Help, Don't give answers without showing all the calculations

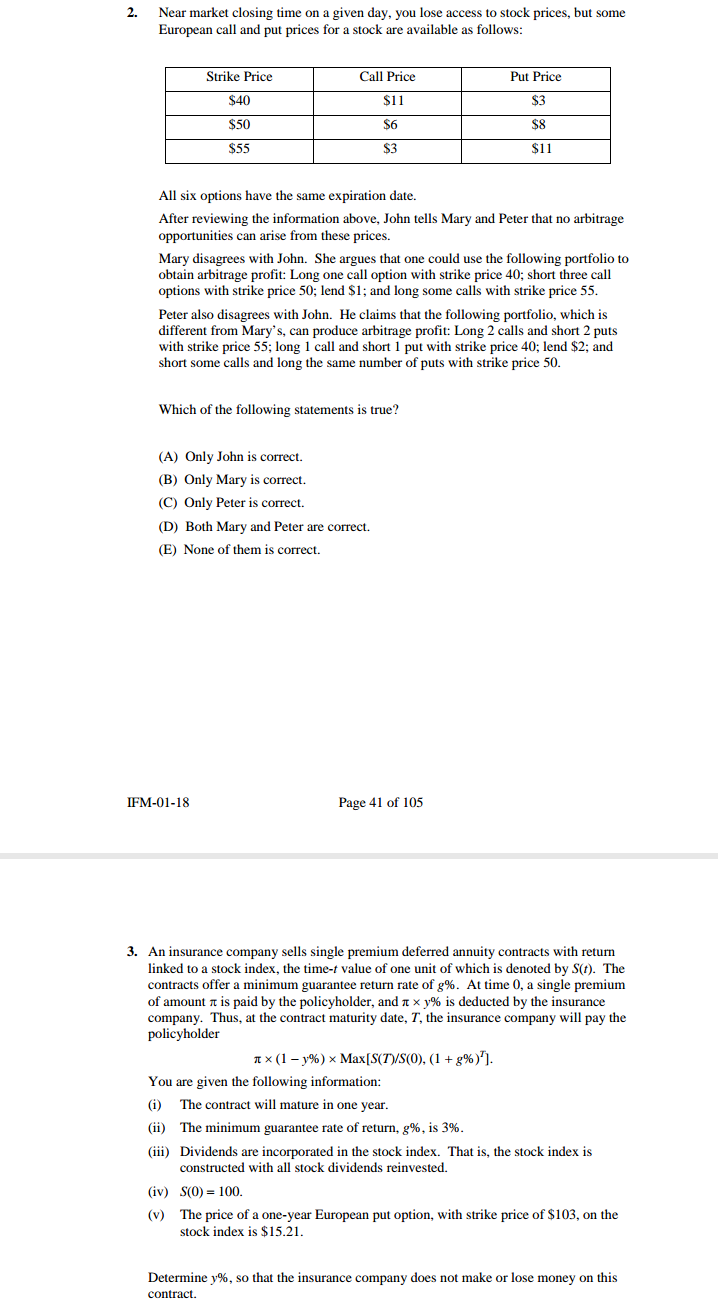

65. Assume that a single stock is the underlying asset for a forward contract, a K-strike call option, and a K-strike put option. Assume also that all three derivatives are evaluated at the same point in time. Which of the following formulas represents put-call parity? (A) Call Premium - Put Premium = Present Value (Forward Price - K) (B) Call Premium - Put Premium = Present Value (Forward Price) (9) Put Premium - Call Premium = 0 (D) Put Premium - Call Premium = Present Value (Forward Price - K) (E) Put Premium - Call Premium = Present Value (Forward Price) 66. The current price of a stock is 80. Both call and put options on this stock are available for purchase at a strike price of 65. Determine which of the following statements about these options is true. (A) Both the call and put options are at-the-money. (B) Both the call and put options are in-the-money. (C) Both the call and put options are out-of-the-money. (D) The call option is in-the-money, but the put option is out-of-the-money. (E) The call option is out-of-the-money, but the put option is in-the-money. IFM-01-18 Page 34 of 105 67. Consider the following investment strategy involving put options on a stock with the same expiration date. i) Buy one 25-strike put ii ) Sell two 30-strike puts iii) Buy one 35-strike put Calculate the payoffs of this strategy assuming stock prices (i.e., at the time the put options expire) of 27 and 37, respectively. (A) -2 and 2 (B) 0 and 0 (C) 2 and 0 (D) 2 and 2 (E) 14 and 071. A certain stock costs 40 today and will pay an annual dividend of 6 for the next 4 years. An investor wishes to purchase a 4-year prepaid forward contract for this stock. The first dividend will be paid one year from today and the last dividend will be paid just prior to delivery of the stock. Assume an annual effective interest rate of 5%. Calculate the price of the prepaid forward contract. (A) 12.85 (B) 13.16 (C) 17.29 (D) 18.72 (E) 21.28 72. CornGrower is going to sell corn in one year. In order to lock in a fixed selling price, CornGrower buys a put option and sells a call option on each bushel, each with the same strike price and the same one-year expiration date. The current price of corn is 3.59 per bushel, and the net premium that CornGrower pays now to lock in the future price is 0.10 per bushel. The continuously compounded risk-free interest rate is 4%. Calculate the fixed selling price per bushel one year from now. (A) 3.49 (B) 3.63 (C) 3.69 (D) 3.74 (E) 3.84 IFM-01-18 Page 37 of 105 73. The current price of a non-dividend-paying stock is 100. The annual effective risk-free interest rate is 4%, and there are no transaction costs. The stock's two-year forward price is mispriced at 108, so to exploit this mispricing, an investor can short a share of the stock for 100 and simultaneously take a long position in a two-year forward contract. The investor can then invest the 100 at the risk-free rate, and finally buy back the share of stock at the forward price after two years. Determine which term best describes this strategy. (A) Hedging (B) Immunization (C) Arbitrage (D) Paylater (E) Diversification2. Near market closing time on a given day, you lose access to stock prices, but some European cal] and put prices for a stock are