Help help help tutors...dont give answers without Workings

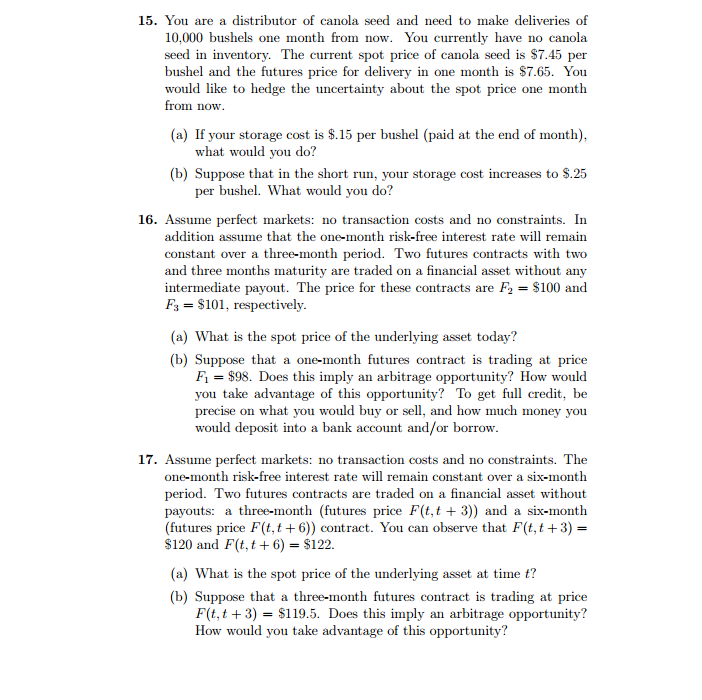

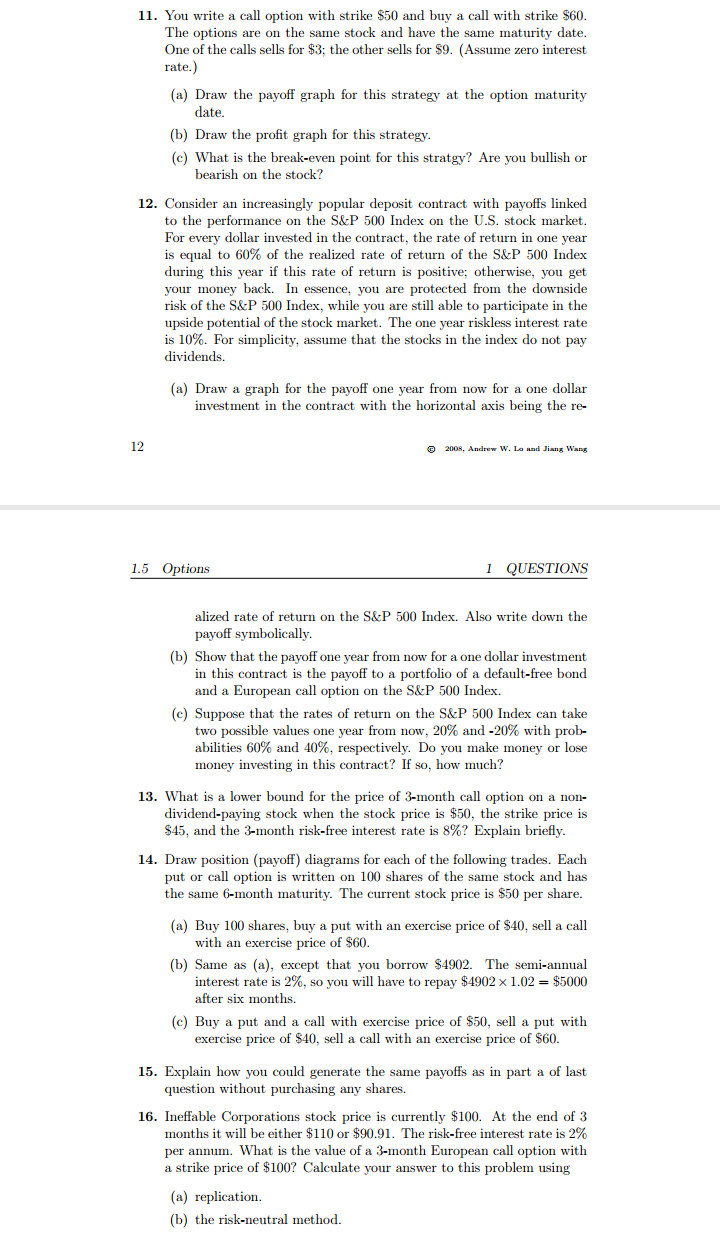

15. You are a distributor of canola seed and need to make deliveries of 10,000 bushels one month from now. You currently have no canola seed in inventory. The current spot price of canola seed is $7.45 per bushel and the futures price for delivery in one month is $7.65. You would like to hedge the uncertainty about the spot price one month from now. (a) If your storage cost is $.15 per bushel (paid at the end of month), what would you do? (b) Suppose that in the short run, your storage cost increases to $.25 per bushel. What would you do? 16. Assume perfect markets: no transaction costs and no constraints. In addition assume that the one-month risk-free interest rate will remain constant over a three-month period. Two futures contracts with two and three months maturity are traded on a financial asset without any intermediate payout. The price for these contracts are F2 = $100 and F3 = $101, respectively. (a) What is the spot price of the underlying asset today? (b) Suppose that a one-month futures contract is trading at price F1 = $98. Does this imply an arbitrage opportunity? How would you take advantage of this opportunity? To get full credit, be precise on what you would buy or sell, and how much money you would deposit into a bank account and/or borrow. 17. Assume perfect markets: no transaction costs and no constraints. The one-month risk-free interest rate will remain constant over a six-month period. Two futures contracts are traded on a financial asset without payouts: a three-month (futures price F(t, t + 3)) and a six-month futures price F(t,t + 6)) contract. You can observe that F(t, t + 3) = $120 and F(t, t + 6) = $122. (a) What is the spot price of the underlying asset at time t? (b) Suppose that a three-month futures contract is trading at price F(t, t+3) = $119.5. Does this imply an arbitrage opportunity? How would you take advantage of this opportunity?1.5 Options 1. A stock price is currently $50. It is known that at the end of two months it will be either $53 or $48. The risk-free interest rate is 10% per annum with continuous compounding. What is the value of a two- month European call option with a strike price of $49? 2. A stock price is currently $80. It is known that at the end of four months it will be either $75 or $85. The risk-free interest rate is 5% per annum with continuous compounding. What is the value of a four- month European put option with a strike price of $80? 3. Today's price of three traded call options on BackBay.com, all expiring in one month, are as follows: Strike Price Option Price $50 60 $3 70 You are considering buying a "butterfly spread" consisting of the fol- lowing positions: . Buy 1 call at strike price of $50 . Sell (write) 2 calls at strike price of $60 . Buy 1 call at strike price of $70. (a) Plot the payoff of your total position for different values of the stock price on the maturity date. (b) What is the dollar investment required to establish the spread? (c) For what stock prices on the maturity date will you be making an overall profit? 4. You are given the following prices: Security Maturity (years) Strike Price ($) JEK stock 94 Put on JEK stock 50 3 Put on JEK stock 60 Call on JEK 50 Call on JEK 60 Tbill (FV=100) 1 91 What is the price of the two call options?1". IBM shares are now traded at $80.00. The term structure of interest rates is at at 5%. (a) Plot the tenninal payoff from a European put option on 1 share of IBM with a exercise price of $85 and a maturity of 3 months (not including the price of the option}. [b] Suppose that you purchase the put Optiou at $4.00 tram the mar- ket. Specify the ranges of IBM share price at the options maturity date or which you will be making a net prot. 3. Suppose that after a recent news about the economy1 IBM share price remains the same, but the prices of its options shot up. How is this possible? 