Here are the client situation and format examples of the file memo. Please provide an answer, what the client is able to write off, and under what section code. . I also attach one similar answer example.

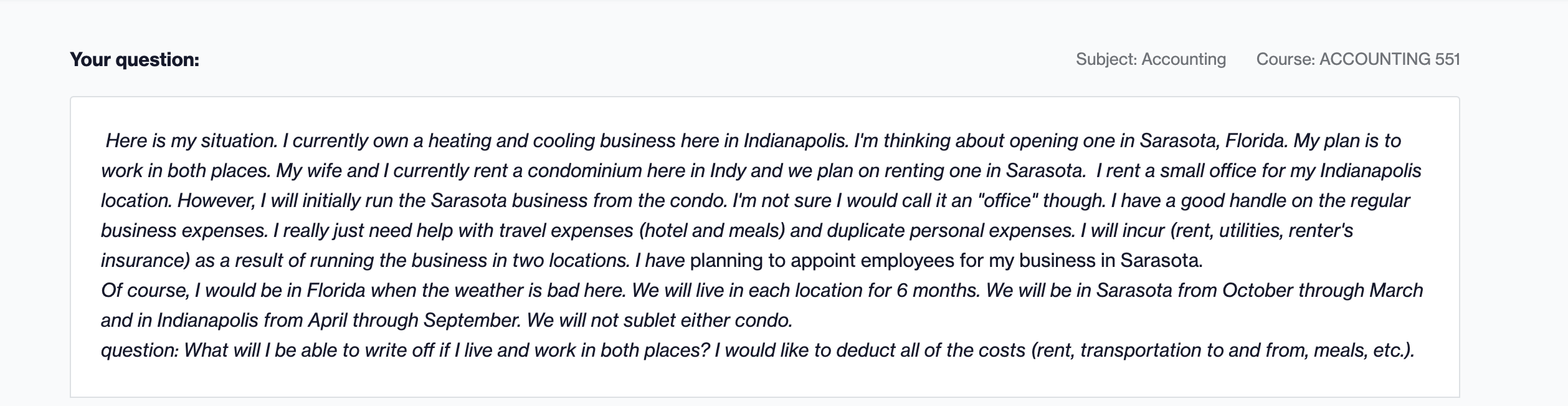

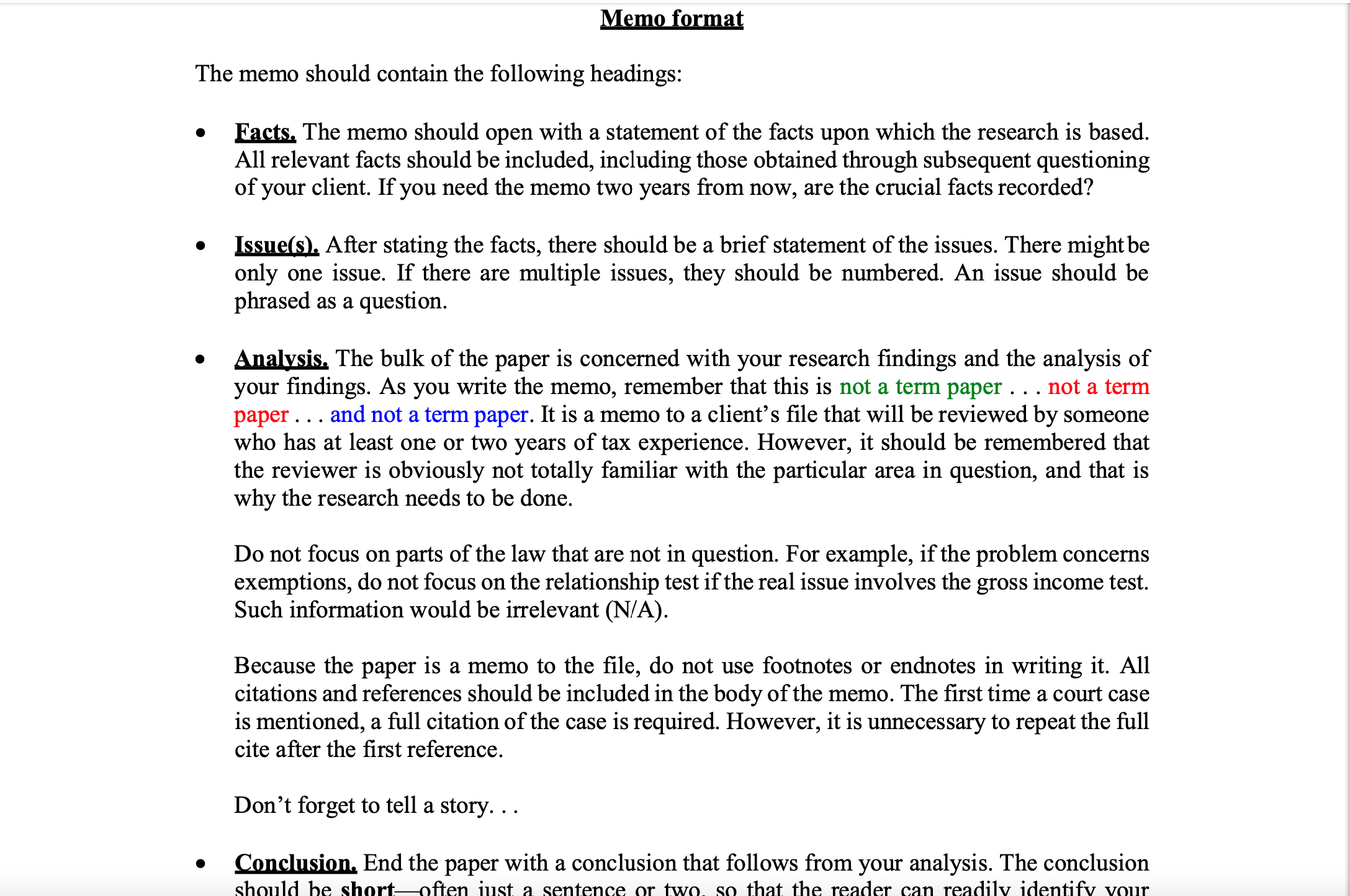

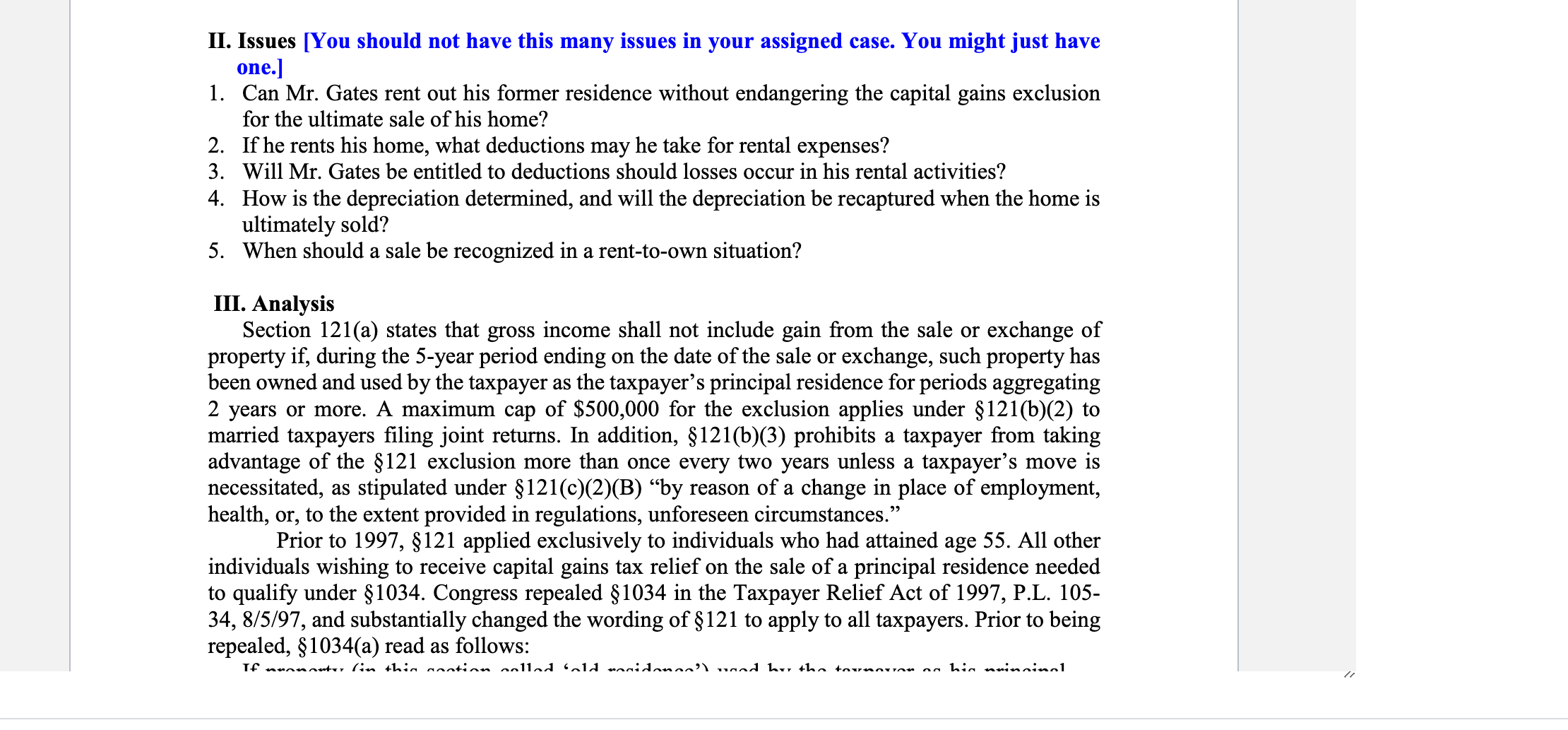

Your question: Subject: Accounting Course: ACCOUNTING 551 Here is my situation. I currently own a heating and cooling business here In Indianapolis. I'm thinking about opening one in Sarasota, Florida. My plan is to work in both places. My wife and I currently rent a condominium here in Indy and we plan on renting one in Sarasota. Irent a small ofce for my Indianapolis location. However, I will initially run the Sarasota business from the condo. I'm not sure I would call it an "office" though. I have a good handle on the regular business expenses. I really just need help with travel expenses (hotel and meals) and duplicate personal expenses. I will incur (rent, utilities, renter's insurance) as a result of running the business in two locations. [have planning to appoint employees for my business in Sarasota. Of course, I would be in Florida when the weather is bad here. We will live in each location for 6 months. We will be in Sarasota from October through March and in Indianapolis from April through September. We will not sublet either condo. question: What will I be able to write off if I live and work in both places? I would like to deduct all of the costs (rent, transportation to and from, meals, etc.). Memo format The memo should contain the following headings: . Facts. The memo should open with a statement of the facts upon which the research is based. All relevant facts should be