Question: Hello :D From the Information provided above, the below document is showing my Tax Form schedule C. I was having trouble calculating the figure that

Hello :D

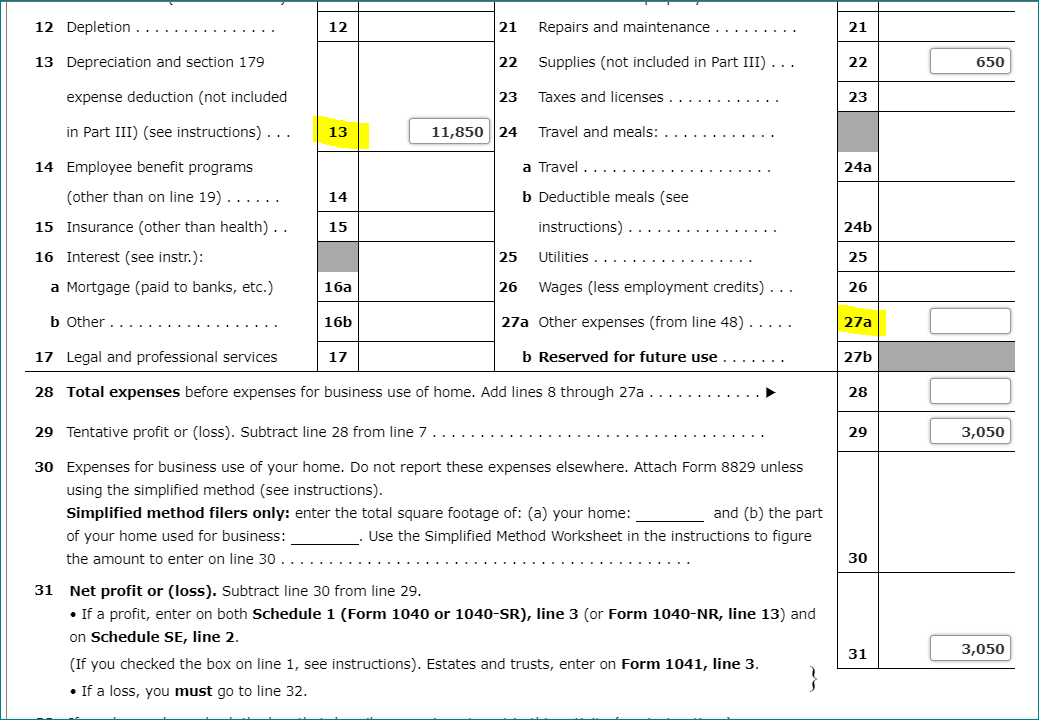

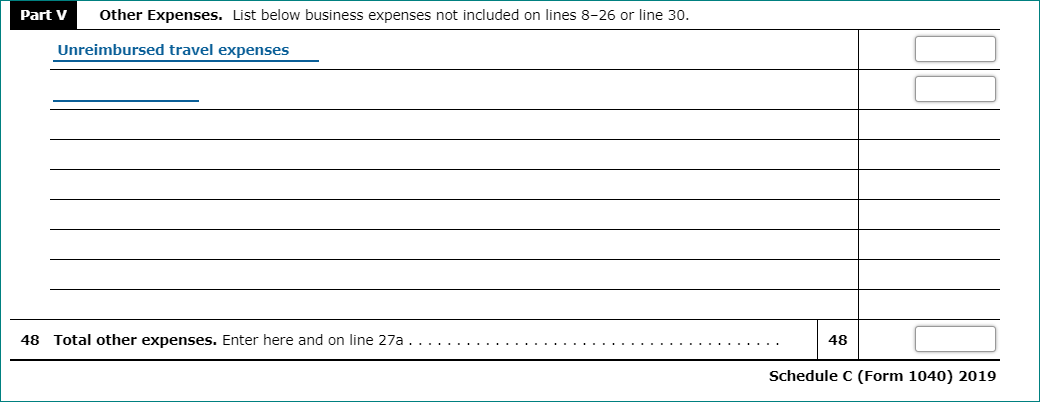

From the Information provided above, the below document is showing my Tax Form schedule C. I was having trouble calculating the figure that was highlighted and wanted to make sure that the $11,850 was the correct check figure that is suppose to go there. For question 