9. You are given the following information. Use this information to de- termine the unknown prices. Table 2: Stock, Options, and T-bill prices SECutiry Maturity years) Strike Prim 5 401 Stock - - $100 Put on 401 Stock 1 $50 33 Put on 401 Stock 1 $30 $5 Calle on 401 Stock 1 $512} SKEW Calle on 401 Stock 1 $50 '? TbimFV=moJ 1 - ? 10. Joseph Jones, a manager at Computer Science, Inc. (CSI), received 1,001) shares of company stock as part of his compensation package. The stock currently sells at $40 at share. Joseph wo1d like to defer selling the stock until the next tax year. In January, however, he will I]. @ m,a=s;..w.r..ad1i.n.ma. 1.5 Options 1 QUESTIONS need to sell all his holdings to provide for a down payment on his new house. Joseph is worried about the price risk involved in lumping his sharia. At current prices, he would receive $40.0(I) for the stock. If the value of his stock holdings falls below $35.02!), his ability to come up with the necessary down payment would be jeopardized. On the other hand, if the stock value rises to 545.0(1), he would be able to maintain a small cash resenre even after making the down payment. Joseph considers three investment strategies: (a) Strategy A is to write January call options on the CS] shares with strike price $45. There calls are currently selling for $3 each. [h] Strategy B is to buy January put options on CSI with strike price $35. These options also sell for $3 each. [c] Strategy C is to establish a zero-cost collar by writing the January calls and buying the January puts. Evaluation each of these strategies with respect to Joseph's investmem goals. What are the advantages and disadvantages of each? Which would you reocmmeud? 11. You write a call option with strike $50 and buy a call with strike $60. The options are on the same stock and have the same maturity date. One of the calls sells for $3; theother sells for $9. [Assume zero interest rate.) (a) Draw the payoff graph for this strategy at the option maturity date. [b] Draw the prot graph for this strategy. (c) What is the break-em point for this stratgy'? Are you bullish or bearish on the stock? 11. You write a call option with strike $50 and buy a call with strilne $60. The options are on the same stock and have the same maturity date. lDue of the calls sells for $3; theother sells for $9. [Assume zero interest rate.) {a} Draw the payoff graph for this strategy at the option maturity date. [b] Draw the prot graph for this strategy. {e} What is the break-even point for this stratgy'? Are you bullish or bearish on the stock? 12. Consider an increasingly popular deposit contract with payoffs linked to the performance on the 3.3.513 500 Index on the US. stock market. For every dollar invested in the contract, the rate of return in one year is equal to 60% of the realized rate of return of the 3.3.51:I 500 Index during this year if this rate of return is positive; otherwise, you get your money back. In essence1 you are protected from the downside risk of the S&P an Index, while you are still able to participate in the upside potential of the stock market. The one year rislrless interest rate is 10%. For simplicity1 assume that the stocks in the index do not pay dividends. {a} Draw a graph for the paonI one year from now for a one dollar investment in the contract with the horizontal axis being the re- 12 @ m.r|ndrrrw.1nlnd1in.''hq 1.5 Options 1 QUESTIONS alized rate of return on the S&P 500 Index. Also write down the payoff symbolically. [b] Show that the payoff one year from now for aone dollar imastment in this contract is the payoff to a portfolio of a default-free bond and a European call option on the S&P 500 Index. (c) Suppose that the rates of return on the S&P 5m Index can talre two possible values one year from now, 212% and 40% with prob- abilities 60% and 40%. respectively. Do you malice money or lose money investing in this contract? If so, how much? 13. What is a lower bound for the price of 3-month call option on a non- dividend-paying stoclr when the stoclr price is $50, the strike price is $45, and the 3-month risk-free interest rate is 3%? Explain briey. 