Question: .Helo kind ly help Question 1 (20 points) Consider the standard Mortensen-Pissarides model in continuous time. Labor force is normalized to 1. Unemployed workers with

.Helo kind ly help

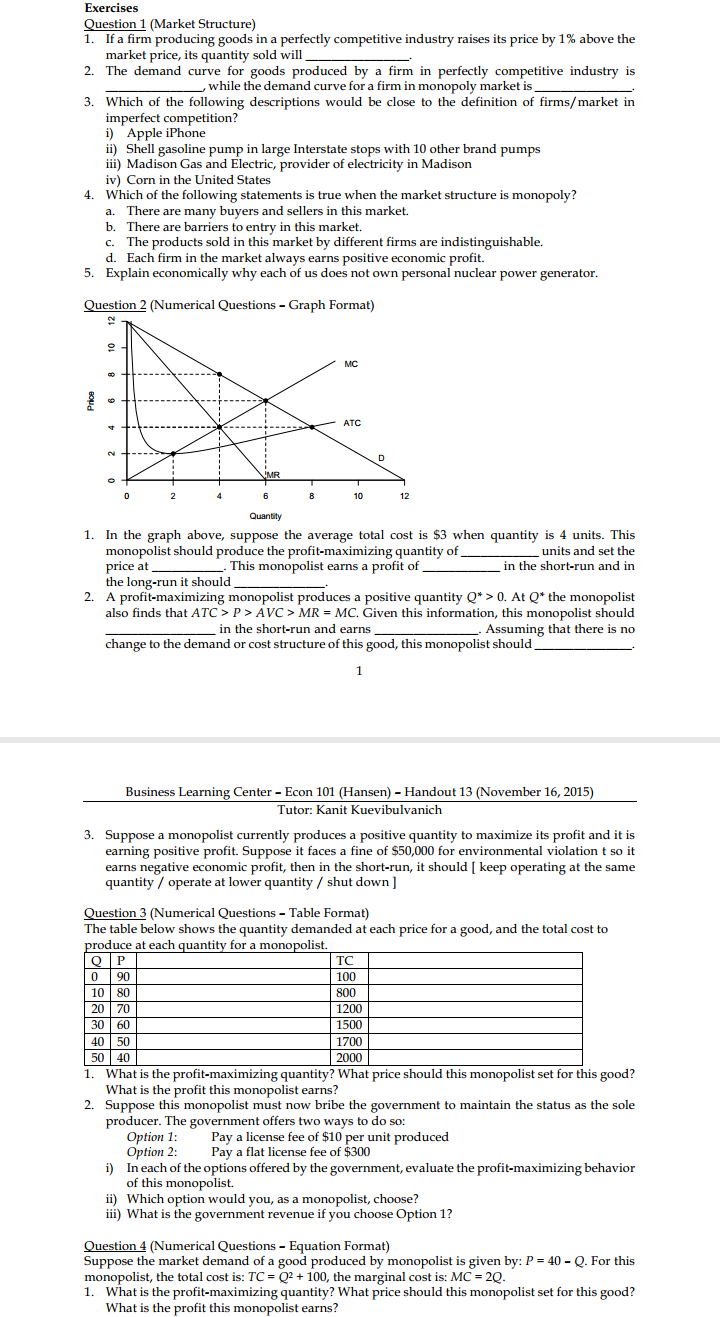

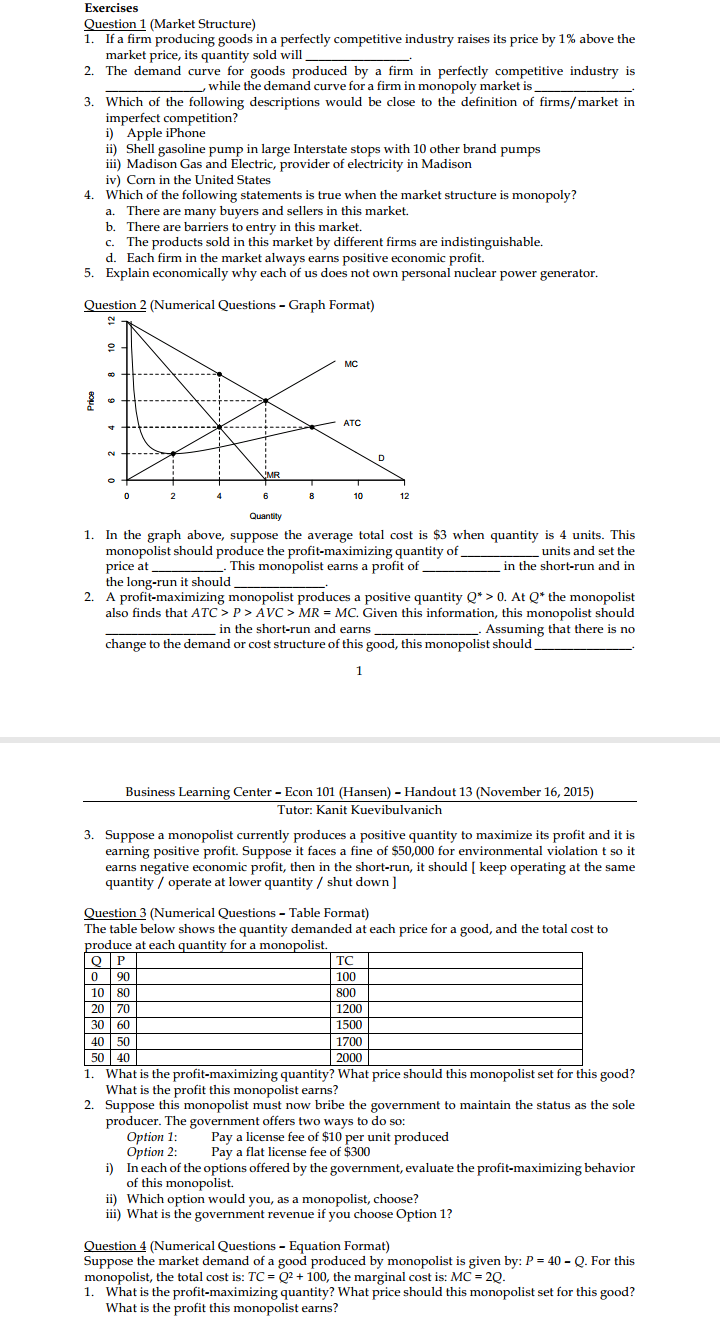

Question 1 (20 points) Consider the standard Mortensen-Pissarides model in continuous time. Labor force is normalized to 1. Unemployed workers with measure u search for jobs, and firms with measure v search for unemployed workers. The matching technology is given by the function m(u, v), which is increasing in both arguments and exhibits constant returns to scale. It is convenient to define the market tightness 0 = v/u. A large measure of firms decide whether to enter the labor market with exactly one vacancy. When a firm meets an unemployed worker a job is formed. The output of a job is p per unit of time. However, while the vacancy is unfilled, firms have to pay a search or recruiting cost equal to pc per unit of time. Upon a successful match, the worker's wage is negotiated through Nash bargaining. Let / represent the worker's bargaining power. The destruction rate of existing jobs is exogenous and given by the Poison rate A. Once a shock arrives, the firm closes the job down. Subsequently, the worker goes back to the pool of unemployment, and the firm exits the labor market. So far this is just the model we described in class. What is new here is that unemployed workers are not (necessarily) eligible for unemployment benefits for the whole duration of their unemployment spell. More precisely, a worker who just lost her job starts receiving a benefit z per unit of time right away, but she will stop being eligible for this benefit at a Poisson rate 6. Thus, at any point in time, there are two types of unemployed workers: those who are still eligible for z, and those whose unemployment benefit eligibility has expired. This, of course, will be important for the negotiation process between a firm and an uncinployed worker. Throughout this question focus on steady state equilibria and let the discount rate of agents be given by r. Also, assume that o 2 A, which will simplify some of the derivations later on. a) Draw a figure that describes the flows in and out of the various states a worker may be in. Denote these states by E, for employed, U, for unemployed with benefits, and Un, for unemployed without benefits. b) Let u denote the equilibrium measure of all unemployed workers, and un the measure of unemployed workers who do not receive benefits. Equating the inflows and outflows for the states E and Un (defined in part a), derive the analogue of the Beveridge curve for this economy. That is, find two equations that describe the equilibrium variables u, un as functions of the market tightness e. In what follows let w denote the wage of a worker who got a job while still cligible for unemployment benefits, and let w, denote the wage of a worker who was not eligible for unemployment benefits when she negotiated with the firm. It should be obvious why: even though the two types of unemployed workers have the exact same bargaining power (8), they do not have the same outside option. 