27a, I am having trouble trying to figure what the other expenses are and kept getting confused. May I have some assistance with that part, please:)

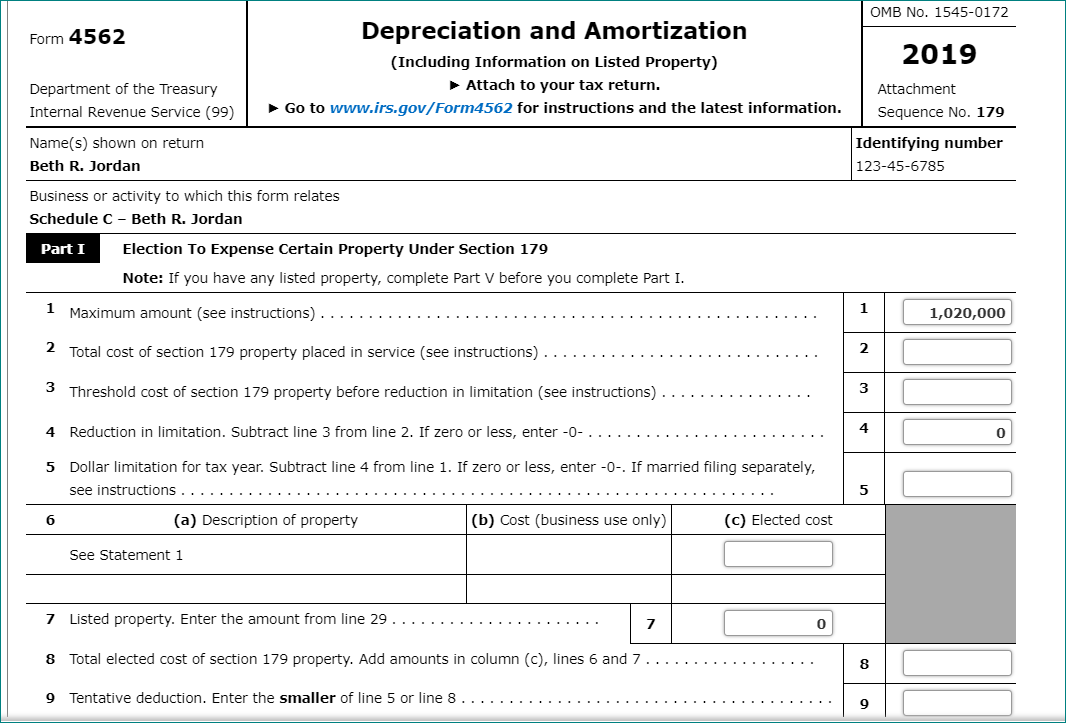

For this tax For 4562, I need help as well filling in the blanks! D: I got stuck on trying to decifer if the computer, printer and furniture were included in line 2 and 3 but was not sure. If I may have some clarification on this part as well, please :)

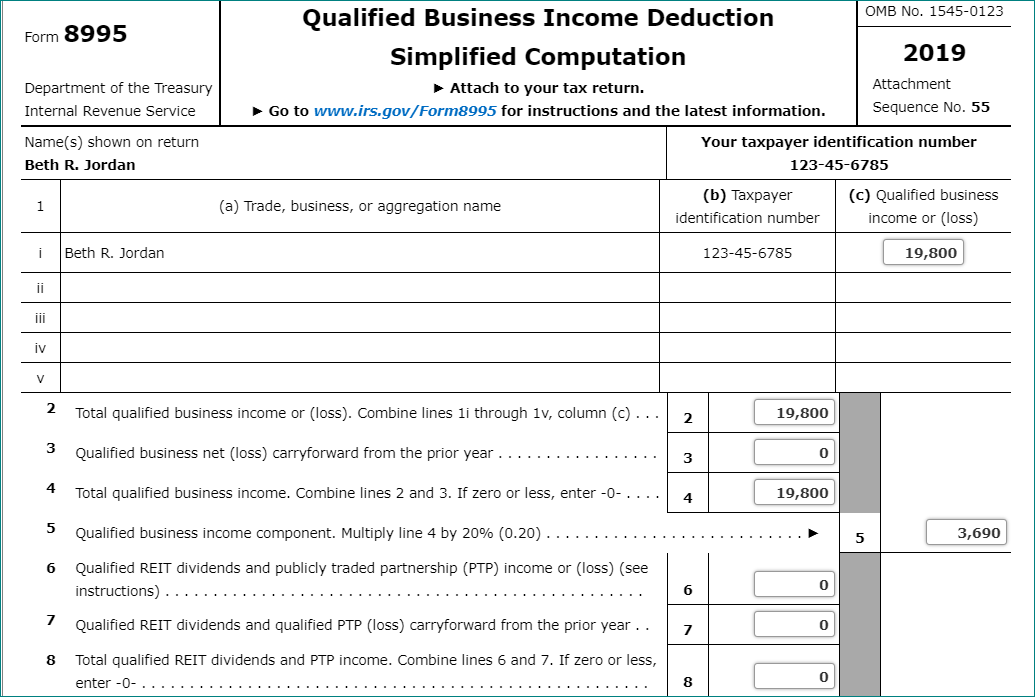

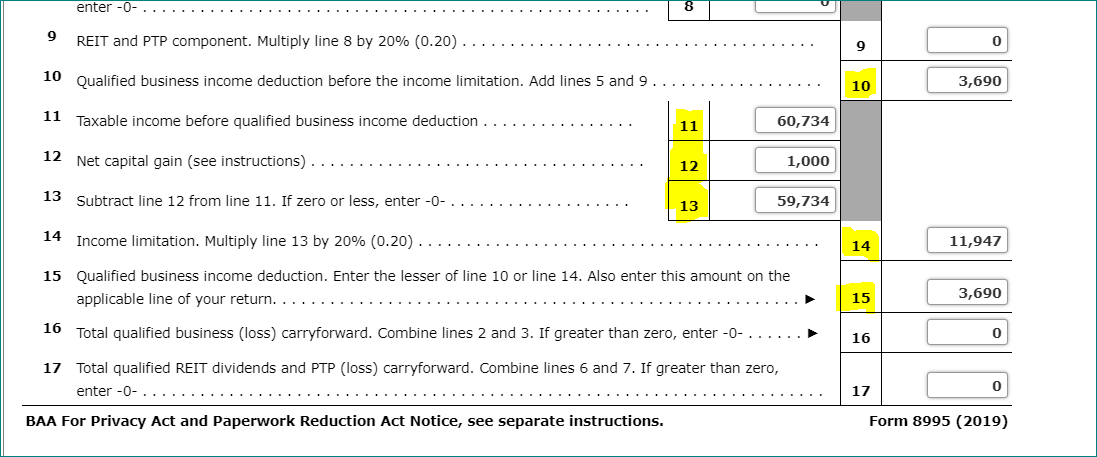

I do apologize for this question is very long but lastly is the form 8995. With this form, I just need help verifying if the check figures I got were correct and if they were if I can get assistance with those as well if you don't mind :D This would be the last problem I am having trouble with. Please do leave detailed explanations if you can so I may understand where you are coming from with your answers!

I will definitely give a thumbs up and a great review! The help is much appreciated :) Thank you so much!

