hi can someone please do question D and E.

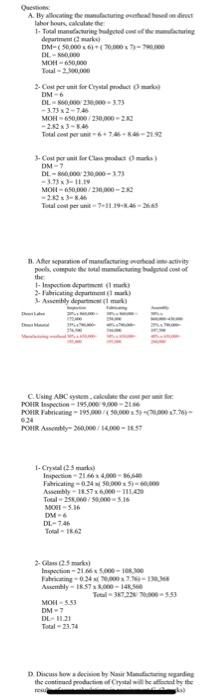

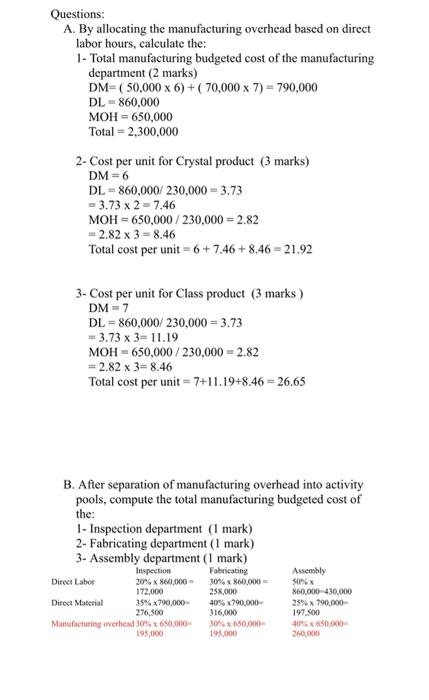

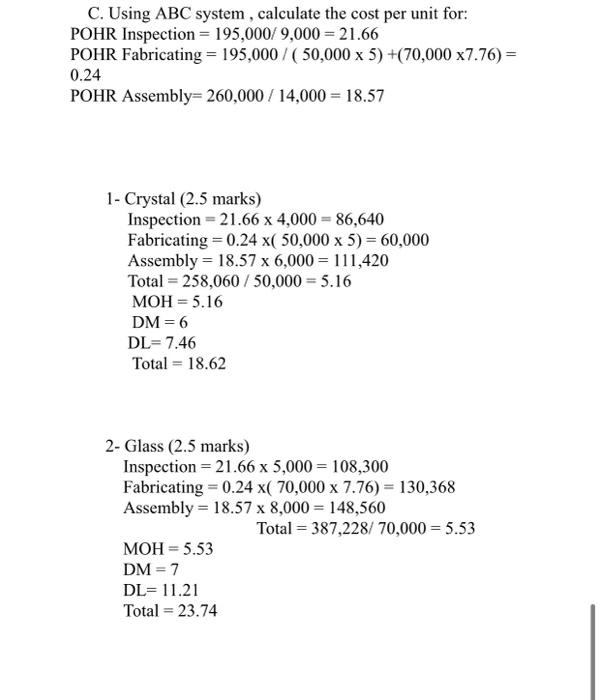

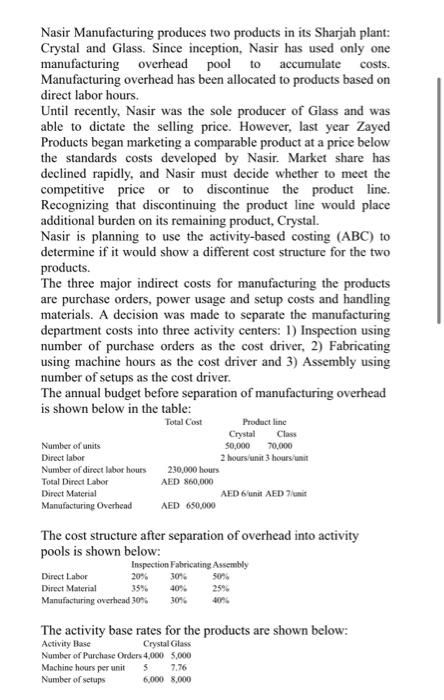

Nasir Manufacturing produces two products in its Sharjah plant: Crystal and Glass. Since inception. Nasir has used only one manufacturing overhead pool to accumulate costs. Manufacturing overhead has been allocated to products based on direct labor hours. Until recently, Nasir was the sole producer of Glass and was able to dictate the selling price. However, last year Zayed Products began marketing a comparable product at a price below the standards costs developed by Nasir. Market share has declined rapidly, and Nasir must decide whether to meet the competitive price or to discontinue the product line. Recognizing that discontinuing the product line would place additional burden on its remaining product, Crystal. Nasir is planning to use the activity-based costing (ABC) to determine if it would show a different cost structure for the two products. The three major indirect costs for manufacturing the products are purchase orders, power usage and setup costs and handling materials. A decision was made to separate the manufacturing department costs into three activity centers: 1) Inspection using number of purchase orders as the cost driver, 2) Fabricating using machine hours as the cost driver and 3) Assembly using number of setups as the cost driver. The annual budget before separation of manufacturing overhead is shown below in the table: Total Cost Product line Crystal Class Number of units 50,000 70,000 Direct labor 2 hours unit 3 hours unit Number of direct labor hours 230,000 hours Total Direct Labor AED 860,000 Direct Material AED 6 unit AED 7 mit Manufacturing Overhead AED 650,000 The cost structure after separation of overhead into activity pools is shown below: Inspection Fabricating Assembly Direct Labor 20% 50% Direct Material 35% 40% 25% Manufacturing overhead 30% 30% 30% The activity base rates for the products are shown below: Activity Base Crystal Glass Number of Purchase Orders 4,000 5,000 Machine hours per unit 5 7.76 Number of setups 6,000 8,000 D. Discuss how a decision by Nasir Manufacturing regarding the continued production of Crystal will be affected by the results of your calculations in requirement C. (2 marks) E. If Nasir decides to moves to mass production and focuses on one product (Glass) by using process costing system in highly automated process. Identify the five steps required of the production the cost report if Nasir uses