Answered step by step

Verified Expert Solution

Question

1 Approved Answer

HELP PLEASE!!! this is my second attempt. i need the journal entries, income statement, and balance sheet!!! RWP1U-1 (Static) Great Adventures Continuing Case (GL) Tony

HELP PLEASE!!! this is my second attempt. i need the journal entries, income statement, and balance sheet!!!

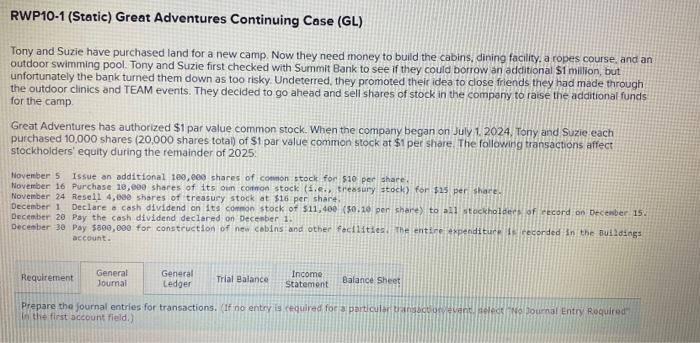

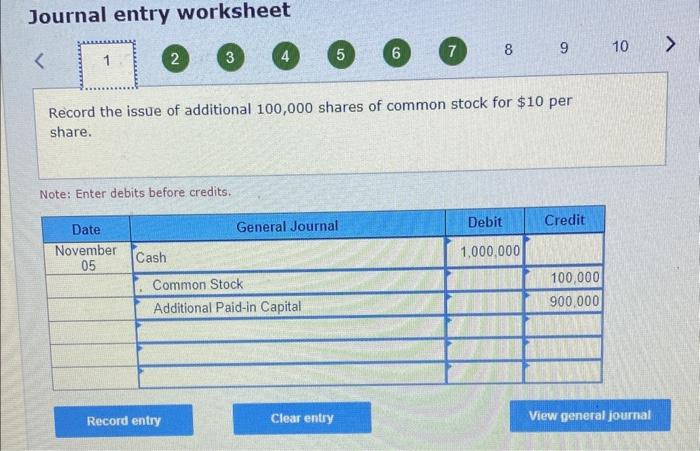

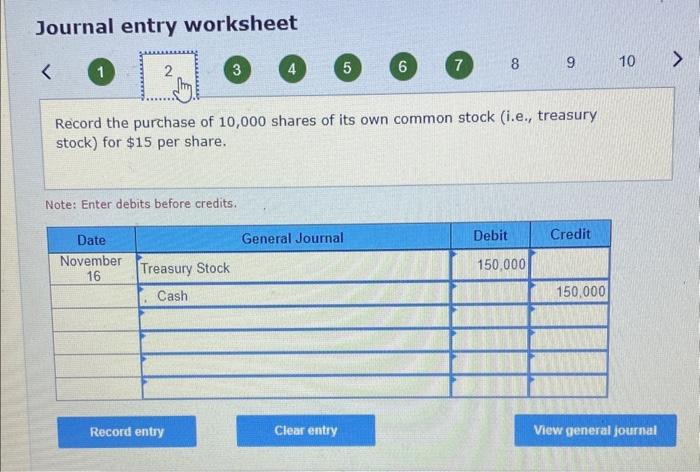

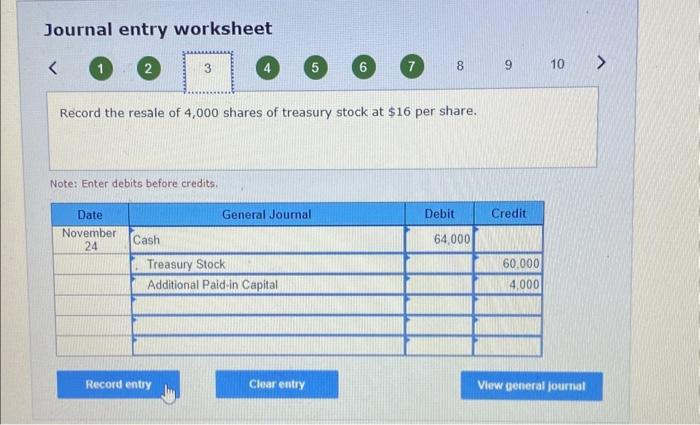

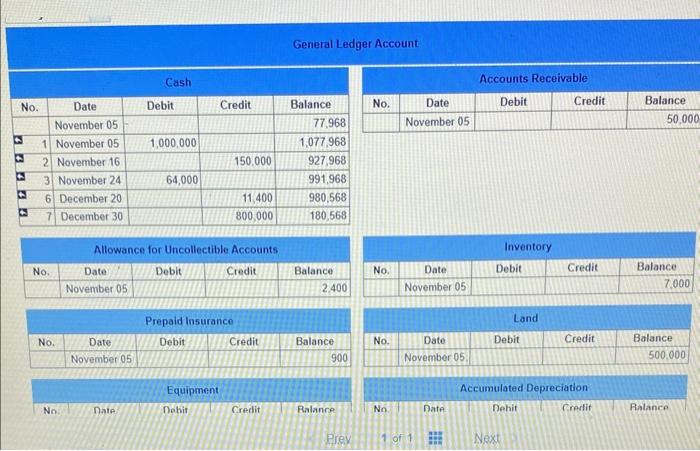

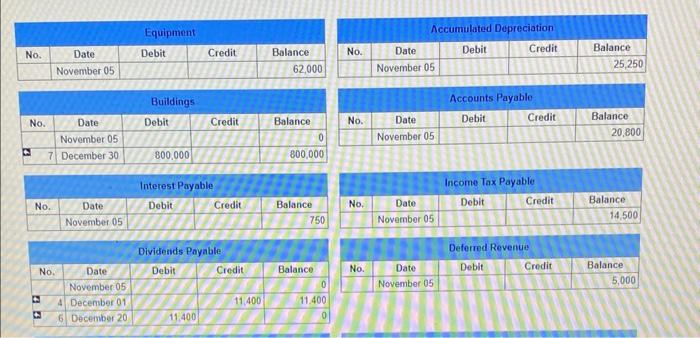

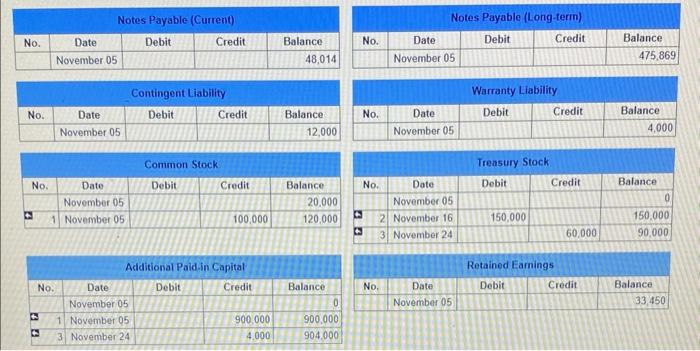

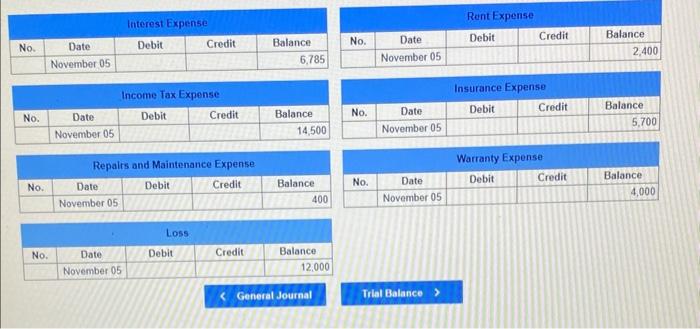

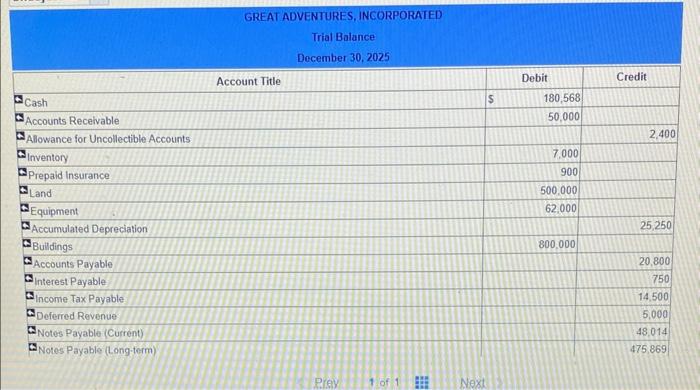

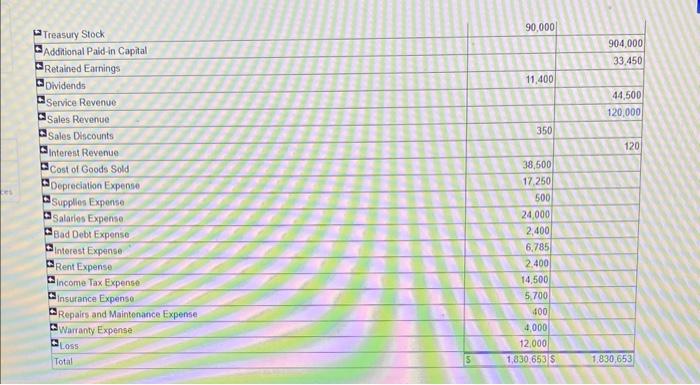

RWP1U-1 (Static) Great Adventures Continuing Case (GL) Tony and Suzie have purchased land for a new camp. Now they need money to build the cabins, dining facility, a ropes course, and an outdoor swimming pool. Tony and Suzie first checked with Summit Bank to see if they could borrow an additional \$1 milion, but. unfortunately the bank turned them down as too risky. Undeterred, they promoted their idea to close friends they had made through the outdoor clinics and TEAM events. They decided to go ahead and sell shares of stock in the company to raise the additional funds for the camp. Great Adventures has authorized \$1 par value common stock. When the company began on July 1. 2024, Tony and Suzie each purchased 10,000 shares (20,000 shares totai) of \$1 par value common stock at $1 per share. The following transactions affect stockholders' equity during the remainder of 2025 . Hovenber 5 Issue an additional 100 , e00 shares of connon stock for 510 per share. Novertber 16 Purchase 10,000 shares of 1 ts oin coinon stock (1,e., preasury stock) for \$15, per share. Noveriber 24 Resel1 4,000 shares of treasury stock at \$16 per shara December 1 Declare a cosh dividend on 1ts compon stock of 511,400 (\$0.20 per share) to az1 stockholdees of icecord on Decenber 15. Deceaber 20 Pay the cosh dividend declared on Decenber 1. December 30 Pay 5800,000 for construction of new cobins and other foctlities. The entire Axpenditure if recorded In the fuidding account: in the first occount field.) Journal entry worksheet 789 Record the issue of additional 100,000 shares of common stock for $10 per share. Note: Enter debits before credits. Journal entry worksheet (7) 89 Record the purchase of 10,000 shares of its own common stock (i.e., treasury stock) for $15 per share. Note: Enter debits before credits. Journal entry worksheet 1 5 6 7 8 Record the resale of 4,000 shares of treasury stock at $16 per