Answered step by step

Verified Expert Solution

Question

1 Approved Answer

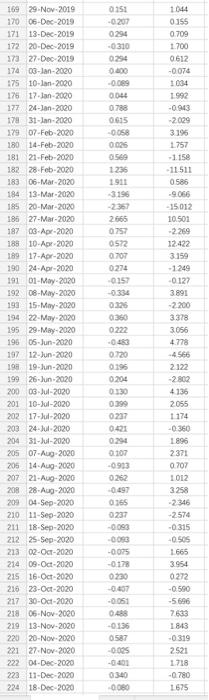

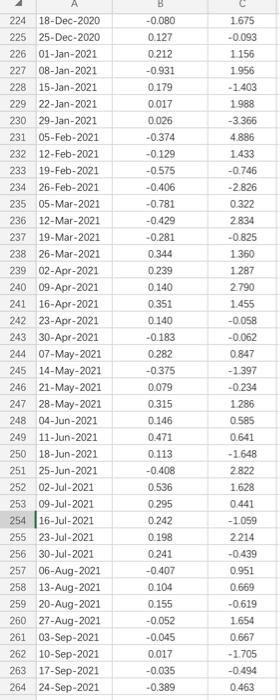

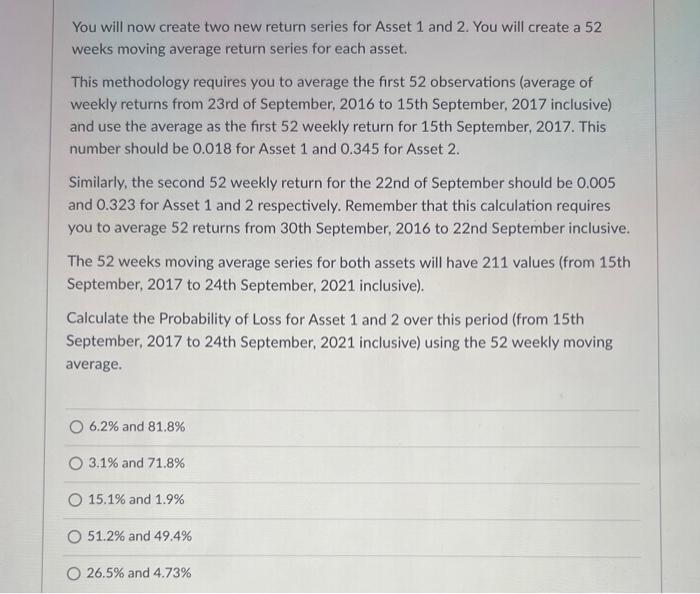

help You will now create two new return series for Asset 1 and 2 . You will create a 52 weeks moving average return series

help

You will now create two new return series for Asset 1 and 2 . You will create a 52 weeks moving average return series for each asset. This methodology requires you to average the first 52 observations (average of weekly returns from 23rd of September, 2016 to 15 th September, 2017 inclusive) and use the average as the first 52 weekly return for 15 th September, 2017. This number should be 0.018 for Asset 1 and 0.345 for Asset 2 . Similarly, the second 52 weekly return for the 22 nd of September should be 0.005 and 0.323 for Asset 1 and 2 respectively. Remember that this calculation requires you to average 52 returns from 30 th September, 2016 to 22 nd September inclusive. The 52 weeks moving average series for both assets will have 211 values (from 15 th September, 2017 to 24 th September, 2021 inclusive). Calculate the Probability of Loss for Asset 1 and 2 over this period (from 15 th September, 2017 to 24 th September, 2021 inclusive) using the 52 weekly moving average. 6.2% and 81.8% 3.1% and 71.8% 15.1% and 1.9% 51.2% and 49.4% 26.5% and 4.73% You will now create two new return series for Asset 1 and 2 . You will create a 52 weeks moving average return series for each asset. This methodology requires you to average the first 52 observations (average of weekly returns from 23rd of September, 2016 to 15 th September, 2017 inclusive) and use the average as the first 52 weekly return for 15 th September, 2017. This number should be 0.018 for Asset 1 and 0.345 for Asset 2 . Similarly, the second 52 weekly return for the 22 nd of September should be 0.005 and 0.323 for Asset 1 and 2 respectively. Remember that this calculation requires you to average 52 returns from 30 th September, 2016 to 22 nd September inclusive. The 52 weeks moving average series for both assets will have 211 values (from 15 th September, 2017 to 24 th September, 2021 inclusive). Calculate the Probability of Loss for Asset 1 and 2 over this period (from 15 th September, 2017 to 24 th September, 2021 inclusive) using the 52 weekly moving average. 6.2% and 81.8% 3.1% and 71.8% 15.1% and 1.9% 51.2% and 49.4% 26.5% and 4.73% Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

A Fast And Frugal Finance

Authors: William P. Forbes, Aloysius Igboekwu, Shabnam Mousavi

1st Edition

0128124954, 978-0128124956