2 c) Describe the value functions for a worker in the various states. d) Describe the value functions for a firm in the various states. e) Exploiting the free entry of firms into the labor market, describe the Job Creation (JC) condition for this economy." f) Solve the bargaining problem between a firm and an unemployed worker in state U and Un and derive the analogue of the Wage Curve (WC) for this economy. g) Using your findings in part (f) show that, for any given d, we have w > wn What is the economic meaning of this result? h) Without going into detail, provide a strategy to solve for the steady state equi- librium. More precisely, explain how you would combine the various equilibrium con- ditions derived so far in order to characterize the five equilibrium variables.Exercises lguestion lfMarket Structure} 4. 5. If a rm producing goods' on a perfectly competitive industry raises its price by 1'11: above the market price, ils quantity sold will The demand curve for goods produced by a firm in perfectly competitive industry is while the demand curve for a rm' in monopoly market' is Which of the following descriptions would be close to the denition of firms/market in imperfect competition? i] Apple iPhone ii) Shel] gasoline pump in large Interstate stops with 1|] other brand pumps iii) Madison Gas and Electric. provider of electricity in Madison iv} Corn in the United States Which of the following statements is true when the market structure is monopoly? a. There are many buyers and sellers in this market b. There are barriers to entry in this market. c. The products sold in this market by different firms are indistinguishable. d. Each firrrl in the market always earns positive economic prot. Explain economically why each of us does not own persona] nuclear power generator. Question 2 {Numerical Questions - Graph Format) N In the graph above, suppose the average total cost is '53 when quantity is 4 units. This monopolist should produce the profit-maximizing quantity of units and set the price at .This monopolist earns a profit of in the short-run and in the long-run it should A profit-maximizing monopolist produces a positive quantity Q' 2* (I. At Q*the monopolist also nds that ATC > P > AVC > MR= MC Given this information, this monopolist should in the short-run and earns . Assuming that there is no change to the demand or cost structure ofthis good, this monopolist should 1 Business Learning Center - Econ 1|]1 (Hansen) - Handout 13 (November 16, 2015} Tutor: Kanit Kuevibulvanich Suppose a monopolist currently produces a positive quantity to maximize its prot and it is earning positive profit. Suppose it faces a fine of $50,010 for environmental violationt so it earns negative economic profit, then in the short-run, it should [ keep operating at the same quantity / operate at lower quantity / shut down ] Question 3 {Numerical Questions Table Format) The table below shows thequantity demanded at each price for a good, and the total cost to produce at each quantity for a monopolist. 1. 