Help me make a strategic plan on the case study attached below. Star Appliance Company (A) 9 Arthur Foster, the nancial vice president of Star

Help me make a strategic plan on the case study attached below.

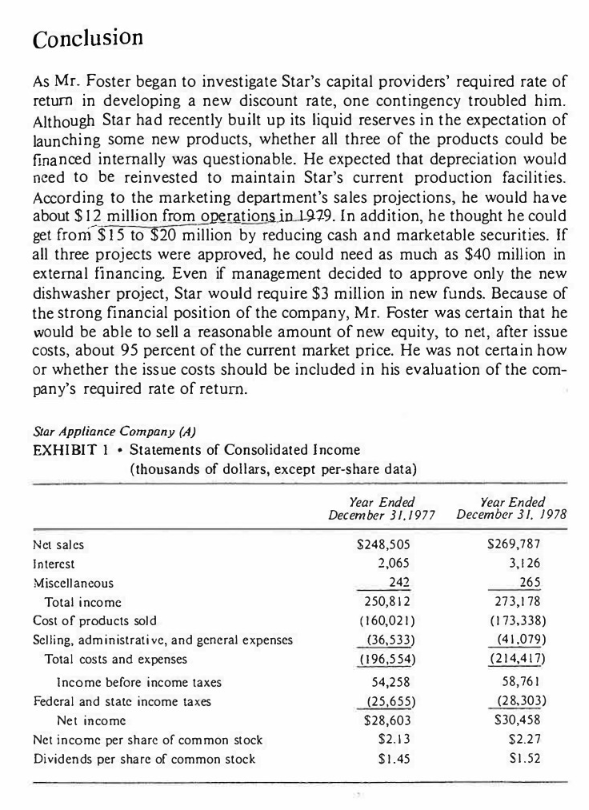

Star Appliance Company (A) 9 Arthur Foster, the nancial vice president of Star Appliance Cumpany, thought that the Opportunity had nally presented itself. Sincejoining the company in early-122%, he had been concerned about the l _r_a_t_e [also called the hurdle rate) used in the capitaluallocation process. He had not wanted to create a controversy immediately after accepting his posi* tion, but now in early October 1979, with the company considering a move into new products, he thought that the time had cume for discussing the company's rewiretLrate 91.1119???\" investment (frequently referred to as the cost of capitat). History of Star Appliance Company Star Appliance had been founded in 1922 by Ken McDonald to manufac- ture electric stovgndcvens During the prosperous 292th, the demand for electric stoves and ovens as replacements for wood- and coal-burning stoves increased. and Star became a'respected brand name and the market leader. Capitalizing on this success and'the burgeoning equity market dur- ing the 19205, Mr. McDonald nanced the rapid growth of the company through the sale ofcommon stock. This move proved to be farsighted; The companyr was able to enter the Depression with a debtfree balance sheet. Many rms, plagued with dwindling sales and poor or nonexistent prots, had defaulted on their debts and were forced into bankruptcy and eventu ally out of business. Star suffered severely during the Depression, but was able to survive by significantly reducing its operations and concentrating its sales efforts on the least affected part of the market, the premium end. As a result, Star remained alive and viable, emerging at the end ofWorld War it with a smaller base of operations, a strong balance sheet, and a well- established reputation in the marketplace. In the ensuing three decades. the company grew and prospered. Star continued to concentrate on the premium market and over the years introduction of new products might provide an impetus to the stock mar- ket, thus increasing the company's priceleamings {PIE} ratio back to its normal levels. Three new product lines had been proposed-a dishwasher, a food disposer to be installed in kitchen sinks. and a trash compactor. The mar- keting department believed that each of these products had good sales potential and would fit with the company image ofhigh-quality, premium- priced kitchen products. Each of the three projects had been analyzed following the require- ments of Star's capital-allocation process. Like most projects at Star, these bad originated in either the marketing or manufacturing departments. For each, the costs, benets. expected lives, and terminal values had been deter- mined. The results oi' the analysis for each project are shown in Exhibit 4. Using Star's marginal tax rate, the after-tax cash ows were used to calculate the internal rate of return {IRR} for each project. Following Star's usual procedures, the ERR would then be compared with the company's lO-per- cent discount rate. Star's management would accept projects whose IRR exceeded the discount rate as long as funds were available. In years when capital was short, projects with the highest lRRs were implemented, and lower return projects were postponed until funds became available. Several parts of this process troubled Mr. Foster. First, he was con- cerned about the appropriateness of the lO-percent required rate of return. When he joined the company, he had asked about the source ofthe rate. but noeseemed to be able_t_p_give,a precisereason, for it. The best he could determinE'wa's"Hiat' the return on equity seemed to have been about It] percent during the period when the capitalbudgeting system was being Established, and since that time, the IO-percent rate had boon used; Mr. Foster was convinced that the discount rate was too low. The interest rate on various US. Treasury securities is shown in Exhibit 5. Treasury bills had recently exceeded 1} pgrcent= and one study showed that common stock historically had a return of about 3.5 percent above the average return on Treasury billsand gment ribosomes term Treasury securities. He was certain that Star's projects were more risky than Treas- ury bills, and thus the projects should have a higher expected return if they were to be accepted. 