weighted average method. (2 marks) Quest Ayallering the maturing the time he 1. Total dating departar DM50,00000000-00 DL. MO60 Total 2. Cost per una fortal product DM - 6 DL 0.000 2000 3.73 -3.73 x 2-7.46 MOH650,000/230,000 - 200 -2.52346 Total6.74 3- Cost performs produto DM- DL-00000001 - 3.73)-11.19 MOH-650,000/230,000 - 20 -2 3-4 Totalco per 31.10.26 ther separation of manufacturing watotivity pois completing the cost of the - Indrek - Fabricating departme) Assently department . C. Using ABC system.cale the comper POHR aspection - 195.000 9.00-2156 PH Fabricating - 199,000,000 35 34 POHR Assibly 1- Crystal In 21.6.2016 Fabricating 0.050,000 As 11.574,00 1.2 Toul-25.650,000316 M-6 DL-746 Tool MO5.36 In 16.00-10.30 Facing-03 Amy R7.000- Tel 37290553 MOR-553 DM- DL-1121 Tool-21.74 D. Dichow aby Nadie the command productim of Crystal by the Questions: A. By allocating the manufacturing overhead based on direct labor hours, calculate the: 1- Total manufacturing budgeted cost of the manufacturing department (2 marks) DM=( 50,000 x 6)+( 70,000 x 7) = 790,000 DL-860,000 MOH = 650,000 Total = 2,300,000 2- Cost per unit for Crystal product (3 marks) DM = 6 DL = 860,000/ 230,000 = 3.73 = 3.73 x 2 -7.46 MOH = 650,000/230,000 = 2.82 = 2.82 x 3 = 8.46 Total cost per unit = 6 + 7.46 +8.46 -21.92 3- Cost per unit for Class product (3 marks) DM = 7 DL = 860,000/ 230,000 = 3.73 = 3.73 x 3-11.19 MOH = 650,000/230,000 - 2.82 = 2.82 x 3= 8.46 Total cost per unit - 7+11.1948.46 = 26.65 B. After separation of manufacturing overhead into activity pools, compute the total manufacturing budgeted cost of the: 1- Inspection department (1 mark) 2- Fabricating department (1 mark) 3- Assembly department (1 mark) Inspection Fabricating Assembly Direct Labor 20% x 860,000 -30% x 860,000 172,000 238,000 860,000-430,000 Direct Material 35% x 790,000 40% x 790,000 25% x 790,000 276,500 316,000 197.500 Manufacturing werhead 30% 650,000372 650,000 40 x 650.000 195,000 195,000 260,000 C. Using ABC system, calculate the cost per unit for: POHR Inspection = 195,000/ 9,000 = 21.66 POHR Fabricating = 195,000 / ( 50,000 x 5) +(70,000 x7.76) = 0.24 POHR Assembly= 260,000 / 14,000 = 18.57 1- Crystal (2.5 marks) Inspection = 21.66 x 4,000 = 86,640 Fabricating = 0.24 x( 50,000 x 5) = 60,000 Assembly = 18.57 x 6,000 = 111,420 Total = 258,060 / 50,000 = 5.16 MOH= 5.16 DM = 6 DL= 7.46 Total = 18.62 2- Glass (2.5 marks) Inspection = 21.66 x 5,000 = 108,300 Fabricating = 0.24 x( 70,000 x 7.76) = 130,368 Assembly = 18.57 x 8,000 = 148,560 Total = 387,228/ 70,000 = 5.53 MOH= 5.53 DM = 7 DL= 11.21 Total = 23.74