here he the first picture again

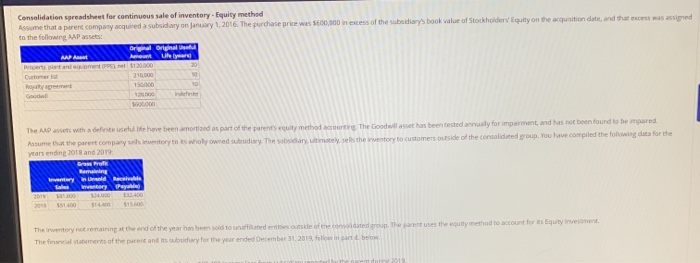

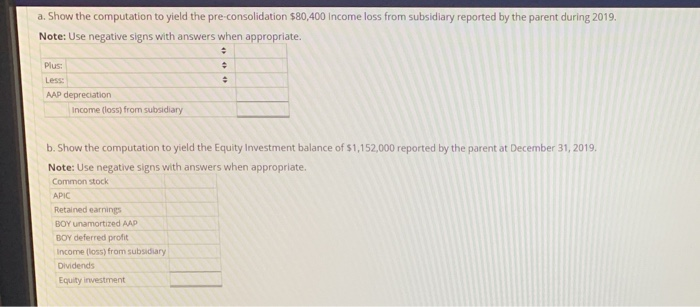

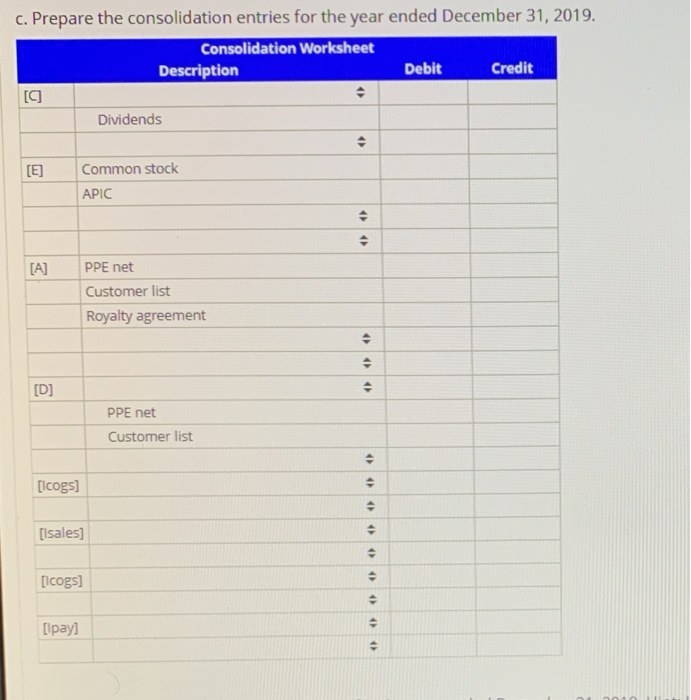

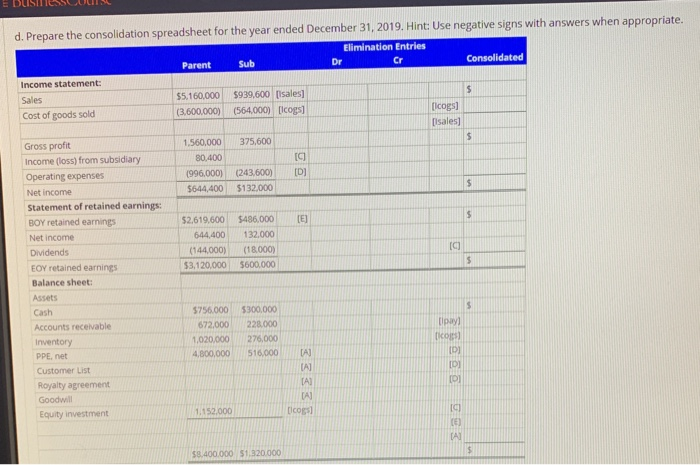

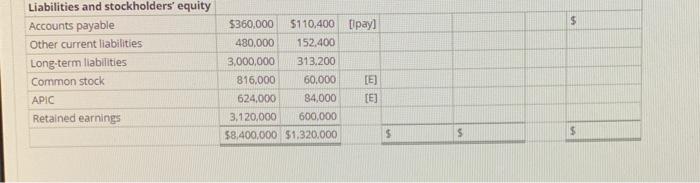

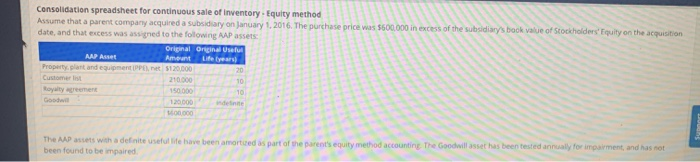

Consolidation spreadsheet for continuous sale of inventory. Equity method Assume that a parent company acquired a subsidiary on January 1, 2016. The purchase price was 5600,000 in excess of the subsidiary's book value of Stockholders' Equity on the acquisition date, and that was assigned to the following AAP assets: Original Originals ANA Aument Decerts and emot5120000 Duru 210.000 Hoyage 12000 nostres The Davies with a dere su Te have been amortized as part of the parents culty method accounting The Goodwill asset has been tested annually for imparment, and has not been found to be mpared Assume that the parent company will inventory to Es wholly owned subsidiary. The sadary, ultimately, sels the inventory to customers outside of the consolidated group. You have compiled the following data for the years endine 2018 and 2019 Bra Prete Wyld Reale 2018 The inwertery not remaining at the end of the year has been said to unitedde of the conted group. The uses the equity method to account for its Equity Investment The filaments of the parent and its subsidiary for the year ended December 31, 2019 folie in arte a. Show the computation to yield the pre-consolidation $80,400 Income loss from subsidiary reported by the parent during 2019. Note: Use negative signs with answers when appropriate. Plus: Less: AAP depreciation Income (loss) from subsidiary b. Show the computation to yield the Equity Investment balance of 1,152,000 reported by the parent at December 31, 2019. Note: Use negative signs with answers when appropriate. Common stock APIC Retained earnings BOY un amortized AAD BOY deferred profit Income (loss) from subsidiary Dividends Equity investment C. Prepare the consolidation entries for the year ended December 31, 2019. Consolidation Worksheet Description Debit Credit [C Dividends [E] Common stock APIC [A] PPE net Customer list Royalty agreement > [D] PPE net Customer list [lcogs] [lsales] . e [lcogs] 4) [lpay] d. Prepare the consolidation spreadsheet for the year ended December 31, 2019. Hint: Use negative signs with answers when appropriate. Elimination Entries Dr Cr Consolidated Parent Sub Income statement: Sales Cost of goods sold $5.160,000 (3.600.000) $939,600 (sales (564,000) [icogs $ [Icogs] [sales) $ 375,600 [C] 1,560,000 80,400 1996,000) $644,400 (D) (243,600) $132.000 $ $ [E] $2.619,600 644,400 (144,000) $3,120.000 $486.000 132,000 (18.000) 5600.000 IC) $ Gross profit Income (loss) from subsidiary Operating expenses Net income Statement of retained earnings: BOY retained earnings Net income Dividends EOY retained earnings Balance sheet: Assets Cash Accounts receivable Inventory PPE, net Customer List Royalty agreement Goodwill Equity investment $ 5756.000 672,000 1,020,000 4,800,000 5300,000 228.000 276.000 516.000 3333 ) fico) DI IDI 0 1.152.000 Dicope 19 CE) [A $ $8.400.000 511320.000 $ Liabilities and stockholders' equity Accounts payable Other current liabilities Long-term liabilities Common stock APIC Retained earnings $360,000 $110,400 Upayl 480,000 152,400 3,000,000 313,200 816.000 60,000 [E] 624,000 84,000 [E] 3,120,000 600,000 $8,400,000 $1.320.000 $ $ $ Consolidation spreadsheet for continuous sale of Inventory. Equity method Assume that a parent company acquired a subsidiary on January 1, 2016. The purchase price was $600.000 in excess of the subsidiary's book value of Stockholders' Equity on the acquisition date, and that excess was assigned to the following AAP assets: Original Original Useful AAP Anet Amount Life Cars Property plant and equipment Pret 5120.000 20 Customer 210.000 10 Royalty freement 10 Good 120.000 The AP assets with a defnite useful life have been amortured as part of the parent's equity method accounting The Goodwill asset has been tested annually for impairment, and has not been found to be paired Consolidation spreadsheet for continuous sale of inventory. Equity method Assume that a parent company acquired a subsidiary on January 1, 2016. The purchase price was 5600,000 in excess of the subsidiary's book value of Stockholders' Equity on the acquisition date, and that was assigned to the following AAP assets: Original Originals ANA Aument Decerts and emot5120000 Duru 210.000 Hoyage 12000 nostres The Davies with a dere su Te have been amortized as part of the parents culty method accounting The Goodwill asset has been tested annually for imparment, and has not been found to be mpared Assume that the parent company will inventory to Es wholly owned subsidiary. The sadary, ultimately, sels the inventory to customers outside of the consolidated group. You have compiled the following data for the years endine 2018 and 2019 Bra Prete Wyld Reale 2018 The inwertery not remaining at the end of the year has been said to unitedde of the conted group. The uses the equity method to account for its Equity Investment The filaments of the parent and its subsidiary for the year ended December 31, 2019 folie in arte a. Show the computation to yield the pre-consolidation $80,400 Income loss from subsidiary reported by the parent during 2019. Note: Use negative signs with answers when appropriate. Plus: Less: AAP depreciation Income (loss) from subsidiary b. Show the computation to yield the Equity Investment balance of 1,152,000 reported by the parent at December 31, 2019. Note: Use negative signs with answers when appropriate. Common stock APIC Retained earnings BOY un amortized AAD BOY deferred profit Income (loss) from subsidiary Dividends Equity investment C. Prepare the consolidation entries for the year ended December 31, 2019. Consolidation Worksheet Description Debit Credit [C Dividends [E] Common stock APIC [A] PPE net Customer list Royalty agreement > [D] PPE net Customer list [lcogs] [lsales] . e [lcogs] 4) [lpay] d. Prepare the consolidation spreadsheet for the year ended December 31, 2019. Hint: Use negative signs with answers when appropriate. Elimination Entries Dr Cr Consolidated Parent Sub Income statement: Sales Cost of goods sold $5.160,000 (3.600.000) $939,600 (sales (564,000) [icogs $ [Icogs] [sales) $ 375,600 [C] 1,560,000 80,400 1996,000) $644,400 (D) (243,600) $132.000 $ $ [E] $2.619,600 644,400 (144,000) $3,120.000 $486.000 132,000 (18.000) 5600.000 IC) $ Gross profit Income (loss) from subsidiary Operating expenses Net income Statement of retained earnings: BOY retained earnings Net income Dividends EOY retained earnings Balance sheet: Assets Cash Accounts receivable Inventory PPE, net Customer List Royalty agreement Goodwill Equity investment $ 5756.000 672,000 1,020,000 4,800,000 5300,000 228.000 276.000 516.000 3333 ) fico) DI IDI 0 1.152.000 Dicope 19 CE) [A $ $8.400.000 511320.000 $ Liabilities and stockholders' equity Accounts payable Other current liabilities Long-term liabilities Common stock APIC Retained earnings $360,000 $110,400 Upayl 480,000 152,400 3,000,000 313,200 816.000 60,000 [E] 624,000 84,000 [E] 3,120,000 600,000 $8,400,000 $1.320.000 $ $ $ Consolidation spreadsheet for continuous sale of Inventory. Equity method Assume that a parent company acquired a subsidiary on January 1, 2016. The purchase price was $600.000 in excess of the subsidiary's book value of Stockholders' Equity on the acquisition date, and that excess was assigned to the following AAP assets: Original Original Useful AAP Anet Amount Life Cars Property plant and equipment Pret 5120.000 20 Customer 210.000 10 Royalty freement 10 Good 120.000 The AP assets with a defnite useful life have been amortured as part of the parent's equity method accounting The Goodwill asset has been tested annually for impairment, and has not been found to be paired