Answered step by step

Verified Expert Solution

Question

1 Approved Answer

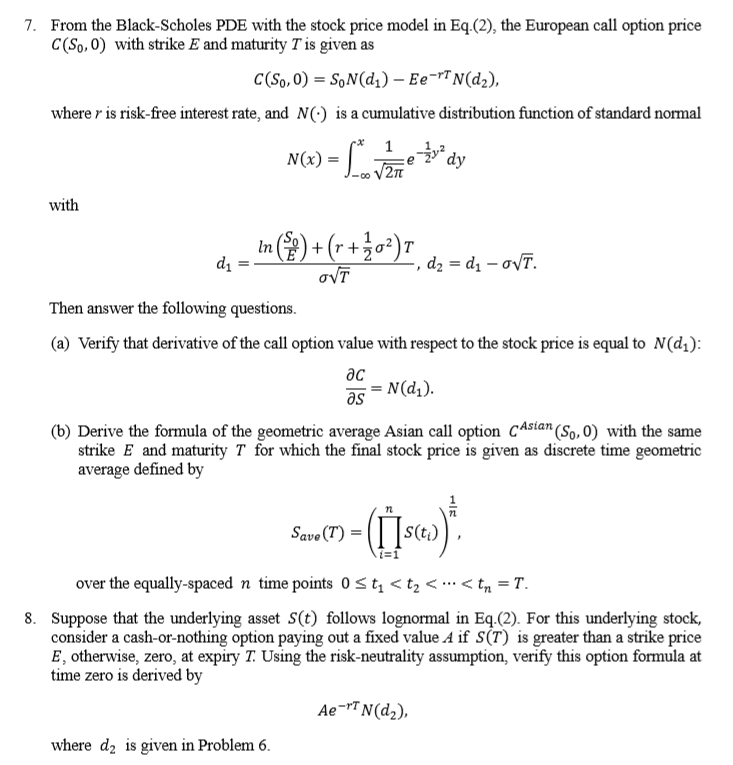

Hello. I want to solve this. I need your help 7. From the Black-Scholes PDE with the stock price model in Eq.(2), the European call

Hello. I want to solve this. I need your help

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Functional Analysis And The Feynman Operator Calculus

Authors: Tepper L Gill, Woodford W Zachary, Zachary Woodford

1st Edition

331927595X, 9783319275956