help finding total variance, spending variance and efficiency variance

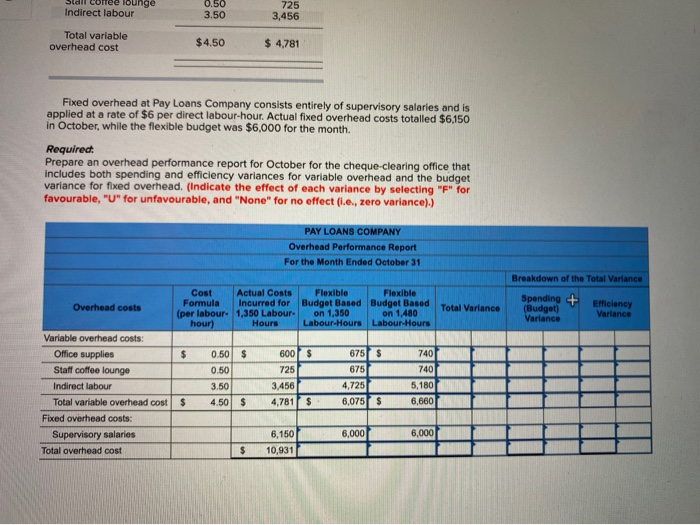

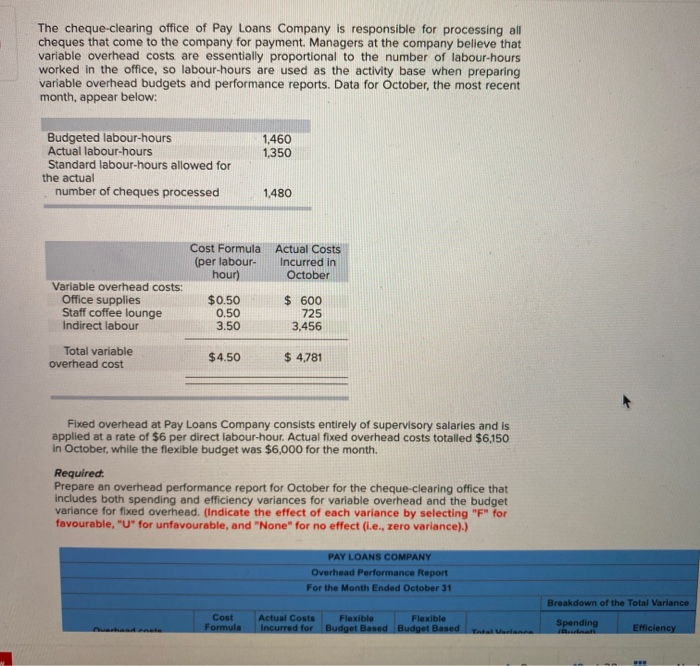

The cheque-clearing office of Pay Loans Company is responsible for processing all cheques that come to the company for payment Managers at the company believe that variable overhead costs are essentially proportional to the number of labour-hours worked in the office, so labour-hours are used as the activity base when preparing variable overhead budgets and performance reports. Data for October, the most recent month, appear below: 1,460 1,350 Budgeted labour-hours Actual labour-hours Standard labour-hours allowed for the actual number of cheques processed 1,480 Cost Formula (per labour- hour) Actual Costs Incurred in October Variable overhead costs: Office supplies Staff coffee lounge Indirect labour $0.50 0.50 3.50 $ 600 725 3,456 Total variable overhead cost $4.50 $ 4,781 Fixed overhead at Pay Loans Company consists entirely of supervisory salaries and is applied at a rate of $6 per direct labour-hour. Actual fixed overhead costs totalled $6,150 in October, while the flexible budget was $6,000 for the month. Required: Prepare an overhead performance report for October for the cheque-clearing office that includes both spending and efficiency variances for variable overhead and the budget variance for fixed overhead. (indicate the effect of each variance by selecting "F" for favourable, "U" for unfavourable, and "None" for no effect (ie, zero variance).) PAY LOANS COMPANY Overhead Performance Report For the Month Ended October 31 Breakdown of the Total Variance Cost Formula Actual Costs Incurred for Flexible F lexible Budget Based Budget Based Spending Eiciency Jual Lulee lounge Indirect labour 0.50 3.50 725 3,456 Total variable overhead cost $4.50 $ 4,781 Fixed overhead at Pay Loans Company consists entirely of supervisory salaries and is applied at a rate of $6 per direct labour-hour. Actual fixed overhead costs totalled $6,150 in October, while the flexible budget was $6,000 for the month. Requirect Prepare an overhead performance report for October for the cheque clearing office that includes both spending and efficiency variances for variable overhead and the budget variance for fixed overhead. (Indicate the effect of each variance by selecting "F" for favourable, "U" for unfavourable, and "None" for no effectie, zero variance).) PAY LOANS COMPANY Overhead Performance Report For the Month Ended October 31 Breakdown of the Total Variance Overhead costs Cost Actual Costs Flexible Flexible Formula Incurred for Budget Based Budget Based (per labour. 1,350 Labour on 1,350 on 1,480 hour) Hours Labour Hours Labour Hours Total Variance Spending + (Budget) Variance Efficiency Variance $ $ $ $ Variable overhead costs: Office supplies Staff coffee lounge Indirect labour Total variable overhead cost Faced overhead costs Supervisory salaries Total overhead cost 0.50 0.50 3.50 4.50 600 725 3.456 4,781 675 675 4.725 6,075 7401 740 5,180 6,660 $ $ $ $ 6.000 6.000 6,150 10.931 $