available as follows: Strike Price Call Price Put Price $40 51 1 $3 $50 $6 $8 $55 $3 $1 1 All six options have the same expiration date. After reviewing the information above, John tells Mary and Peter that no arbitrage opportunities can arise from these prices. Mary disagrees with John. She argues that one could use the following portfolio to obtain arbitrage profit: Long one call option with strike price 40; short three call options with strike price 50; lend $1; and long some calls with strike price 55. Peter also disagrees with John. He claims that the following ponfolio, which is different from Mary's, can produce arbitrage profit: [mg 2 calls and short 2 puts with strike price 55; long 1 call and short 1 put with strike price 40; lend $2; and short some calls and long the same number of puts with strike price 50. Which of the following statements is true? (A) Only John is correct. (B) Only Mary is correct. (C) Only Peter is correct. (D) Both Mary and Peter are correct. {E} None of them is correct. IFM-Dl-l Pagedl of105 3. An insurance company sells single premium deferred annuity contracts with return linked to a stock index, the time-r value of one unit of which is denoted by 5\"). The contracts offer a minimum guarantee return rate Ofg'lh. At time 0, a single premium of amount I: is paid by the policyholder, and it it t. is deducted hy the insurance company. Thus, at the contract maturity date, 1", the insurance company will pay the policyholder n x (1 y%) x Maxlsavsw). (1 + 3% . You are given the following information: (i) The contract will mature in one year. (ii) The minimum guarantee rate of return. 3%, is 3%. (iii) Dividends are incorporated in the stock index. That isI the stock index is constructed with all stock dividends reinvested. (iv) 5(0) = 10!]. (v) The price ofa one-year European put optionI with strike price of $103, on the stock index is $15.21. Determine y'i, so that the insurance company does not make or lose money on this contract. 4. Fora two-period binomial model, you are given: (i) Each period is one year. (ii) The current price for a nondividend-paying stock is 20. (iii) a = 1.2340, where u is one plus the rateof capital gain on the stock per period if the stock price goes up. (iv) d: 0.3601 where d is one plus the rate of capital loss on the stock per period if the stock price goes down. (v) The continuously compounded risk-free interest rate is 5%. Calculate the price ofan American call option on the stock with a strike price of221 (A) t] (B) 1 (C) 2 (D) 3 (E) 4 5. Consider a 9-month dollar-denominated American put option on British pounds. You are given that: (i) The current exchange rate is 1.43 US dollars per pound. (ii) The strike price ofthe put is 1.56 US dollars per pound. (iii) The volatility of the exchange rate is a: {13. (iv) The US dollar continuously compolmded risk-free interest rate is 8%. (v) The British pound continuously compounded risk-free interest rate is 9%. Using a three-period binomial modelI calculate the price of the put. (A) 0.23 (B) 0.25 (C) 0.2? (D) 0.29 (E) 0.3] IFM-Dl-l Page 43 of 105 6. You are considering the purchase of 100 units of a 3-month 25-strilte European call option on a stock. You are given: (i) The Black-Scholes framework holds. (ii) The stock is currently selling for 20. (iii) The stock's volatility is 24%. (iv) The stock pays dividends