2. What is the prot-mindzing quantity? What price should this monopolist set for this good? What is the profit this monopolist earns? Suppose this monopolist must now bribe the government to maintain the status as the sole producer. The government offers two ways to do so: Option 1: Pay a license fee of $10 per unit produced Option 2: Pay a at license fee of 53:10 i] In each of the options offered by the government, evaluate the profit-maximizing behavior of this monopolist ii) Which option would you, as a monopolist, choose? iii) What is the government revenue if you choose Option 1? Question 4 {Numerical Questions - Equation Format} Suppose the market demand of a good produced by monopolist is given by: P = 4U - C]. For this monopolist, the total cost is: TC = Q2 1- 100, the marginal cost is: MC = 2Q. 1. What is the profit-maximizing quantity? What price should this monopolist set for this good? What is the profit this monopolist earns? Exercises Question 1 (Monopoly and Market Efficiency) Suppose the demand for a particular good is given by P = 120 - Q. This good is produced by a monopolist who has the cost function of TC = 0.502 + 30Q + 100, and the marginal cost is given by MC = Q + 30. This monopolist cannot discriminate prices each consumer pays. 1. What would be the profit-maximizing behavior of this monopolist? What is its profit? 2. What are the price and quantity if this good were to be produced in a perfectly competitive setting? Compare the changes in consumer surpluses, producer surpluses, and, if any, deadweight losses in each case. Draw the graphs to illustrate these facts. 3. If this monopolist did not study Econ101 before starting his business and he decides to maximize the revenue instead. (This is usually seen in real life by managers who maximize sales instead of profits.) What would be the price and quantity if he does so? Compare the profits to the case where this monopolist maximizes his profits. Question 2 (Price Discrimination - Conceptual Question) Identify which kind of price discrimination is practiced in each of the following scenarios. i) Student price for Wisconsin Men's Basketball tickets ii) Plastic molding company poisons material and labels "Not Suitable for Food Handling" iii) Priceline "Name Your Price" lets you choose the price you want for hotels and flights iv) Airlines and hotels charging different prices when buying at different time before travel Question 3 (First-Degree Price Discrimination) Suppose a hotel can perfectly identify how much each consumer is willing to pay and it knows that the demand curve is P = 100 - Q. The operating cost per room is constant at AC = MC = 20. 1. What is (are) the price(s) the hotel will charge to consumers? How many rooms would be sold? What is its profits? 2. What is the consumer surplus? What is the producer surplus? What is the deadweight loss? 3. Compare the results to the scenario where the hotel cannot price-discriminate and must charge a single price. Question 4 (Third-Degree Price Discrimination) Northeast Airlines has the same operating cost per passenger in First Class and Economy Class at MC = AC = 20. The demand by First Class passengers is P = 100 - 20, while the demand by Economy Class passengers is P = 50 - 0.5Q. 1. Suppose the airlines can price-discriminate, how many seats will the airlines sell? At what price(s)? What is its profits? 2. Suppose the airlines is unable to price-discriminate, how many seats will the airlines sell? At what price(s)? What is its profits

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts