Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Help! Please show work!! Answer is C, but I'm struggling to come up with the work!! Thank you!! Q20 (4 pts) There are three zero-coupon

Help! Please show work!! Answer is C, but I'm struggling to come up with the work!! Thank you!!

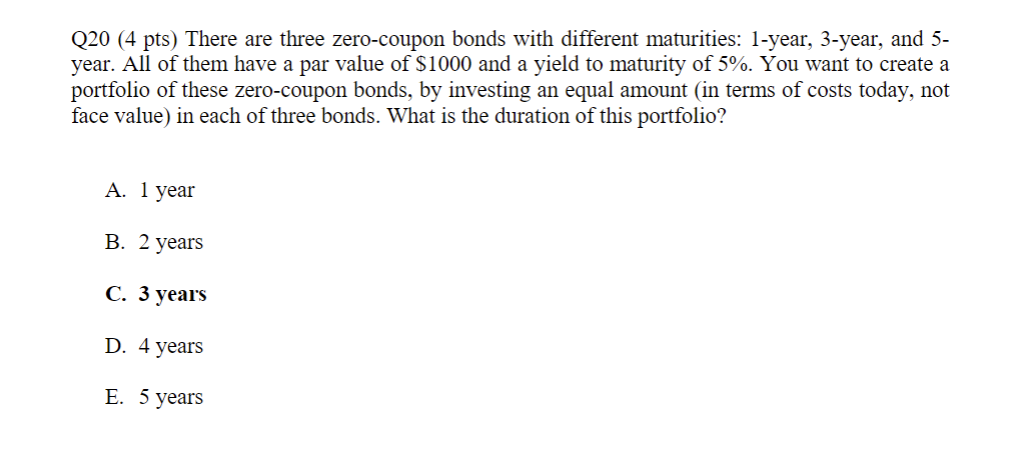

Q20 (4 pts) There are three zero-coupon bonds with different maturities: 1-year, 3-year, and 5year. All of them have a par value of $1000 and a yield to maturity of 5%. You want to create a portfolio of these zero-coupon bonds, by investing an equal amount (in terms of costs today, not face value) in each of three bonds. What is the duration of this portfolio? A. 1 year B. 2 years C. 3 years D. 4 years E. 5 years

Q20 (4 pts) There are three zero-coupon bonds with different maturities: 1-year, 3-year, and 5year. All of them have a par value of $1000 and a yield to maturity of 5%. You want to create a portfolio of these zero-coupon bonds, by investing an equal amount (in terms of costs today, not face value) in each of three bonds. What is the duration of this portfolio? A. 1 year B. 2 years C. 3 years D. 4 years E. 5 years Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Before You Buy The Homebuyers Handbook For Todays Market

Authors: Michael Corbett, Jim Gillespie

1st Edition

0452296803, 978-0452296800