Answered step by step

Verified Expert Solution

Question

1 Approved Answer

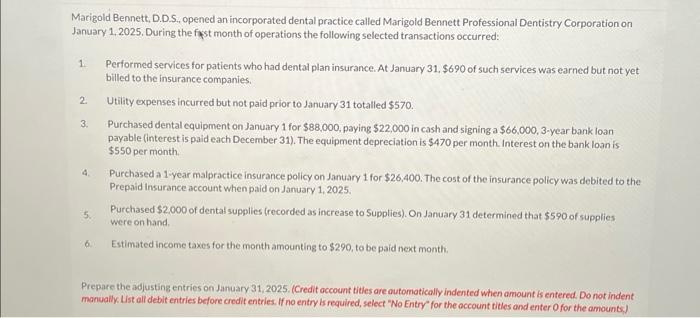

help Marigold Bennett, D.D.S., opened an incorporated dental practice called Marigold Bennett Professional Dentistry Corporation on January 1, 2025, During the fast month of operations

help

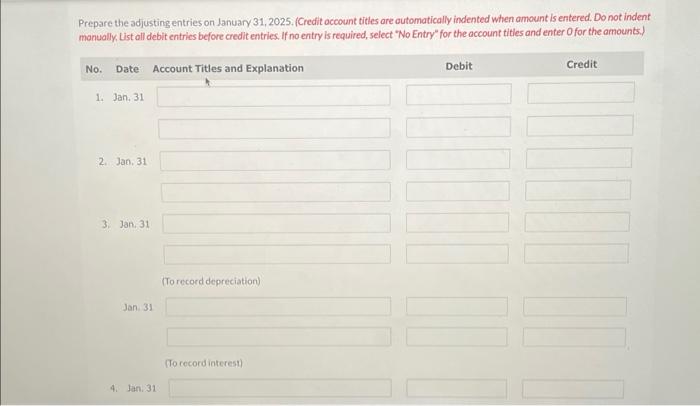

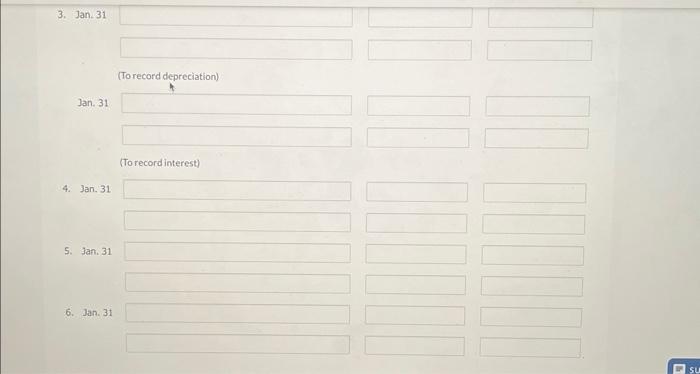

Marigold Bennett, D.D.S., opened an incorporated dental practice called Marigold Bennett Professional Dentistry Corporation on January 1, 2025, During the fast month of operations the following selected transactions occurred: 1. Performed services for patients who had dental plan insurance. At January 31,$690 of such services was earned but not yet billed to the insurance companies. 2. Utility expenses incurred but not paid prior to January 31 totalled $570. 3. Purchased dental equipment on January 1 for $88,000, paying $22,000 in cash and signing a $66,000,3-year bank loan payable (interest is paid each December 31 ). The equipment depreciation is $470 per month Interest on the bank loan is $550 permonth. 4. Purchased a 1-year malpractice insurance policy on January 1 for $26,400. The cost of the insurance policy was debited to the Prepaid Insurance account when paid on January 1, 2025. 5. Purchased $2.000 of dental supplies (recorded as increase to Supplies). On January 31 determined that $590 of supplies were on hand. 6. Estimated income taxes for the month amounting to $290, to be paid nekt month. Prepare the adjusting entries on January 31, 2025. (Credit occount tities are outomotically indented when amount is entered. Do not indent manually. List alf debit entries before credit entries. If no entry is required, select "No Entry" for the occount titles and enter o for the amounts.) Prepare the adjusting entries on January 31, 2025. (Credit occount titles are automatically indented when amount is entered. Do not indent manually, list all debit entries before credit entries. If no entry is required, select "No Entry" for the account tities and enter Ofor the amounts.) 3. Jan. 31 (To record depreciation) Jan. 31 (To record interest) 4. 3an,31 5. Jan. 31 6. Jan. 31 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Core Concepts Of Accounting

Authors: Robert N. Anthony, Leslie Pearlman Breitner

8th Edition

0130406716, 9780130406712