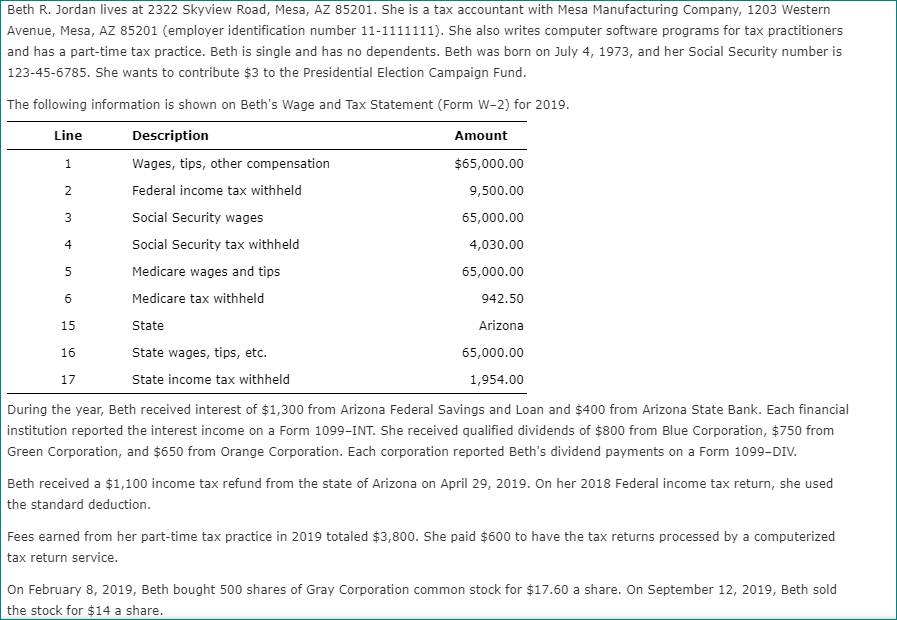

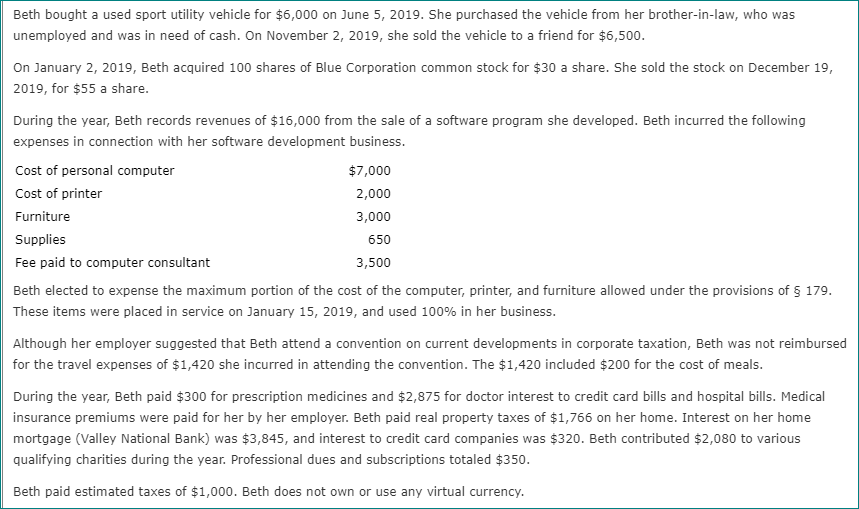

1 2 4 5 Beth R. Jordan lives at 2322 Skyview Road, Mesa, AZ 85201. She is a tax accountant with Mesa Manufacturing Company, 1203 Western Avenue, Mesa, AZ 85201 employer identification number 11-1111111). She also writes computer software programs for tax practitioners and has a part-time tax practice. Beth is single and has no dependents. Beth was born on July 4, 1973, and her Social Security number is 123-45-6785. She wants to contribute $3 to the Presidential Election Campaign Fund. The following information is shown on Beth's Wage and Tax Statement (Form W-2) for 2019. Line Description Amount Wages, tips, other compensation $65,000.00 Federal income tax withheld 9,500.00 3 Social Security wages 65,000.00 Social Security tax withheld 4,030.00 Medicare wages and tips 65,000.00 Medicare tax withheld 942.50 State Arizona State wages, tips, etc. 65,000.00 17 State income tax withheld 1,954.00 During the year, Beth received interest of $1,300 from Arizona Federal Savings and Loan and $400 from Arizona State Bank. Each financial institution reported the interest income on a Form 1099-INT. She received qualified dividends of $800 from Blue Corporation, $750 from Green Corporation, and $650 from Orange Corporation. Each corporation reported Beth's dividend payments on a Form 1099-DIV. Beth received a $1,100 income tax refund from the state of Arizona on April 29, 2019. On her 2018 Federal income tax return, she used the standard deduction. Fees earned from her part-time tax practice in 2019 totaled $3,800. She paid $600 to have the tax returns processed by a computerized tax return service. 6 15 16 On February 8, 2019, Beth bought 500 shares of Gray Corporation common stock for $17.60 a share. On September 12, 2019, Beth sold the stock for $14 a share. Beth bought a used sport utility vehicle for $6,000 on June 5, 2019. She purchased the vehicle from her brother-in-law, who was unemployed and was in need of cash. On November 2, 2019, she sold the vehicle to a friend for $6,500. On January 2, 2019, Beth acquired 100 shares of Blue Corporation common stock for $30 a share. She sold the stock on December 19, 2019, for $55 a share. During the year, Beth records revenues of $16,000 from the sale of a software program she developed. Beth incurred the following expenses in connection with her software development business. Cost of personal computer $7,000 Cost of printer 2,000 Furniture 3,000 Supplies 650 Fee paid to computer consultant 3,500 Beth elected to expense the maximum portion of the cost of the computer, printer, and furniture allowed under the provisions of $ 179. These items were placed in service on January 15, 2019, and used 100% in her business. Although her employer suggested that Beth attend a convention on current developments in corporate taxation, Beth was not reimbursed for the travel expenses of $1,420 she incurred in attending the convention. The $1,420 included $200 for the cost of meals. During the year, Beth paid $300 for prescription medicines and $2,875 for doctor interest to credit card bills and hospital bills. Medical insurance premiums were paid for her by her employer. Beth paid real property taxes of $1,766 on her home. Interest on her home mortgage (Valley National Bank) was $3,845, and interest to credit card companies was $320. Beth contributed $2,080 to various qualifying charities during the year. Professional dues and subscriptions totaled $350. Beth paid estimated taxes of $1,000. Beth does not own or use any virtual currency. 12 Depletion ... 12 21 Repairs and maintenance ..... 