Answered step by step

Verified Expert Solution

Question

1 Approved Answer

hello yourgreat answer no.3.5 would be very touched. waiting for your positive response thank you 1 Standard Deviation CFA6) You find a particular st0CK deviation

hello

yourgreat answer no.3.5 would be very touched.

waiting for your positive response

thank you

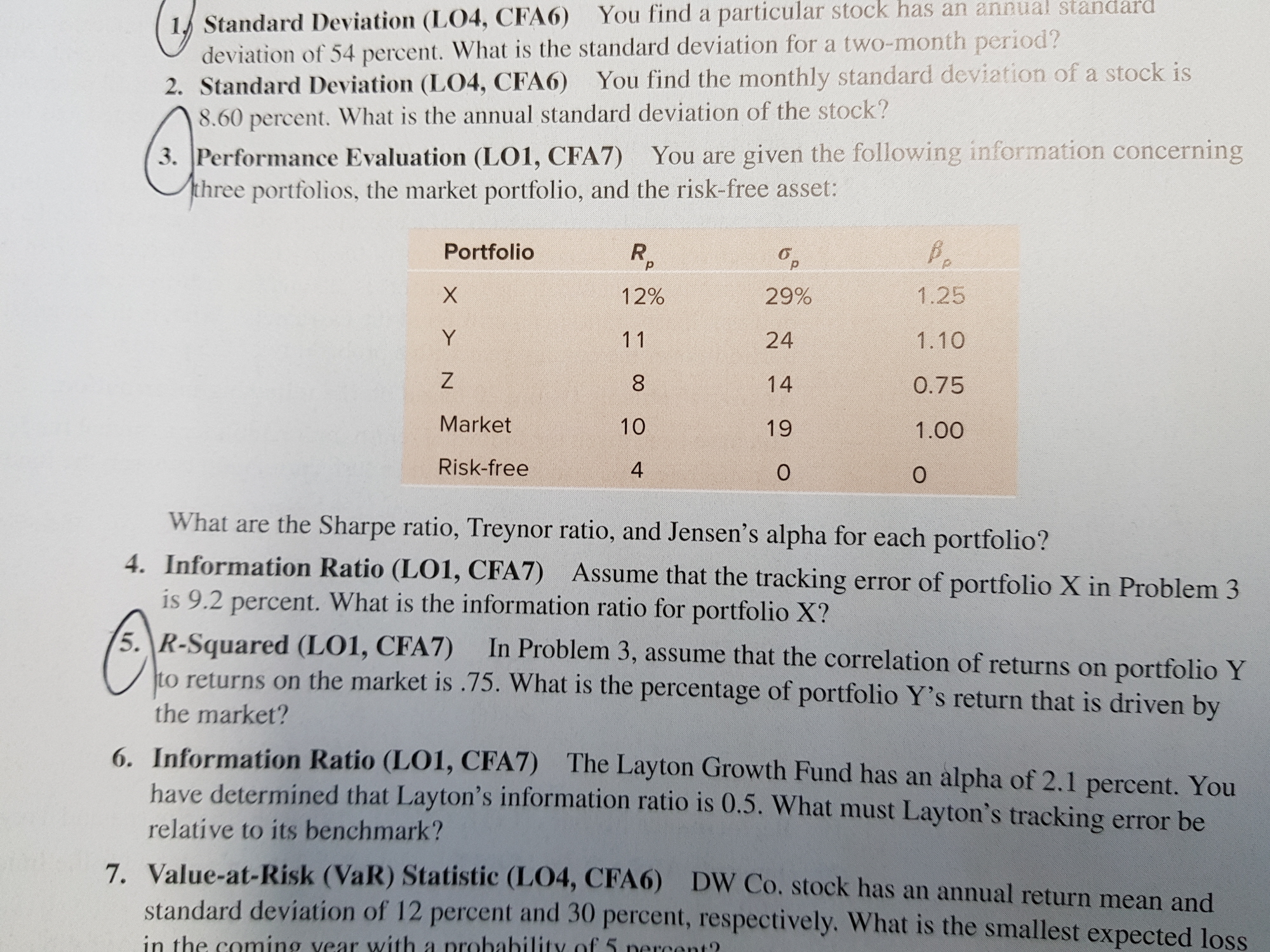

1 Standard Deviation CFA6) You find a particular st0CK deviation of 54 percent. What is the standard deviation for a two-month poriocl? 2. Standard (L04, CFA6) You find thc monthly standard of a stock is 8.60 percent. What is the annual standard deviation of the stock? 3. Performance Evaluation (LOI, CFA7) You are given the following in!Orrnation concerning hree portfolios, the market portfolio, and the risk-free asset: Portfolio x z Market Risk-free p 12% 11 8 10 4 p 29% 14 19 1.25 1.10 0.75 1.00 What are the Sharpe ratio, Treynor ratio, and Jensen's alpha for each portfolio? 4. Information Ratio (1001, CFA7) Assume that the tracking error of portfolio X in Problem 3 is 9.2 percent. What is the information ratio for portfolio X? 5. R-Squared (LOI, CFA7) In Problem 3, assume that the correlation of returns on portfolio Y o returns on the market is .75. What is the percentage of portfolio Y's return that is driven by the market? 6. Information Ratio (LOI, CFA7) The Layton Growth Fund has an lpha of 2.1 percent. You have determined that Layton's information ratio is 0.5. What must Layton's tracking error be relative to its benchmark? 7. Value-at-Risk (VaR) Statistic (L04, CFA6) DW Co. stock has an annual return mean and standard deviation of 12 percent and 30 percent, respectively. What is the smallest expected loss

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduction To Finance Markets, Investments, And Financial Management

Authors: Ronald W. Melicher, Edgar A. Norton

17th Edition

1119561175, 978-1119561170