continuously at a rate proportional to its price. The dividend yield is 3%. (v) The continuously compounded risk-free interest rate is 5%. Calculate the price of the block of 100 options. (A) 0.04 (B) 1.93 (C) 3.63 (D) 4.22 (E) 5.09 7. Company A is a U.S. international company, and Company B is a Japanese local company. Company A is negotiating with Company B to sell its operation in Tokyo to Company B. The deal will be settled in Japanese yen. To avoid a loss at the time when the deal is closed due to a sudden devaluation of yen relative to dollar, Company A has decided to buy at-the-money dollar-denominated yen put of the European type to hedge this risk. You are given the following information: (i) The deal will be closed 3 months from now. (ii) The sale price of the Tokyo operation has been settled at 120 billion Japanese yen. (iii) The continuously compounded risk-free interest rate in the U.S. is 3.5%. (iv) The continuously compounded risk-free interest rate in Japan is 1.5%. (v) The current exchange rate is 1 U.S. dollar = 120 Japanese yen. (vi) The daily volatility of the yen per dollar exchange rate is 0.261712%. (vii) 1 year = 365 days; 3 months = 14 year. Calculate Company A's option cost. IFM-01-18 Page 44 of 105 (A) 7.32 million (B) 7.42 million (C) 7.52 million (D) 7.62 million (E) 7.72 million 8. You are considering the purchase of a 3-month 41.5-strike American call option on a nondividend-paying stock. You are given: (1) The Black-Scholes framework holds. (ii) The stock is currently selling for 40. (iii) The stock's volatility is 30%. (iv) The current call option delta is 0.5. Determine the current price of the option. (A) 20 - 20.453 ] _ (B) 20 - 16.138 0.15 -x re-x- 12dx (0.15 -x2 /2dx (C) 20 - 40.453 -e- (D) 16.138 .e-x- /2dx - 20.453 (E) 40.453 (0.15 -x2 /2dx - 20.4539. Consider the Black-Scholes framework. A market-maker, who delta-hedges, sells a three-month at-the-money European call option on a nondividend-paying stock. You are given: (i) The continuously compounded risk-free interest rate is 10%. (ii) The current stock price is 50. (iii) The current call option delta is 0.61791. (iv) There are 365 days in the year. If, after one day, the market-maker has zero profit or loss, determine the stock price move over the day. (A) 0.41 (B) 0.52 (C) 0.63 (D) 0.75 (E) 1.11 10-17. DELETED 18. A market-maker sells 1,000 1-year European gap call options, and delta-hedges the position with shares. You are given: (i) Each gap call option is written on 1 share of a nondividend-paying stock. (ii) The current price of the stock is 100. (iii) The stock's volatility is 100%. (iv) Each gap call option has a strike price of 130. (v) Each gap call option has a payment trigger of 100. (vi) The risk-free interest rate is 0%. Under the Black-Scholes framework, determine the initial number of shares in the delta-hedge. IFM-01-18 Page 46 of 105 (A) 586 (B) 594 684 (D) 692 (E) 797 19. Consider a forward start option which, 1 year from today, will give its owner a 1-year European call option with a strike price equal to the stock price at that time. You are given: (i) The European call option is on a stock that pays no dividends. (ii) The stock's volatility is 30%. (iii) The forward price for delivery of 1 share of the stock 1 year from today is 100. (iv) The continuously compounded risk-free interest rate is 8%