Answered step by step

Verified Expert Solution

Question

1 Approved Answer

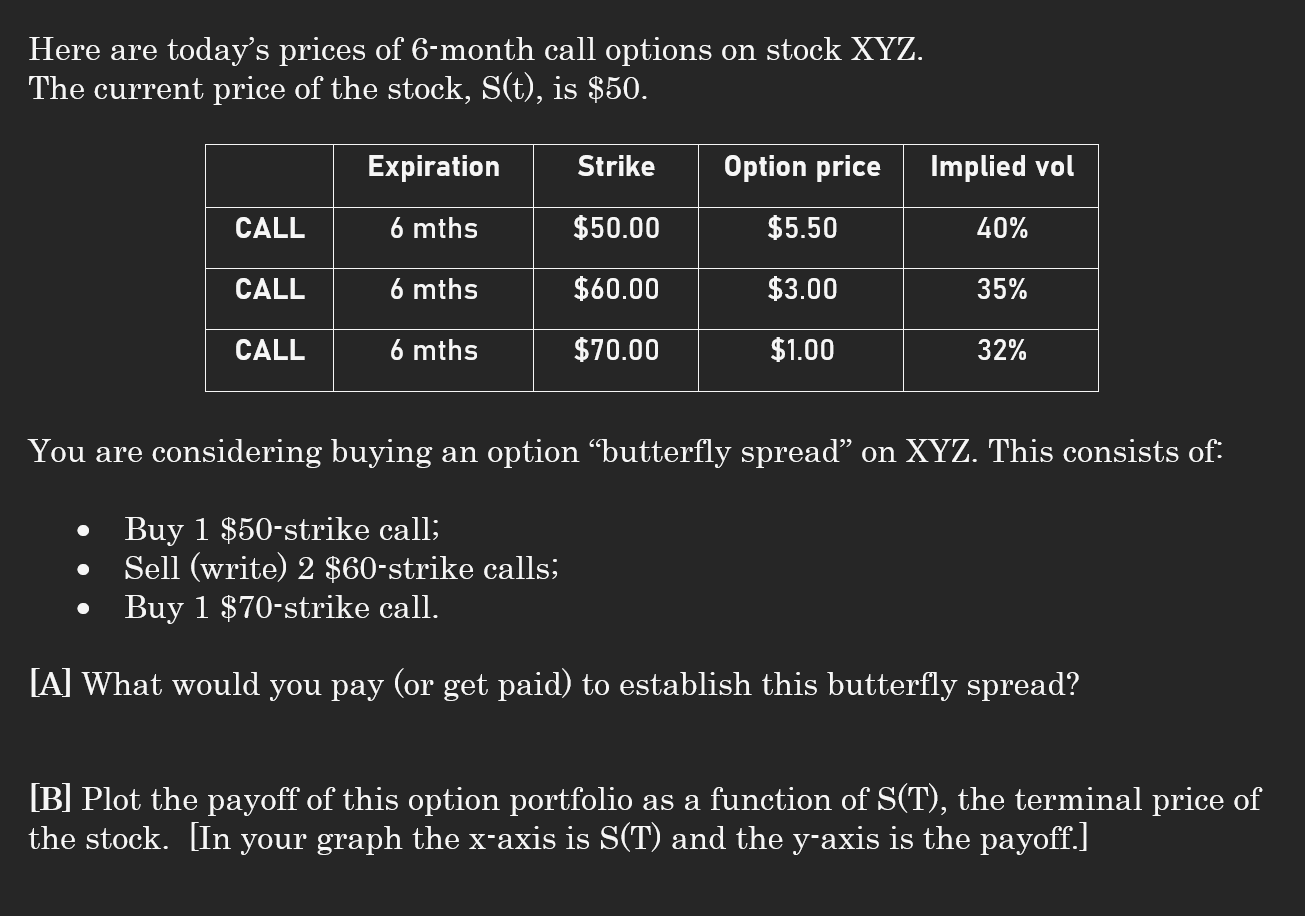

Here are today's prices of 6-month call options on stock XYZ. The current price of the stock, S(t), is $50. CALL CALL CALL Expiration

Here are today's prices of 6-month call options on stock XYZ. The current price of the stock, S(t), is $50. CALL CALL CALL Expiration 6 mths 6 mths 6 mths Strike $50.00 $60.00 $70.00 Option price $5.50 $3.00 $1.00 Implied vol 40% 35% 32% You are considering buying an option butterfly spread on XYZ. This consists of: Buy 1 $50-strike call; Sell (write) 2 $60-strike calls; Buy 1 $70-strike call. [A] What would you pay (or get paid) to establish this butterfly spread? [B] Plot the payoff of this option portfolio as a function of S(T), the terminal price of the stock. [In your graph the x-axis is S(T) and the y-axis is the payoff.]

Step by Step Solution

★★★★★

3.45 Rating (152 Votes )

There are 3 Steps involved in it

Step: 1

To determine the cost or ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Corporate Finance

Authors: Jonathan Berk, Peter DeMarzo, Jarrad Harford

5th Edition

0135811600, 978-0135811603