share. Note: Enter debits before credits. Journal entry worksheet 1 2 6 (7) 8 9 Record the declaration of $11,400 ( $0.10 per share) cash dividend on its common stock to all stockholders of record on December 15. Note: Enter debits before credits. Journal entry worksheet 1 2 6 Record the entry on December 15 , the date of record. Note: Enter debits before credits. Journal entry worksheet 1 2 3 Record the payment of cash dividend declared on December 1. Note: Enter debits before credits. Journal entry worksheet 1 2 3 4 5 9 Record the payment of $800,000 for construction of new cabins and other facilities. The entire expenditure is recorded in the Buildings account. Note: Enter debits before credits. Journal entry worksheet Record the entry to close the revenue accounts. Note: Enter debits before credits. Journal entry worksheet Record the entry to close the expense accounts. Note: Enter debits before credits. Journal entry worksheet Record the entry to close the dividends account. Note: Enter debits before credits. Gger Account \begin{tabular}{|c|c|c|c|c|} \hline \multicolumn{5}{|c|}{ Equipment } \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 62,000 \\ \hline \end{tabular} \begin{tabular}{|c|c|c|c|c|} \hline \multicolumn{5}{|c|}{ Accumulated Depreciation } \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 25,250 \\ \hline \end{tabular} \begin{tabular}{|r|c|c|r|r|} \hline \multicolumn{5}{|c|}{ Buildings } \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 0 \\ \hline \end{tabular} \begin{tabular}{|c|c|c|c|c|} \hline \multicolumn{1}{|c|}{ Accounts Payable } & \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 20,800 \\ \hline \end{tabular} \begin{tabular}{|c|c|c|c|c|} \hline \multicolumn{1}{|c|}{} & \multicolumn{5}{|c|}{ Income Tax Payable } \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 14,500 \\ \hline \end{tabular} \begin{tabular}{|r|c|c|c|c|} \hline \multicolumn{1}{|c|}{} & \multicolumn{2}{|c|}{ Deferred Revenue } & \\ \hline No. & Date & Deblt & Credit & Balance \\ \hline & November 05 & & & 5,000 \\ \hline \end{tabular} \begin{tabular}{|c|c|c|c|c|} \hline \multicolumn{5}{|c|}{ Notes Payable (Current) } \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 48,014 \\ \hline \end{tabular} \begin{tabular}{|c|c|c|c|c|||} \hline \multicolumn{4}{|c|}{ Notes Payable (Long-term) } & \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 475,869 \\ \hline \end{tabular} \begin{tabular}{|c|c|c|c|c|} \hline \multicolumn{4}{|c|}{ Contingent Liability } \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 12,000 \\ \hline \end{tabular} Retained Earnings \begin{tabular}{|c|c|c|c|c|} \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 