Answered step by step

Verified Expert Solution

Question

1 Approved Answer

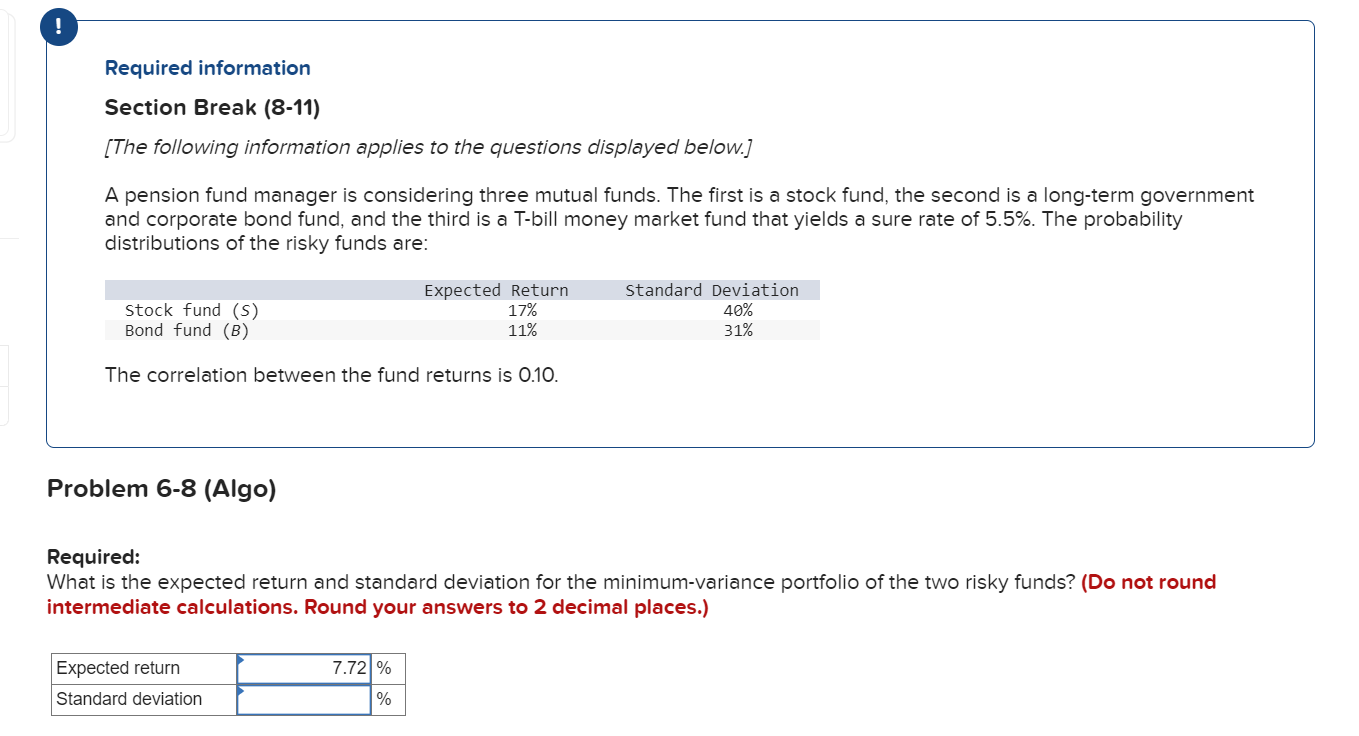

Hello, Please show step by step solution. Thank you. (excel solution is highly appreciated) Required information Section Break (8-11) [The following information applies to the

Hello, Please show step by step solution. Thank you. (excel solution is highly appreciated)

Hello, Please show step by step solution. Thank you. (excel solution is highly appreciated)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding Housing Finance

Authors: Peter King

2nd Edition

0415432952, 978-0415432955