21 13 Depreciation and section 179 22 Supplies (not included in Part III) .. 22 650 expense deduction (not included 23 Taxes and licenses 23 in Part III) (see instructions) ... 13 11,850 24 Travel and meals: a Travel 24a 14 b Deductible meals (see 14 Employee benefit programs (other than on line 19)...... 15 Insurance (other than health).. 16 Interest (see instr.): a Mortgage (paid to banks, etc.) 15 instructions) 24b 25 Utilities 25 16a 26 Wages (less employment credits) ... 26 b Other.. 16b 27a Other expenses (from line 48) 27a 17 Legal and professional services 17 b Reserved for future use 27b 28 Total expenses before expenses for business use of home. Add lines 8 through 27a. 28 29 Tentative profit or loss). Subtract line 28 from line 7 29 3,050 30 Expenses for business use of your home. Do not report these expenses elsewhere. Attach Form 8829 unless using the simplified method (see instructions). Simplified method filers only: enter the total square footage of: (a) your home: and (b) the part of your home used for business: Use the Simplified Method Worksheet in the instructions to figure the amount to enter on line 30 30 31 Net profit or loss). Subtract line 30 from line 29. If a profit, enter on both Schedule 1 (Form 1040 or 1040-SR), line 3 (or Form 1040-NR, line 13) and on Schedule SE, line 2. (If you checked the box on line 1, see instructions). Estates and trusts, enter on Form 1041, line 3. If a loss, you must go to line 32 31 3,050 Part V Other Expenses. List below business expenses not included on lines 8-26 or line 30. Unreimbursed travel expenses 48 Total other expenses. Enter here and on line 27a 48 Schedule C (Form 1040) 2019 OMB No. 1545-0172 Form 4562 2019 Depreciation and Amortization (Including Information on Listed Property) Attach to your tax return. Go to www.irs.gov/Form4562 for instructions and the latest information. Department of the Treasury Internal Revenue Service (99) Attachment Sequence No. 179 Name(s) shown on return Beth R. Jordan Identifying number 123-45-6785 Business or activity to which this form relates Schedule C - Beth R. Jordan Part I Election To Expense Certain Property Under Section 179 Note: If you have any listed property, complete Part V before you complete Part I. 1 Maximum amount (see instructions) 1 1,020,000 2 Total cost of section 179 property placed in service (see instructions) 2 3 Threshold cost of section 179 property before reduction in limitation (see instructions) 3 4 Reduction in limitation. Subtract line 3 from line 2. If zero or less, enter -0- 4 5 Dollar limitation for tax year. Subtract line 4 from line 1. If zero or less, enter -O-. If married filing separately, see instructions 5 6 (a) Description of property (b) Cost (business use only) (C) Elected cost See Statement 1 7 Listed property. Enter the amount from line 29 7 0 8 Total elected cost of section 179 property. Add amounts in column (C), lines 6 and 7 8 9 Tentative deduction. Enter the smaller of line 5 or line 8 9 10 Carryover of disallowed deduction from line 13 of your 2018 Form 4562. 10 0 11 Business income limitation. Enter the smaller of business income (not less than zero) or line 5. See instrs. 11 12 Section 179 expense deduction. Add lines 9 and 10, but don't enter more than line 11 12 13 Carryover of disallowed deduction to 2020. Add lines 9 and 10, less line 12.. > 13 0 Note: Don't use Part II or Part III below for listed property. Instead, use Part V. OMB No. 1545-0123 Form 8995 Qualified Business Income Deduction Simplified Computation Attach to your tax return. Go to www.irs.gov/Form8995 for instructions and the latest information. 2019 Department of the Treasury Internal Revenue Service Attachment Sequence No. 55 Name(s) shown on return Beth R. Jordan Your taxpayer identification number 123-45-6785 1 (a) Trade, business, or aggregation name (b) Taxpayer identification number (c) Qualified business income or loss) i Beth R. Jordan 123-45-6785 19,800 ii jii iv V 2 Total qualified business income or loss). Combine lines li through 1v, column (C)... 2 19,800 3 Qualified business net (loss) carryforward from the prior year 3 0 4 Total qualified business income. Combine lines 2 and 3. If zero or less, enter-O-. 19,800 4 5 Qualified business income component. Multiply line 4 by 20% (0.20). 5 3,690 6 Qualified REIT dividends and publicly traded partnership (PTP) income or (loss) (see instructions) 6 0 7 0 7 8 Qualified REIT dividends and qualified PTP (loss) carryforward from the prior year .. Total qualified REIT dividends and PTP income. Combine lines 6 and 7. If zero or less, enter -0- 8 0 enter -0- 9 REIT and PTP component. Multiply line 8 by 20% (0.20).. 9 0 10 Qualified business income deduction before the income limitation. Add lines 5 and 9 10 3,690 11 Taxable income before qualified business income deduction 11 60,734 12 Net capital gain (see instructions). 12 1,000 13 Subtract line 12 from line 11. If zero or less, enter-O- 13 59,734 14 Income limitation. Multiply line 13 by 20% (0.20). 14 11,947 15 Qualified business income deduction. Enter the lesser of line 10 or line 14. Also enter this amount on the applicable line of your return... 15 3,690 16 Total qualified business (loss) carryforward. Combine lines 2 and 3. If greater than zero, enter-O- 0 16 17 Total qualified REIT dividends and PTP (loss) carryforward. Combine lines 6 and 7. If greater than zero, enter -0- 17 0 BAA For Privacy Act and Paperwork Reduction Act Notice, see separate instructions. Form 8995 (2019) 1 2 4 5 Beth R. Jordan lives at 2322 Skyview Road, Mesa, AZ 85201. She is a tax accountant with Mesa Manufacturing Company, 1203 Western Avenue, Mesa, AZ 85201 employer identification number 11-1111111). She also writes computer software programs for tax practitioners and has a part-time tax practice. Beth is single and has no dependents. Beth was born on July 4, 1973, and her Social Security number is 123-45-6785. She wants to contribute $3 to the Presidential Election Campaign Fund. The following information is shown on Beth's Wage and Tax Statement (Form W-2) for 2019. Line Description Amount Wages, tips, other compensation $65,000.00 Federal income tax withheld 9,500.00 3 Social Security wages 65,000.00 Social Security tax withheld 4,030.00 Medicare wages and tips 65,000.00 Medicare tax withheld 942.50 State Arizona State wages, tips, etc. 65,000.00 17 State income tax withheld 1,954.00 During the year, Beth received interest of $1,300 from Arizona Federal Savings and Loan and $400 from Arizona State Bank. Each financial institution reported the interest income on a Form 1099-INT. She received qualified dividends of $800 from Blue Corporation, $750 from Green Corporation, and $650 from Orange Corporation. Each corporation reported Beth's dividend payments on a Form 1099-DIV. Beth received a $1,100 income tax refund from the state of Arizona on April 29, 2019. On her 2018 Federal income tax return, she used the standard deduction. Fees earned from her part-time tax practice in 2019 totaled $3,800. She paid $600 to have the tax returns processed by a computerized tax return service. 