 2009 were $60 million. The investment in Company "C" has not suffered any impairment since 1 October 2009. Note 3 - B's investment: Company "B"'s investment is a strategic equity investment in "D" that is a key supplier. This investment does not give Company "B" control or significant influence over "D". The investment in Company "D" is correctly classified as available for sale and on 1 April 2009 was included in the financial statements of Company "B" at its fair value of $15 million. The fair value of the investment in Company "D" on 31 March 2010 was $17 million. In the tax jurisdiction in which Company "B" is located unrealized profits on the revaluation of equity investments are not subject to current tax. Any such profits are taxed only when the investment is sold. Note 4 - Inter-company sale of inventories: The inventories of Company "B" and Company "C" at 31 March 2010 included components purchased from Company "A" during the year at a cost of $10 million to Company "B" and $12 million to Company "C". Company "A" generated a gross profit margin of 25% on the supply of these components. Note 5 - Trade receivables and payables: The trade receivables of Company "A" included $5 million receivable from Company "B" and $4 million receivable from Company "C" in respect of the purchase of components (see Note 4). The trade payables of Company "B" and Company "C" do not include any amounts payable to Company "A". This is because on 29 March 2010 Company "B" and Company "C" paid $5 million and $4 million respectively to Company "A" to eliminate the balances. Company "A" received and recorded these payments on 2 April 2010. Required: Prepare the consolidated statement of financial position of Company "A" at 31 March 2010