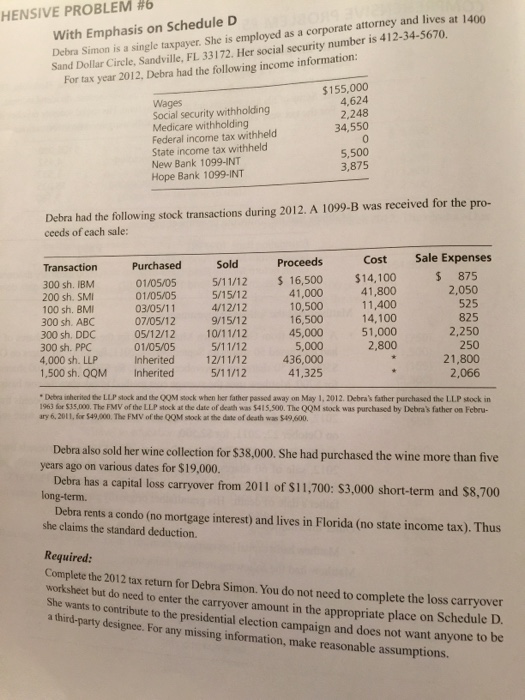

HENSIVE PROBLEM #6 at 1400 With Emphasis on Schedule D attorney and lives Debra Simon is a single taxpayer. She is employed as a corporate is Sand Dollar Circle, Sandville, 33172. Her social security number For tax year 2012. Debra had the following income information: $155,000 4,624 Wages withholding Social Security 2,248 Medicare withholding 34,550 Federal income tax withheld State income tax withheld 5,500 New Bank 1099-INT 3,875 Hope Bank 1099-INT Debra had the following stock transactions during 2012. A 1099-B was received for the pro- ceeds of each sale: Cost Sale Expenses Proceed Transaction Purchased Sold 875 $14,100 16,500 01/05/05 300 sh. IBM 2,050 41,800 41,000 5/15/12 01/05/05 200 sh, SM 525 11,400 10,500 4/12/12 100 sh. BMI 03/05/11 825 14,100 16,500 9/15/12 07/05/12 300 sh, ABC 2,250 51,000 300 sh, DDC 45,000 10/11/12 01/05/05 5/11/12 250 2,800 300 sh. PPC 21,800 4,000 sh. LLP Inherited 12/11/12 436,000 1,500 sh. QQM inherited 41,325 2,066 Debra inherited the LLP stock and the QOM sock when her father passed away on May 2012. Debra's father purchased the LLP stock in 963 for s35.000. The FMV of the LLP stock at the date of death was s415.500. The QQM stock was purchased by Debra's father on Febru- ary 6, 2011, for 49,000. The FMV of the QM stock at the date of death was Debra also sold her wine collection for s38,000. She had purchased the wine more than five years ago on various dates for $19,000. Debra has a capital loss carryover from 2011 of si1700: s3,000 short-term and s8,700 long-term Debra rents a condo (no mortgage interest) and lives in Florida (no state income tax).Thus she claims the standard deduction. equired: Complete the 2012 tax return for Debra Simon You do not need to complete the loss carryover She wants but do need to enter the carryover amount in the appropriate place on Schedule D. to contribute to the presidential election campaign and does not want anyone to be third-party designee. For any missing information, make reasonable assumptions. HENSIVE PROBLEM #6 at 1400 With Emphasis on Schedule D attorney and lives Debra Simon is a single taxpayer. She is employed as a corporate is Sand Dollar Circle, Sandville, 33172. Her social security number For tax year 2012. Debra had the following income information: $155,000 4,624 Wages withholding Social Security 2,248 Medicare withholding 34,550 Federal income tax withheld State income tax withheld 5,500 New Bank 1099-INT 3,875 Hope Bank 1099-INT Debra had the following stock transactions during 2012. A 1099-B was received for the pro- ceeds of each sale: Cost Sale Expenses Proceed Transaction Purchased Sold 875 $14,100 16,500 01/05/05 300 sh. IBM 2,050 41,800 41,000 5/15/12 01/05/05 200 sh, SM 525 11,400 10,500 4/12/12 100 sh. BMI 03/05/11 825 14,100 16,500 9/15/12 07/05/12 300 sh, ABC 2,250 51,000 300 sh, DDC 45,000 10/11/12 01/05/05 5/11/12 250 2,800 300 sh. PPC 21,800 4,000 sh. LLP Inherited 12/11/12 436,000 1,500 sh. QQM inherited 41,325 2,066 Debra inherited the LLP stock and the QOM sock when her father passed away on May 2012. Debra's father purchased the LLP stock in 963 for s35.000. The FMV of the LLP stock at the date of death was s415.500. The QQM stock was purchased by Debra's father on Febru- ary 6, 2011, for 49,000. The FMV of the QM stock at the date of death was Debra also sold her wine collection for s38,000. She had purchased the wine more than five years ago on various dates for $19,000. Debra has a capital loss carryover from 2011 of si1700: s3,000 short-term and s8,700 long-term Debra rents a condo (no mortgage interest) and lives in Florida (no state income tax).Thus she claims the standard deduction. equired: Complete the 2012 tax return for Debra Simon You do not need to complete the loss carryover She wants but do need to enter the carryover amount in the appropriate place on Schedule D. to contribute to the presidential election campaign and does not want anyone to be third-party designee. For any missing information, make reasonable assumptions