6 15 16 On February 8, 2019, Beth bought 500 shares of Gray Corporation common stock for $17.60 a share. On September 12, 2019, Beth sold the stock for $14 a share. Beth bought a used sport utility vehicle for $6,000 on June 5, 2019. She purchased the vehicle from her brother-in-law, who was unemployed and was in need of cash. On November 2, 2019, she sold the vehicle to a friend for $6,500. On January 2, 2019, Beth acquired 100 shares of Blue Corporation common stock for $30 a share. She sold the stock on December 19, 2019, for $55 a share. During the year, Beth records revenues of $16,000 from the sale of a software program she developed. Beth incurred the following expenses in connection with her software development business. Cost of personal computer $7,000 Cost of printer 2,000 Furniture 3,000 Supplies 650 Fee paid to computer consultant 3,500 Beth elected to expense the maximum portion of the cost of the computer, printer, and furniture allowed under the provisions of $ 179. These items were placed in service on January 15, 2019, and used 100% in her business. Although her employer suggested that Beth attend a convention on current developments in corporate taxation, Beth was not reimbursed for the travel expenses of $1,420 she incurred in attending the convention. The $1,420 included $200 for the cost of meals. During the year, Beth paid $300 for prescription medicines and $2,875 for doctor interest to credit card bills and hospital bills. Medical insurance premiums were paid for her by her employer. Beth paid real property taxes of $1,766 on her home. Interest on her home mortgage (Valley National Bank) was $3,845, and interest to credit card companies was $320. Beth contributed $2,080 to various qualifying charities during the year. Professional dues and subscriptions totaled $350. Beth paid estimated taxes of $1,000. Beth does not own or use any virtual currency. 12 Depletion ... 12 21 Repairs and maintenance ..... 21 13 Depreciation and section 179 22 Supplies (not included in Part III) .. 22 650 expense deduction (not included 23 Taxes and licenses 23 in Part III) (see instructions) ... 13 11,850 24 Travel and meals: a Travel 24a 14 b Deductible meals (see 14 Employee benefit programs (other than on line 19)...... 15 Insurance (other than health).. 16 Interest (see instr.): a Mortgage (paid to banks, etc.) 15 instructions) 24b 25 Utilities 25 16a 26 Wages (less employment credits) ... 26 b Other.. 16b 27a Other expenses (from line 48) 27a 17 Legal and professional services 17 b Reserved for future use 27b 28 Total expenses before expenses for business use of home. Add lines 8 through 27a. 28 29 Tentative profit or loss). Subtract line 28 from line 7 29 3,050 30 Expenses for business use of your home. Do not report these expenses elsewhere. Attach Form 8829 unless using the simplified method (see instructions). Simplified method filers only: enter the total square footage of: (a) your home: and (b) the part of your home used for business: Use the Simplified Method Worksheet in the instructions to figure the amount to enter on line 30 30 31 Net profit or loss). Subtract line 30 from line 29. If a profit, enter on both Schedule 1 (Form 1040 or 1040-SR), line 3 (or Form 1040-NR, line 13) and on Schedule SE, line 2. (If you checked the box on line 1, see instructions). Estates and trusts, enter on Form 1041, line 3. If a loss, you must go to line 32 31 3,050 Part V Other Expenses. List below business expenses not included on lines 8-26 or line 30. Unreimbursed travel expenses 48 Total other expenses. Enter here and on line 27a 48 Schedule C (Form 1040) 2019 OMB No. 1545-0172 Form 4562 2019 Depreciation and Amortization (Including Information on Listed Property) Attach to your tax return. Go to www.irs.gov/Form4562 for instructions and the latest information. Department of the Treasury