Question

Hello- I had tried this problem and was able to complete part A, the standard deviation. However I could not get the correct answer for

Hello- I had tried this problem and was able to complete part A, the standard deviation. However I could not get the correct answer for part B. At the bottom of this question, I've attached the work I did (which is partially wrong). Please help with part B. I will upvote immediately! B) What is the proportion invested in the money market fund and each of the two risky funds? (Round your answers to 2 decimal places.)

B) What is the proportion invested in the money market fund and each of the two risky funds? (Round your answers to 2 decimal places.)

| Proportion Invested | ||

| Money market fund | 39.51. (WRONG) | % |

| Stocks | 21.68 (WRONG) | % |

| Bonds | 38.81 (WRONG) | % |

The Work I did (partially incorrect)

Return required from risky assets,

12% = wR + 4% - 4%w

=> 8%/w + 4% = R

The weights in risky portfolio when sharpe ratio is highest is

Stock s = 0.358473

Stock b = 0.641527

Rp = 0.358473*23% + 0.641527*14% =17.226%

Sp = 15.9443%

=> 8%/w + 4% = R

=> 8%/w + 4% = 17.226%

=> w = 8%/13.226% = 60.49%

Standard Deviation = Wp*Sp = 60.49%*15.9443% = 9.64%

Money Market Fund = 1- 60.49% = 39.51%

Stocks = 60.49%*0.358473 = 21.68%

Bonds = 60.49%*0.641527 = 38.81%

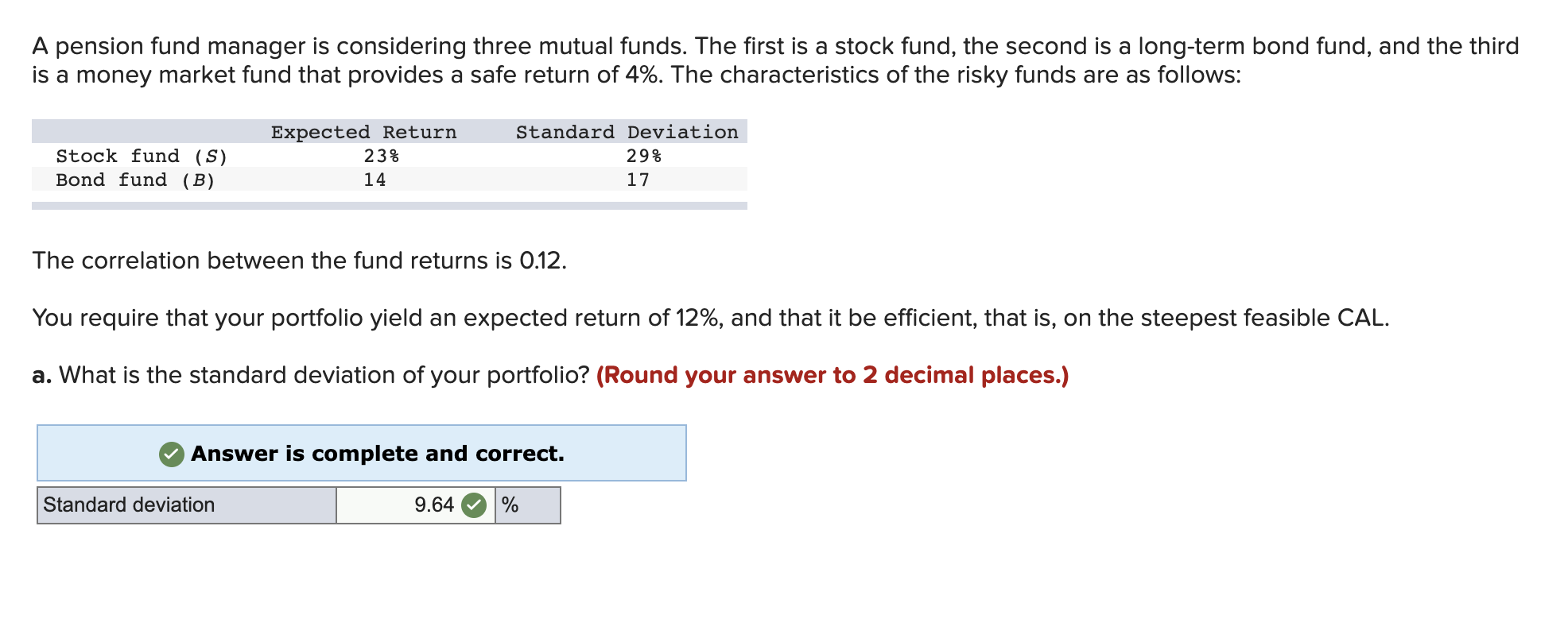

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term bond fund, and the third is a money market fund that provides a safe return of 4%. The characteristics of the risky funds are as follows: Stock fund (S) Bond fund (B) Expected Return 23% 14 Standard Deviation 29% 17 The correlation between the fund returns is 0.12. You require that your portfolio yield an expected return of 12%, and that it be efficient, that is, on the steepest feasible CAL. a. What is the standard deviation of your portfolio? (Round your answer to 2 decimal places.) Answer is complete and correct. Standard deviation 9.64 %Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Economics Of Money Banking And Financial Markets

Authors: Frederic S. Mishkin

7th Edition

0321122356, 978-0321122353