Help:

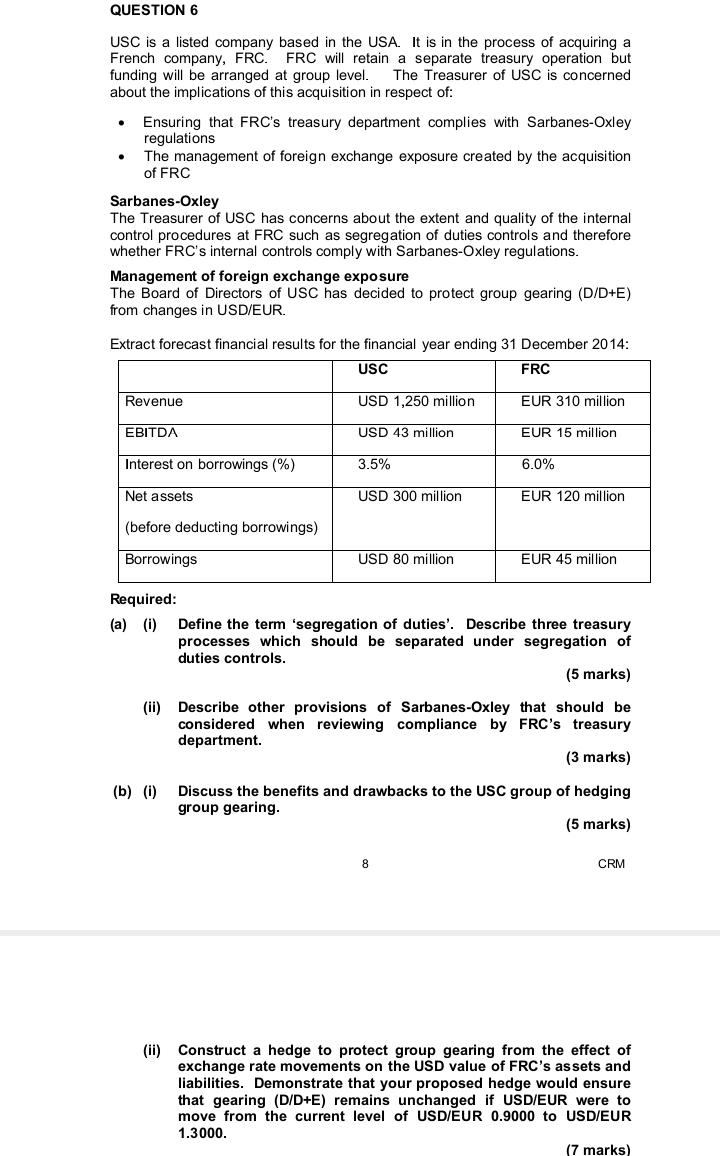

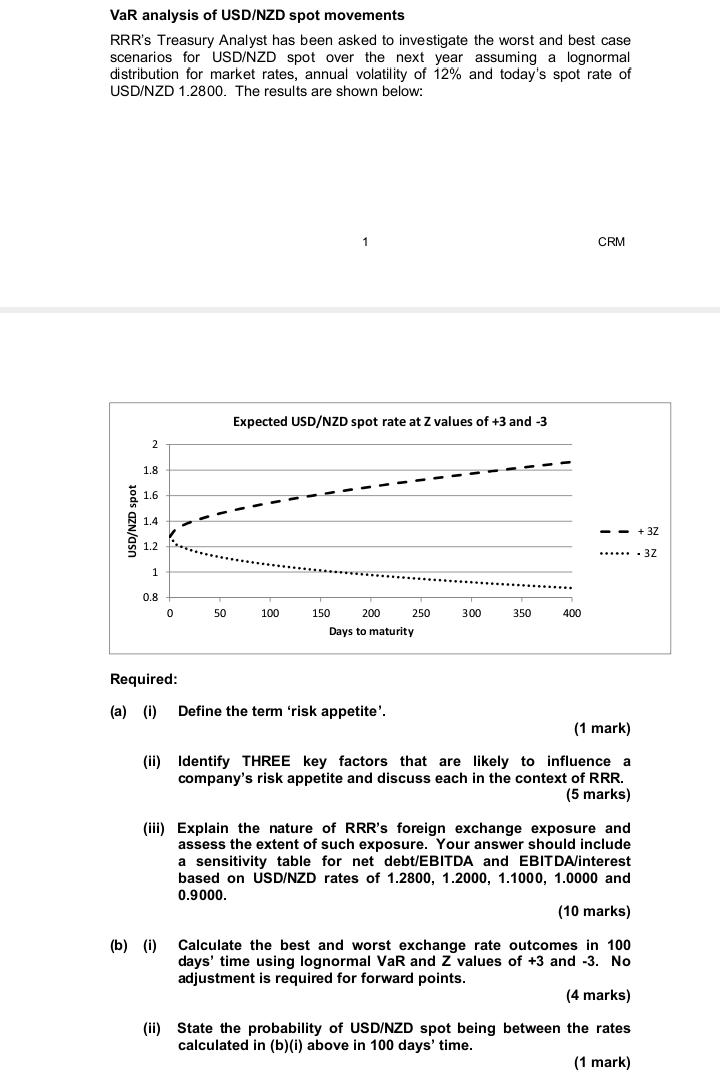

QUESTION 6 USC is a listed company based in the USA. It is in the process of acquiring a French company, FRC. FRC will retain a separate treasury operation but funding will be arranged at group level. The Treasurer of USC is concerned about the implications of this acquisition in respect of: . Ensuring that FRC's treasury department complies with Sarbanes-Oxley regulations The management of foreign exchange exposure created by the acquisition of FRC Sarbanes-Oxley The Treasurer of USC has concerns about the extent and quality of the internal control procedures at FRC such as segregation of duties controls and therefore whether FRC's internal controls comply with Sarbanes-Oxley regulations. Management of foreign exchange exposure The Board of Directors of USC has decided to protect group gearing (D/D+E) from changes in USD/EUR. Extract forecast financial results for the financial year ending 31 December 2014: USC FRC Revenue USD 1,250 million EUR 310 million EBITDA USD 43 million EUR 15 million Interest on borrowings (%) 3.5% 6.0% Net assets USD 300 million EUR 120 million (before deducting borrowings) Borrowings USD 80 million EUR 45 million Required: (a) (i) Define the term 'segregation of duties'. Describe three treasury processes which should be separated under segregation of duties controls. (5 marks) (ii) Describe other provisions of Sarbanes-Oxley that should be considered when reviewing compliance by FRC's treasury department. (3 marks) (b) (i) Discuss the benefits and drawbacks to the USC group of hedging group gearing. (5 marks) CO CRM (ii) Construct a hedge to protect group gearing from the effect of exchange rate movements on the USD value of FRC's assets and liabilities. Demonstrate that your proposed hedge would ensure that gearing (D/D+E) remains unchanged if USD/EUR were to move from the current level of USD/EUR 0.9000 to USD/EUR 1.3000. marks)3. Growth and Natural Resources (10 points). In November 2007, Brazil's state-controlled oil company Petrobras announced that they have discovered new and significant oil reserves in the Tupi oilfield off the coast of Brazil. Given current estimates, Brazil could join the world's "top 10" oil producers. At the time of the discovery, Petrobras President Sergio Gabrielli said that these discoveries would give Brazil the world's eighth-largest oil and gas reserves. "Brazil's reserves will lie somewhere between those of Nigeria and those of Venezuela," Gabrielli said at a news conference. Assume that the reserves are indeed "extractable" and the estimates are right. This