33,450 \\ \hline \end{tabular} \begin{tabular}{|r|c|c|r|r|} \hline \multicolumn{4}{|c|}{ Dividends } \\ \hline No. & Date & Debit & Credit & \multicolumn{1}{|c|}{ Balance } \\ \hline & November 05 & & & 0 \\ \hline A & December 01 & 11,400 & & 11,400 \\ \hline \end{tabular} \begin{tabular}{|r|c|c|c|c|} \hline \multicolumn{5}{|c|}{ Service Revenue } \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 44,500 \\ \hline \end{tabular} \begin{tabular}{|r|c|c|c|c|} \hline \multicolumn{5}{|c|}{ Sales Revenue } \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 120,000 \\ \hline \end{tabular} \begin{tabular}{|r|c|c|c|r|} \hline \multicolumn{1}{|c|}{} & \multicolumn{3}{c|}{ Sales Discounts } \\ \hline \multicolumn{1}{|c|}{ Date } & Debit & Credit & Balance \\ \hline & November 05 & & & 350 \\ \hline \end{tabular} \begin{tabular}{|c|c|c|c|c|} \hline \multicolumn{1}{|c|}{ Interest Revenue } & \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 120 \\ \hline \end{tabular} \begin{tabular}{|r|c|c|c|r|} \hline \multicolumn{5}{|c|}{ Cost of Goods Sold } \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 38,500 \\ \hline \end{tabular} \begin{tabular}{|c|c|c|c|c|} \hline \multicolumn{5}{|c|}{ Supplies Expense } \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 500 \\ \hline \end{tabular} \begin{tabular}{|r|c|c|c|r|} \hline \multicolumn{5}{|c|}{ Bad Debt Expense } \\ \hline \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & Nowember 05 & & & 2.400 \\ \hline \end{tabular} \begin{tabular}{|c|c|c|c|c|} \hline \multicolumn{5}{|c|}{ Interest Expense } \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 6,785 \\ \hline \end{tabular} \begin{tabular}{|r|c|c|c|c|} \hline \multicolumn{5}{|c|}{ Income Tax Expense } \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 14,500 \\ \hline \end{tabular} \begin{tabular}{|c|c|c|c|c|} \hline \multicolumn{5}{|c|}{ Insurance Expense } \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 5,700 \\ \hline \end{tabular} General Journal Trial Balance > GREAT ADVENTURES, INCORPORATED Trial Balance December 30,2025 MTreasury Stock Addditional Paid-in Capital QRetained Earnings Dividends WService Revenue A Sales Revenue A Sales Discounts Winterest Revenue W.ost of Goods Sold Wepreciation Expense 2.Supplien Expense SSalarios Expense Aad Debt Expense thaterest Expense NRent Expense A income Tax Expense Winsurance Expense Wrepais and Maintonance Expense WWarranty Expense. AL.055 Total \begin{tabular}{|r|r|} \hline 90,000 & \\ \hline & 904,000 \\ \hline & 33,450 \\ \hline 11,400 & \\ \hline & 44,500 \\ \hline 350 & 120,000 \\ \hline & \\ \hline 38,500 & 120 \\ \hline 17,250 & \\ \hline 500 & \\ \hline 24,000 & \\ \hline 2,400 & \\ \hline 6,785 & \\ \hline 2,400 & \\ \hline 14,500 & \\ \hline 5,700 & \\ \hline 400 & \\ \hline 4,000 & \\ \hline 12,000 & \\ \hline 1,830,6535 \\ \hline \end{tabular} [1. Trial Balance Balance Sheet > | Unadjusted GREAT ADVENTURES, INCORPORATED Balance Sheet December 31,2025 RWP1U-1 (Static) Great Adventures Continuing Case (GL) Tony and Suzie have purchased land for a new camp. Now they need money to build the cabins, dining facility, a ropes course, and an outdoor swimming pool. Tony and Suzie first checked with Summit Bank to see if they could borrow an additional \$1 milion, but. unfortunately the bank turned them down as too risky. Undeterred, they promoted their idea to close friends they had made through the outdoor clinics and TEAM events. They decided to go ahead and sell shares of stock in the company to raise the additional funds for the camp. Great Adventures has authorized \$1 par value common stock. When the company began on July 1. 2024, Tony and Suzie each purchased 10,000 shares (20,000 shares totai) of \$1 par value common stock at $1 per share. The following transactions affect stockholders' equity during the remainder of 2025 . Hovenber 5 Issue an additional 100 , e00 shares of connon stock for 510 per share. Novertber 16 Purchase 10,000 shares of 1 ts oin coinon stock (1,e., preasury stock) for \$15, per share. Noveriber 24 Resel1 4,000 shares of treasury stock at \$16 per shara December 1 Declare a cosh dividend on 1ts compon stock of 511,400 (\$0.20 per share) to az1 stockholdees of icecord on Decenber 15. Deceaber 20 Pay the cosh dividend declared on Decenber 1. December 30 Pay 5800,000 for construction of new cobins and other foctlities. The entire Axpenditure if recorded In the fuidding account: in the first occount field.) Journal entry worksheet 789 Record the issue of additional 100,000 shares of common stock for $10 per share. Note: Enter debits before credits. Journal entry worksheet (7) 89 Record the purchase of 10,000 shares of its own common stock (i.e., treasury stock) for $15 per share. Note: Enter debits before credits. Journal entry worksheet 1 5 6 7 8 Record the resale of 4,000 shares of treasury stock at $16 per share. Note: Enter debits before credits. Journal entry worksheet 1 2 6 (7) 8 9 Record the declaration of $11,400 ( $0.10 per share) cash dividend on its common stock to all stockholders of record on December 15. Note: Enter debits before credits. Journal entry worksheet 1 2 6 Record the entry on December 15 , the date of record. Note: Enter debits before credits. Journal entry worksheet 1 2 3 Record the payment of cash dividend declared on December 1. Note: Enter debits before credits. Journal entry worksheet 1 2 3 4 5 9 Record the payment of $800,000 for construction of new cabins and other facilities. The entire expenditure is recorded in the Buildings account. Note: Enter debits before credits. Journal entry worksheet Record the entry to close the revenue accounts. Note: Enter debits before credits. Journal entry worksheet Record the entry to close the expense accounts. Note: Enter debits before credits. Journal entry worksheet Record the entry to close the dividends account. Note: Enter debits before credits. Gger Account \begin{tabular}{|c|c|c|c|c|} \hline \multicolumn{5}{|c|}{ Equipment } \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 62,000 \\ \hline \end{tabular} \begin{tabular}{|c|c|c|c|c|} \hline \multicolumn{5}{|c|}{ Accumulated Depreciation } \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 25,250 \\ \hline \end{tabular} \begin{tabular}{|r|c|c|r|r|} \hline \multicolumn{5}{|c|}{ Buildings } \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 0 \\ \hline \end{tabular} \begin{tabular}{|c|c|c|c|c|} \hline \multicolumn{1}{|c|}{ Accounts Payable } & \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 20,800 \\ \hline \end{tabular} \begin{tabular}{|c|c|c|c|c|} \hline \multicolumn{1}{|c|}{} & \multicolumn{5}{|c|}{ Income Tax Payable } \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 14,500 \\ \hline \end{tabular} \begin{tabular}{|r|c|c|c|c|} \hline \multicolumn{1}{|c|}{} & \multicolumn{2}{|c|}{ Deferred Revenue } & \\ \hline No. & Date & Deblt & Credit & Balance \\ \hline & November 05 & & & 5,000 \\ \hline \end{tabular} \begin{tabular}{|c|c|c|c|c|} \hline \multicolumn{5}{|c|}{ Notes Payable (Current) } \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 48,014 \\ \hline \end{tabular} \begin{tabular}{|c|c|c|c|c|||} \hline \multicolumn{4}{|c|}{ Notes Payable (Long-term) } & \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 475,869 \\ \hline \end{tabular} \begin{tabular}{|c|c|c|c|c|} \hline \multicolumn{4}{|c|}{ Contingent Liability } \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 12,000 \\ \hline \end{tabular} Retained Earnings \begin{tabular}{|c|c|c|c|c|} \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 33,450 \\ \hline \end{tabular} \begin{tabular}{|r|c|c|r|r|} \hline \multicolumn{4}{|c|}{ Dividends } \\ \hline No. & Date & Debit & Credit & \multicolumn{1}{|c|}{ Balance } \\ \hline & November 05 & & & 0 \\ \hline A & December 01 & 11,400 & & 11,400 \\ \hline \end{tabular} \begin{tabular}{|r|c|c|c|c|} \hline \multicolumn{5}{|c|}{ Service Revenue } \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 44,500 \\ \hline \end{tabular} \begin{tabular}{|r|c|c|c|c|} \hline \multicolumn{5}{|c|}{ Sales Revenue } \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 120,000 \\ \hline \end{tabular} \begin{tabular}{|r|c|c|c|r|} \hline \multicolumn{1}{|c|}{} & \multicolumn{3}{c|}{ Sales Discounts } \\ \hline \multicolumn{1}{|c|}{ Date } & Debit & Credit & Balance \\ \hline & November 05 & & & 350 \\ \hline \end{tabular} \begin{tabular}{|c|c|c|c|c|} \hline \multicolumn{1}{|c|}{ Interest Revenue } & \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 120 \\ \hline \end{tabular} \begin{tabular}{|r|c|c|c|r|} \hline \multicolumn{5}{|c|}{ Cost of Goods Sold } \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 38,500 \\ \hline \end{tabular} \begin{tabular}{|c|c|c|c|c|} \hline \multicolumn{5}{|c|}{ Supplies Expense } \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 500 \\ \hline \end{tabular} \begin{tabular}{|r|c|c|c|r|} \hline \multicolumn{5}{|c|}{ Bad Debt Expense } \\ \hline \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & Nowember 05 & & & 2.400 \\ \hline \end{tabular} \begin{tabular}{|c|c|c|c|c|} \hline \multicolumn{5}{|c|}{ Interest Expense } \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 6,785 \\ \hline \end{tabular} \begin{tabular}{|r|c|c|c|c|} \hline \multicolumn{5}{|c|}{ Income Tax Expense } \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 14,500 \\ \hline \end{tabular} \begin{tabular}{|c|c|c|c|c|} \hline \multicolumn{5}{|c|}{ Insurance Expense } \\ \hline No. & Date & Debit & Credit & Balance \\ \hline & November 05 & & & 5,700 \\ \hline \end{tabular} General Journal Trial Balance > GREAT ADVENTURES, INCORPORATED Trial Balance December 30,2025 MTreasury Stock Addditional Paid-in Capital QRetained Earnings Dividends WService Revenue A Sales Revenue A Sales Discounts Winterest Revenue W.ost of Goods Sold Wepreciation Expense 2.Supplien Expense SSalarios Expense Aad Debt Expense thaterest Expense NRent Expense A income Tax Expense Winsurance Expense Wrepais and Maintonance Expense WWarranty Expense. AL.055 Total \begin{tabular}{|r|r|} \hline 90,000 & \\ \hline & 904,000 \\ \hline & 33,450 \\ \hline 11,400 & \\ \hline & 44,500 \\ \hline 350 & 120,000 \\ \hline & \\ \hline 38,500 & 120 \\ \hline 17,250 & \\ \hline 500 & \\ \hline 24,000 & \\ \hline 2,400 & \\ \hline 6,785 & \\ \hline 2,400 & \\ \hline 14,500 & \\ \hline 5,700 & \\ \hline 400 & \\ \hline 4,000 & \\ \hline 12,000 & \\ \hline 1,830,6535 \\ \hline \end{tabular} [1. Trial Balance Balance Sheet > | Unadjusted GREAT ADVENTURES, INCORPORATED Balance Sheet December 31,2025 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Labor Economics

Authors: Campbell McConnell, Stanley Brue, David Macpherson

9th Edition

0073375950, 9780073375953