Answered step by step

Verified Expert Solution

Question

1 Approved Answer

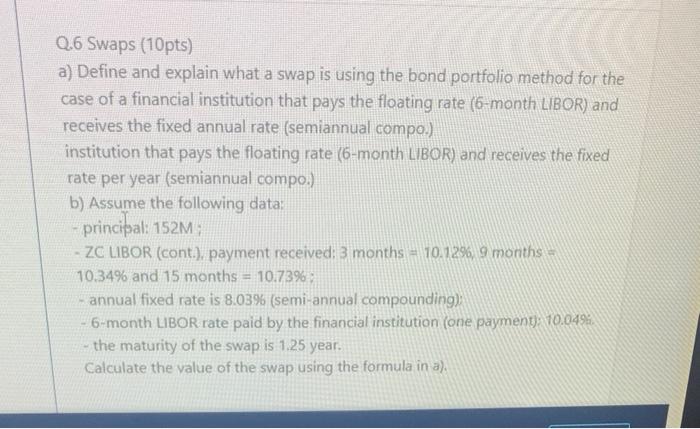

help me solve this and show me all the steps please Q.6 Swaps (10pts) a) Define and explain what a swap is using the bond

help me solve this and show me all the steps please

Q.6 Swaps (10pts) a) Define and explain what a swap is using the bond portfolio method for the case of a financial institution that pays the floating rate (6-month LIBOR) and receives the fixed annual rate (semiannual compo.) institution that pays the floating rate (6-month LIBOR) and receives the fixed rate per year (semiannual compo.) b) Assume the following data: - principal: 152M: - ZC LIBOR (cont.). payment received: 3 months =10.1296,9 months = 10.34% and 15 months =10.73% : - annual fixed rate is 8.03% (semi-annual compounding): -6-month LIBOR rate paid by the financial institution (one payment) 10.049e - the maturity of the swap is 1.25 year. Calculate the value of the swap using the formula in a). Q.6 Swaps (10pts) a) Define and explain what a swap is using the bond portfolio method for the case of a financial institution that pays the floating rate (6-month LIBOR) and receives the fixed annual rate (semiannual compo.) institution that pays the floating rate (6-month LIBOR) and receives the fixed rate per year (semiannual compo.) b) Assume the following data: - principal: 152M: - ZC LIBOR (cont.). payment received: 3 months =10.1296,9 months = 10.34% and 15 months =10.73% : - annual fixed rate is 8.03% (semi-annual compounding): -6-month LIBOR rate paid by the financial institution (one payment) 10.049e - the maturity of the swap is 1.25 year. Calculate the value of the swap using the formula in a) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Oxford Guide To Financial Modeling

Authors: Thomas S Y Ho, Sang Bin Lee

1st Edition

019516962X, 9780195169621