included, including those obtained through subsequent questioning of your client. If you need the memo two years from now, are the crucial facts recorded? . Issue(s). After stating the facts, there should be a brief statement of the issues. There might be only one issue. If there are multiple issues, they should be numbered. An issue should be phrased as a question. Analysis. The bulk of the paper is concerned with your research findings and the analysis of your findings. As you write the memo, remember that this is not a term paper . . . not a term paper . . . and not a term paper. It is a memo to a client's file that will be reviewed by someone who has at least one or two years of tax experience. However, it should be remembered that the reviewer is obviously not totally familiar with the particular area in question, and that is why the research needs to be done. Do not focus on parts of the law that are not in question. For example, if the problem concerns exemptions, do not focus on the relationship test if the real issue involves the gross income test. Such information would be irrelevant (N/A). Because the paper is a memo to the file, do not use footnotes or endnotes in writing it. All citations and references should be included in the body of the memo. The first time a court case is mentioned, a full citation of the case is required. However, it is unnecessary to repeat the full cite after the first reference. Don't forget to tell a story. . . . Conclusion. End the paper with a conclusion that follows from your analysis. The conclusion should be short ften just a sentence or two. so that the reader can r readily identify vour11. Issues [You should not have this many issues in your assigned case. You might just have one.] 1. Can Mr. Gates rent out his former residence without endangering the capital gains exclusion for the ultimate sale of his home? 2. If he rents his home, what deductions may he take for rental expenses? 