sudden increase in nation's wealth will now allow Brazil to grow fast and become a rich country. Evaluate this statement and provide evidence to support your argument. Are there arguments in the opposite direction?7 Exercise 6.3 We consider two types of call arrivals to a cell in a mobile telephone network: new calls that originate in a cell and calls that are handed over from neighboring cells. It is desirable to give preference to handover calls over new calls. For this reason, some of the channels in the cell are reserved for handover calls, while the rest of the channels are available to both types of calls. For the questions below, assume the following: Channels in the cell are held for two minutes on average, with exponential distribution. All calls arrive according to a Poisson process with rie An, = 125 calls per hour for new calls, and Apo = 50 calls per hour for handover calls. The cell has a capacity of 10 channels; each call occupies I channel. I. Draw a state diagram of the channel occupancy in a cell when 2 channels are used exclusively for handover calls. 2. Calculate the Mocking probability in the cell if no channels are reserved for handover calls. What is the average number of channels used? 3. Find the minimum number of channels reserved for handover calls so that their blocking probability is below I percent. What is the blocking probabil- ity for the new calls in this case?VaR analysis of USD/NZD spot movements RRR's Treasury Analyst has been asked to investigate the worst and best case scenarios for USD/NZD spot over the next year assuming a lognormal distribution for market rates, annual volatility of 12% and today's spot rate of USD/NZD 1.2800. The results are shown below: CRM Expected USD/NZD spot rate at Z values of +3 and -3 1.8 USD/NZD spot 1.4 - + 32 1.2 . . .... .32 ........ 0 50 100 150 200 250 300 350 400 Days to maturity Required: (a) (i) Define the term 'risk appetite'. (1 mark) ii) Identify THREE key factors that are likely to influence a company's risk appetite and discuss each in the context of RRR. (5 marks) (iii) Explain the nature of RRR's foreign exchange exposure and assess the extent of such exposure. Your answer should include a sensitivity table for net debt/EBITDA and EBITDA/interest based on USD/NZD rates of 1.2800, 1.2000, 1.1000, 1.0000 and 0.9000. (10 marks) (b) (1) Calculate the best and worst exchange rate outcomes in 100 days' time using lognormal VaR and Z values of +3 and -3. No adjustment is required for forward points. (4 marks) (ii) State the probability of USD/NZD spot being between the rates calculated in (b)(i) above in 100 days' time. (1 mark)