Internal Revenue Service (99) Attachment Sequence No. 179 Name(s) shown on return Beth R. Jordan Identifying number 123-45-6785 Business or activity to which this form relates Schedule C - Beth R. Jordan Part I Election To Expense Certain Property Under Section 179 Note: If you have any listed property, complete Part V before you complete Part I. 1 Maximum amount (see instructions) 1 1,020,000 2 Total cost of section 179 property placed in service (see instructions) 2 3 Threshold cost of section 179 property before reduction in limitation (see instructions) 3 4 Reduction in limitation. Subtract line 3 from line 2. If zero or less, enter -0- 4 5 Dollar limitation for tax year. Subtract line 4 from line 1. If zero or less, enter -O-. If married filing separately, see instructions 5 6 (a) Description of property (b) Cost (business use only) (C) Elected cost See Statement 1 7 Listed property. Enter the amount from line 29 7 0 8 Total elected cost of section 179 property. Add amounts in column (C), lines 6 and 7 8 9 Tentative deduction. Enter the smaller of line 5 or line 8 9 10 Carryover of disallowed deduction from line 13 of your 2018 Form 4562. 10 0 11 Business income limitation. Enter the smaller of business income (not less than zero) or line 5. See instrs. 11 12 Section 179 expense deduction. Add lines 9 and 10, but don't enter more than line 11 12 13 Carryover of disallowed deduction to 2020. Add lines 9 and 10, less line 12.. > 13 0 Note: Don't use Part II or Part III below for listed property. Instead, use Part V. OMB No. 1545-0123 Form 8995 Qualified Business Income Deduction Simplified Computation Attach to your tax return. Go to www.irs.gov/Form8995 for instructions and the latest information. 2019 Department of the Treasury Internal Revenue Service Attachment Sequence No. 55 Name(s) shown on return Beth R. Jordan Your taxpayer identification number 123-45-6785 1 (a) Trade, business, or aggregation name (b) Taxpayer identification number (c) Qualified business income or loss) i Beth R. Jordan 123-45-6785 19,800 ii jii iv V 2 Total qualified business income or loss). Combine lines li through 1v, column (C)... 2 19,800 3 Qualified business net (loss) carryforward from the prior year 3 0 4 Total qualified business income. Combine lines 2 and 3. If zero or less, enter-O-. 19,800 4 5 Qualified business income component. Multiply line 4 by 20% (0.20). 5 3,690 6 Qualified REIT dividends and publicly traded partnership (PTP) income or (loss) (see instructions) 6 0 7 0 7 8 Qualified REIT dividends and qualified PTP (loss) carryforward from the prior year .. Total qualified REIT dividends and PTP income. Combine lines 6 and 7. If zero or less, enter -0- 8 0 enter -0- 9 REIT and PTP component. Multiply line 8 by 20% (0.20).. 9 0 10 Qualified business income deduction before the income limitation. Add lines 5 and 9 10 3,690 11 Taxable income before qualified business income deduction 11 60,734 12 Net capital gain (see instructions). 12 1,000 13 Subtract line 12 from line 11. If zero or less, enter-O- 13 59,734 14 Income limitation. Multiply line 13 by 20% (0.20). 14 11,947 15 Qualified business income deduction. Enter the lesser of line 10 or line 14. Also enter this amount on the applicable line of your return... 15 3,690 16 Total qualified business (loss) carryforward. Combine lines 2 and 3. If greater than zero, enter-O- 0 16 17 Total qualified REIT dividends and PTP (loss) carryforward. Combine lines 6 and 7. If greater than zero, enter -0- 17 0 BAA For Privacy Act and Paperwork Reduction Act Notice, see separate instructions. Form 8995 (2019)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts