Answered step by step

Verified Expert Solution

Question

1 Approved Answer

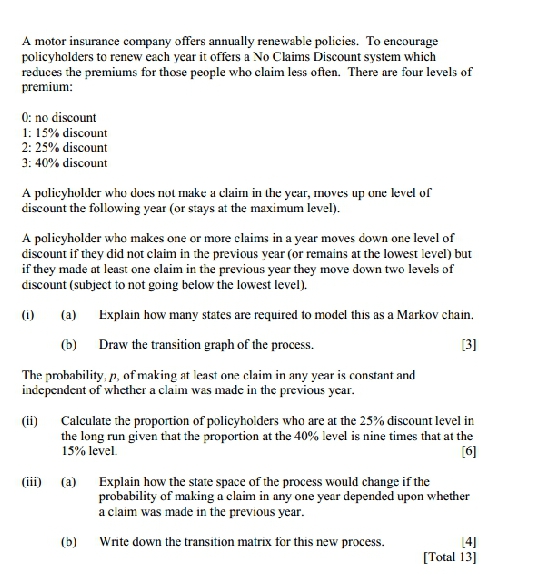

hello,, please assist me tackle these questions A motor insurance company offers annually renewable policies. To encourage policyholders to renew each year it offers a

hello,, please assist me tackle these questions

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finite Mathematics

Authors: Stefan Waner, Steven Costenoble

7th Edition

133751554X, 9781337515542