14. Draw position [payoff] diagrams for each of the following trades. Each put or call option is writtm on 112]!) shares of the same stock and has the same l6-month maturity. The current stool: price is $50 per share. {a} Buy 100 shares1 buy a put with an exercise price of$4Cl1 sell a call with an exercise price of $60. [b] Same as [a], except that you borrow $4902. The semi-annual interest rate is 2%, so you will have to repay $4902 x 1.02 = $5000 after six months. (c) Buy a put and a call with exercise price of $50, sell a put with exercise price of $40, sell a call with an exercise price of $60. 15. Explain how you could generate the same payoffs as in part a of last question without purchasing any shares. 13. IneEl'able Corporations stoclr price is currently $100. At the end of 3 months it will be either $110 or $90.91. The risk-free interest rate is 2% per annum. What is the value of a 3-month European call option with a strike price of $100? Calculate your answer to this problem using (a) replication. {b} the risk-neutral method. 15. Explain how you could generate the same payoffs as in part a of last question without purchasing any shares. 15. IneEfable Corporatimrs stock price is currently $1001 At the end of 3 months it will be either $110 or $90.91. The risk-free interest rate is 2% per annum. What is the value of a 3-month European call option with a strike price of $100? Calculate your answer to this problem using (a) replication. {b} the risk-neutral method. 17. State whether the foowing statements are true or false. In each case1 provide a brief isrplmlatin. (a) In a risk averse world, the binomial model states that, other things being equal. the greater the probability of an up movement in the stock price, the lower the value of a European put option. 13 a \"Hindu-'\"LIHIadJi-ugm 1.5 Options 1 QUESTIONS [b] By observing the price; of call and put options on a stock, one can recover an estimate of the expected stock return {c} An investor would like to purchase a European call option on an underlying stock index with a strike price of 210 and a time to ma- turity of 3 months, but this option is not actively traded. However1 two otherwise identical call options are traded with strike prices of 2m and 22H respectively. hence the investor can replicate a call with a strike price of 210 by holding a static position in the two traded calls. [d] In a binomial world1 if a stock is more likely to go up in price than to go down, an increase in volatility would increase the price of a call option and reduce the price of a put option. Note that a static position is a position that. is chosen initially and not. rebalanced through time. Draw a diagram showing an investor's prot and loss with the terminal stock price for a portfolio consisting of: 18. (a) One share of stock and a short position in one call option [b] Two shares of stock and a shout position in one call option {c} One share of stock and a short position in two call options [d] One share of stock and a short position in four call options You should take into account the cost from purchasing the stock and revenue from selling the calls. For simplicity ignore discounting when combining these costs and revenues with the tm-minal payoff of the portfolio. For simplicity also assume that the current stock price is equal to the strike price, K, of the call. Denote the current call price by c, and the terminl Hindi mice by 3T: 19. Stock KYZ is rmrth S = $80 today. Every 6 months the stock price goes either up by u = 1.3 or down by d = 0.3. The riskless rate is 6% APR, with semiannual compounding. The stock pays no dividends. (a1 Compute the price of a European call with a. maturity of 1 year andastrilre priceofX=$95. [h] Compute the price of an American call with a maturity of 1 year andastrilre priceofX=$95. {cl Compute the price of a European put with a. maturity of 1 year andastrilre priceofX=$95. 20. In August 1993 the Bank of Thailand was reported as offering to foreign investors in troubled banks the opportunity to resell their shares back to the central bank within a period of ve years for the original purchase