3. Will Mr. Gates be entitled to deductions should losses occur in his rental activities? 4. How is the depreciation determined, and will the depreciation be recaptured when the home is ultimately sold? 5. When should a sale be recognized in a rent-toown situation? III. Analysis Section 121(a) states that gross income shall not include gain from the sale or exchange of property if, during the 5-year period ending on the date of the sale or exchange, such property has been owned and used by the taxpayer as the taxpayer's principal residence for periods aggregating 2 years or more. A maximum cap of $500,000 for the exclusion applies under 121(b)(2) to married taxpayers ling joint returns. In addition, 121(b)(3) prohibits a taxpayer from taking advantage of the 121 exclusion more than once every two years unless a taxpayer's move is necessitated, as stipulated under 121(c)(2)(B) \"by reason of a change in place of employment, health, or, to the extent provided in regulations, unforeseen circumstances.\" Prior to 1997, 121 applied exclusively to individuals who had attained age 55. All other individuals wishing to receive capital gains tax relief on the sale of a principal residence needed to qualify under 1034. Congress repealed 1034 in the Taxpayer Relief Act of 1997, PL. 105- 34, 8/5/97, and substantially changed the wording of 121 to apply to all taxpayers. Prior to being repealed, 1034(a) read as follows: YJ.' _-n_,..4" (1,. cLln "Aclnu Annall 'n'lA An:tlann'\\ \"AAA 1.... c1... \"nAn,\" AA L1,. ':n:n1 //