0n the other hand, Mr. Foster did not believe that Star's stock was as risky as the average common stock. This suggested to him that the full market 'sk premium would not be expected by investors in Star's common stock.r At the manufacturing company where Mr. Foster had worked before joining Star, a dividend-growth model had been used in calculating the cost of equity. This model {B11939 + g = Kt) described the return expected by the shareholders {Kt} from investing in the company's common stock as a combination of the next dividend (91), current market price {Po} [the dividend yield [lefufl], and the forecasted long-term growth in dividends (g). Star's current stock price was $22.50. and the company's management and board of directors intended to continue its policy of maintaining or slightly increasing dividends. Information about Star's historic dividends, along with other information about Star's stock and the stock market, can be found in Exhibit 6. Because Star had only short-term debt, Mr. Foster did not believe he should consider the cost ofdebt in calculating the return required by Star 5 capital providers. However,_ there _wame. _thing _that_ perplexed him. If_a_n alluequtygnancedmshegpshy m_ economic downturns, why _ __ f of capital be higher? It was obvious that debt cost less than equity [especially after taking taxes into account} and that the use of debt would reduce a company' 5 overall average required rate of return. In his reviewofthe discount rate and capital providers' required rate of return, several other questions occurred to Mr. Foster. First, was ina- tj_o_r1_ad_e_gl_1at_e1y accounted for in Stars present system? Mr. Foster believed that the rates on U. 3 Treasury securities (Exhibits 5 and 6) included a return to offset expected ination but was that enough?r '- " Second. Mr. Foster wondered whether Star management should accept projects that just met the required rate of return. or only those that exceeded it by a margin ofsafety. Some ofthe forecasts had, in the past. exceeded the results. Perhaps the required rate should be raised to com- pensate for poor forecasts. Furthermore, Star, like other US. companies1 had increased its investment in safety and environmental projects to sat- isfy the U.S. government's increased requirements. Like most companies. Star categorized these as nonproductive investments; investments with no return. The discount rate, Mr. Foster believed. should certainly be increased to cover those investments1 for failing to do so would guarantee that Star would earn less than its required rate, and shareholders would be hurt. Finally. the staff making the forecasts for the three projects believed that two of the projects were ri_s_k_ie_r than the otherpne, because they required new plant and equipment that would add appreciably to fixed costs. In ddwntums, or ifthe projects proved unsuccessful, they could cost Star more. Some of the staff thought that the rate required should be increased to compensate for risk. Others argued that the more risky proj ects should be evaluated on the basis of their strategic importance and that the rate used was irrelevant. the company should accept the sound stratr egy. Dne yog a_n_ahrst_contend_ed__ that if different rates were. 21.1st for different projects. the company would be mixing the nancing and investment decisionssomething that should not be done Conclusion As Mr. Foster began to investigate Star's eapital providers' reoui red rate of return in deveIOping a new discount rate, one contingency troubled him) Although Star had reoentlj.r built up its liquid reserves in the expectation of Iaunching some new products, whether all three of the products could be nanced internally was questionable, He expected that depreciation would need to be reinvested to maintain Star's current production facilities. According to the marketing department's sales projections, he would have about Si2 million fromgperatiirtsjnsmlg. In addition, he thought he could get fromrgmillion by reducing cash and marketable securities. if all three projects were approved, he could need as much as $40 million in external nancing Even it management decided to approve only the new dishwasher project, Star would require $3 million in new funds. Because of the strong nancial position ofthe company, Mr. Foster was certain that he would be able to sell a reasonable amount of new equity, to nets after issue costs, about 95 percent ofthe current market prices He was not certain how er whether the issue costs should be included in his evaluation of the com pany's required rate of return. Star Appliance Company {H} EXHIBIT 1 - Statements of Consolidated Income {thousands of dollars. except per-share data} Year Ended Year Ended DeCember NJ??? December 3!. NM Net sales 5243.505 $269.13? interest 2.065 3.E2l5 Miscellaneous 242 265 Total income 250,8l2 213,!13 Cost of products sold \"60,132 I] [I 73.333} Selling, administrative, and general expenses {35.533} {41.0\"} Total costs and expenses \"96.554: (El-1.4L?) income before income taxes 54.253 5836! Federal and state income taxes {25.655} (23.303) Net income $23,603 $30,453 Net income per share of common stock 32. IE $2.27 Dividends per share ofoornmon stock Sl.45 ELSE

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance