Help????thanks

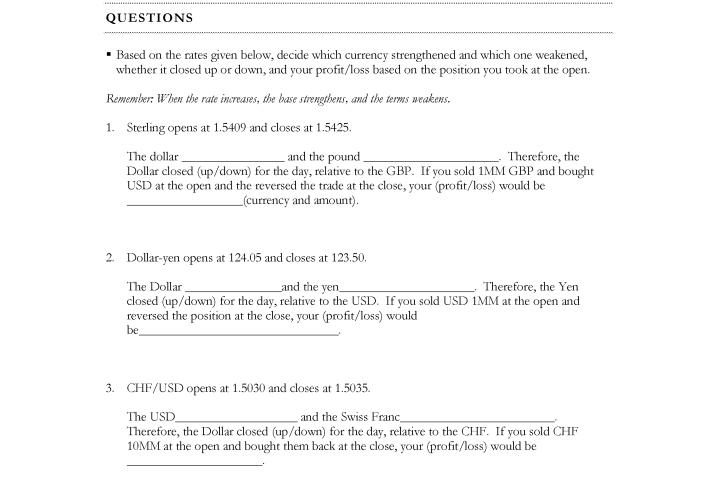

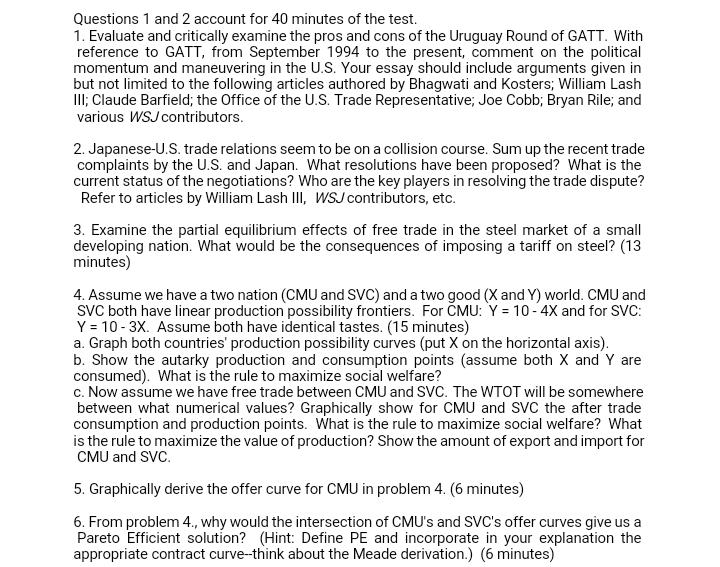

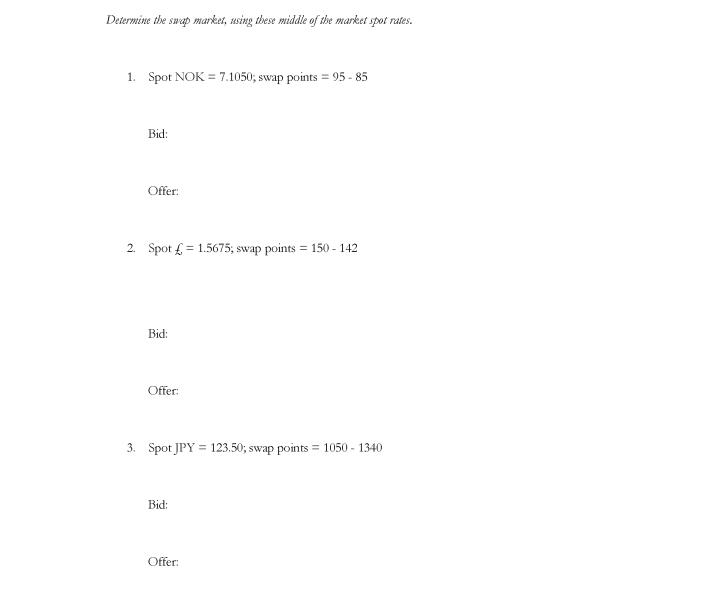

Q1. In what way does a fixed-for-fixed currency swap differ from a spot contract and a reverseQUESTIONS " Based on the rates given below, decide which currency strengthened and which one weakened, whether it closed up or down, and your profit/loss based on the position you took at the open. Remember: When the rate increases, the base strengthens, and the terms weakens. 1. Sterling opens at 1.5409 and closes at 1.5425. The dollar and the pound Therefore, the Dollar closed (up/down) for the day, relative to the GBP. If you sold 1MM GBP and bought USD at the open and the reversed the trade at the close, your (profit/loss) would be (currency and amount). 2. Dollar-yen opens at 124.05 and closes at 123.50, The Dollar and the yen Therefore, the Yen closed (up/down) for the day, relative to the USD. If you sold USD 1MM at the open and reversed the position at the close, your (profit/loss) would be 3. CHF/USD opens at 1.5030 and closes at 1.5035. The USD and the Swiss Franc Therefore, the Dollar closed (up/down) for the day, relative to the CHF. If you sold CHE 10MM at the open and bought them back at the close, your (profit/loss) would beQuestions 1 and 2 account for 4G minutes of the test. 1. Evaluate and critically examine the pros and cons of the Uruguay Round of GATT. With reference to GATT. from September 1994 to the present. comment on the political momentum and maneuvering in the US. Your essay should include arguments given in but not limited to the following articles authored by Bhagwati and Rosters; William Lash Ill; Claude Earfield; the Office of the US. Trade Representative; Joe Cobb; Bryan Rile; and various WSJcontributors. 2. Japanese-US. trade relations seem to be on a collision course. Sum up the recent trade complaints by the U3. and Japan. What resolutions have been proposed? What is the current status of the negotiations? Who are the key players in resolving the trade dispute? Refer to articles by William Lash lll. WSJcontributors. etc. 3. Examine the partial equilibrium effects of free trade in the steel market of a small developing nation. What would be the consequences of imposing a tariff on steel? [13 minutes] 4. Assume we have a two nation [GMU and SEC] and a two good {X and Y} world. GMU and ENG both have linear production possibility frontiers. For GMU: 'f = 1 El 4K and for SVG: '1!" = if] 3X. Assume both have identical tastes. {15 minutes} a. Graph both countries' production possibility curves {put it on the horizontal axis}. b. Show the autarlcy production and consumption points {assume both I and 'f are consumed}. What is the rule to maximize social welfare? c. Now assume we have free trade between GMU and S'v'G. The WTDT will be somewhere between what numerical values? Graphically show for lelU and S'v'G the after trade consumption and production points. What is the rule to maximize social welfare? What is the rule to maximize the value of production? Show the amount of export and import for GMU and SW3. 5. Graphically derive the offer curve for GMU in problem 4. [E minutes) 6. From problem 4.. why would the intersection of GMU's and S'v'G's offer curves give us a Pareto Efficient solution? (Hint: Define PE and incorporate in your explanation the appropriate contract curchthink about the lvleade derivation.) (6 minutes} E1. You are an A quality borrower, and you pay 10 percent on a five-year loan with one final amortization at the end. This is 1 percent above the spread paid by an AAA borrower. What will be the up-front fee for which your bank should be willing to lower the rate by 1 percent?A5. Using the effective spot returns computed in ME4, the yields are found from: 1 - 1/(1 + 7) E 1Determine the swap market, using these middle of the market spot rates. 1. Spot NOK = 7.1050; swap points = 95 - 85 Bid: Offer: 2. Spot { = 1.5675; swap points = 150 - 142 Bid: Offer: 3. Spot JPY = 123.50; swap points = 1050 - 1340 Bid: Offer:ME7. With the same data, verify how well (or how badly) the value of an n-year annuity ( = 1,....5) is approximated when one uses the five-year yield at par of a bullet bond rather than the complete term structure of spot returns